In 2025, the sector ranking looked familiar, yet the market shape continued to evolve. After dropping from $3b in 2023 to $2.2b in 2024, total funding rebounded to $3.2b in 2025, while the number of companies raising $100k+ stayed broadly stable. In fact, 2025 was driven by a handful of very large cheques and facilities, not by a broad expansion in the number of funded companies, especially those raising smaller tickets.

Fintech stayed #1 on amount raised, but it did not broaden. The sector raised $1.2b in 2025 (vs. $1.1b in 2024) across 124 companies (down from 2024). Top-level concentration eased a bit: in 2025, the top 5 Fintech raisers (M-Kopa, Wave, MNT-Halan, Moniepoint, ValU) accounted for $607m (52%) of the sector total, down from $618m (58%) in 2024 and 66% in 2023. While equity still did most of the work ($685m), debt was large enough ($467m) to keep the topline high even with fewer funded companies. Wave’s $137m debt facility and MNT-Halan’s bond issuance are good examples of the kind of capital that can move a sector total. One note on the exit front: 2025 recorded 49 exits in total (up from 22 in 2024) and the skew was clear towards fintech who accounted for 19 of those.

Energy is where 2025 really changed shape. The sector raised $857m across 50 companies, rebounding from $445m in 2024 to roughly its 2023 level ($792m). Concentration continued: in 2025, the top 5 Energy companies accounted for $701m (82%) of the sector total, up from $351m (79%) in 2024, and 75% in 2023. Debt is the conduit for both growth and concentration in the sector: $611m of Energy’s 2025 total (71%) came through debt, and it was heavily stacked. d.light’s $300m and Sun King’s $156m raises did a lot of the work, with other large facilities like Burn’s $80m reinforcing the same pattern. This is why Energy looks structurally different than other sectors, with a small number of very large deals – disproportionately debt – pulling the line up.

If we step away from Fintech and Energy, the next sectors are much smaller on amount raised but often quite broad on participation. Logistics & Transport raised $309m across 63 companies and was overwhelmingly equity-led (87%). Healthcare raised $211m across 49 companies, again mainly equity-led, but one raise did a lot of the work: LXE Hearing’s $100m round alone represented ~47% of the sector total. Agriculture & Food sits behind them on amount raised ($122m), but shows up on breadth (62 companies).

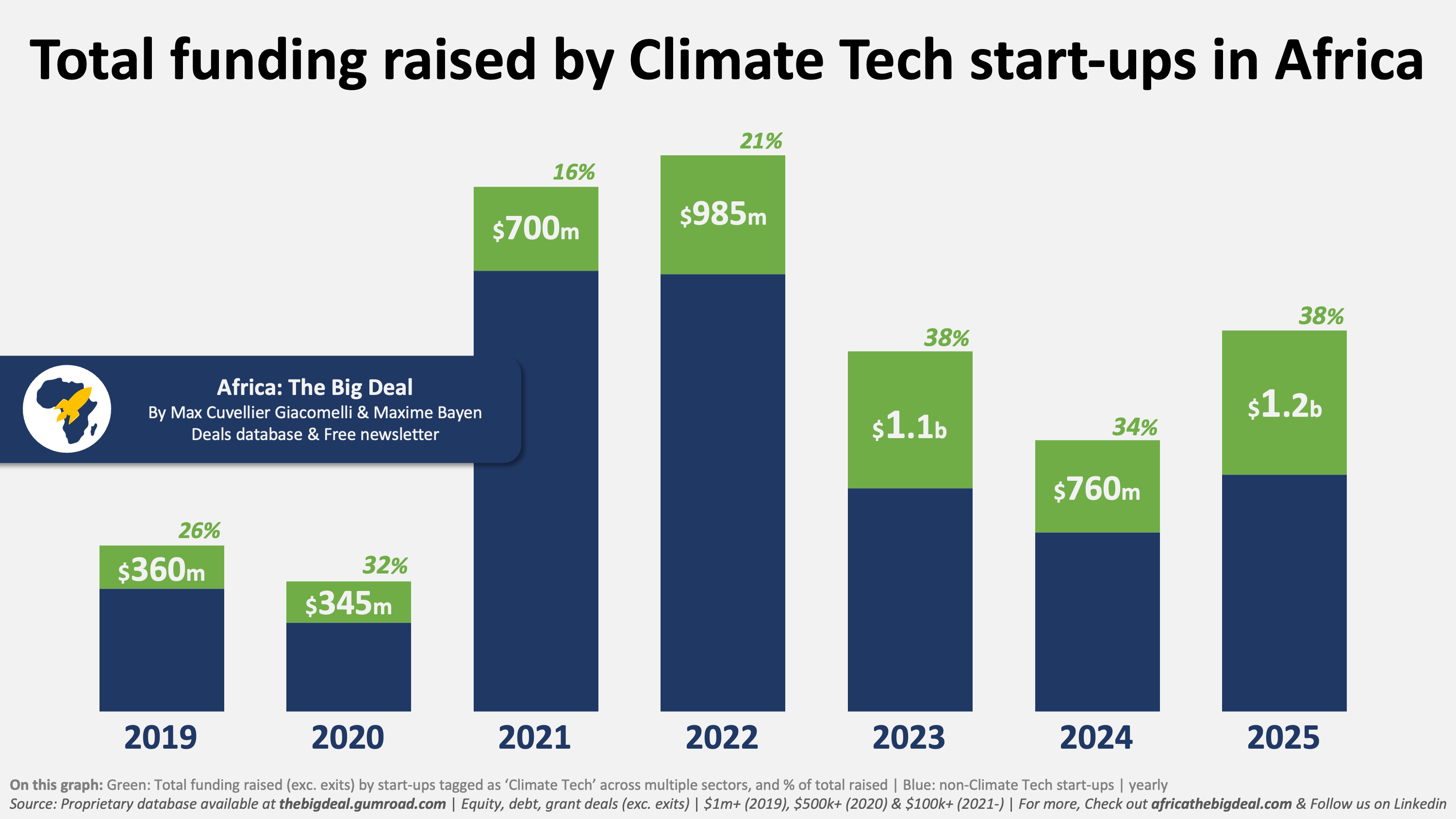

One cross-cut that matters here is Climate Tech. It is not a sector per se but straddles across multiple sectors (Energy, Agriculture, Transport & Logistics etc.). In 2025, Climate Tech companies raised $1.2b across 149 companies, which is 38% of the total amount raised in the year. That compares with $761m (34%) in 2024, and $1.1b (38%) in 2023. What is worth adding is the breadth trend. Since 2023, Climate Tech has consistently increased its share of funded companies, from 26% in 2023 to 28% in 2024 and 29% in 2025. Back in 2021–2022, it was closer to 18-20%. So this is one of the few themes where we can say both that it is large on amount raised and that participation is creeping up.

If you want to go beyond the headline sectors, our database has the full company list behind each total, plus the filters that make many cuts possible (stage, geography, instrument, Climate Tech tags, and more). As always, subscribers to the newsletter (more than 15,000 of you! ) get a special discount. We’ll be back next week with another slice of the data. See you! Max