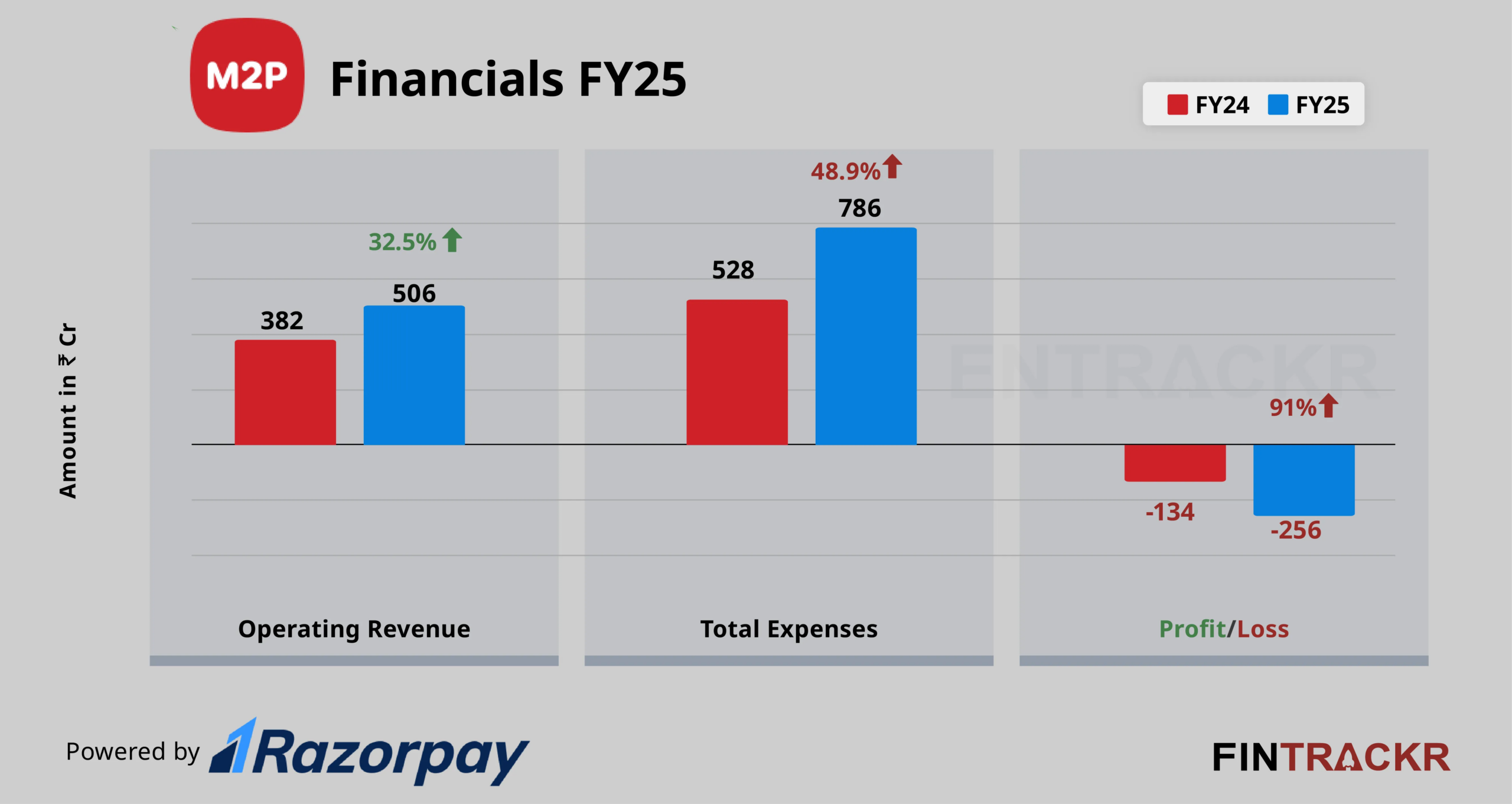

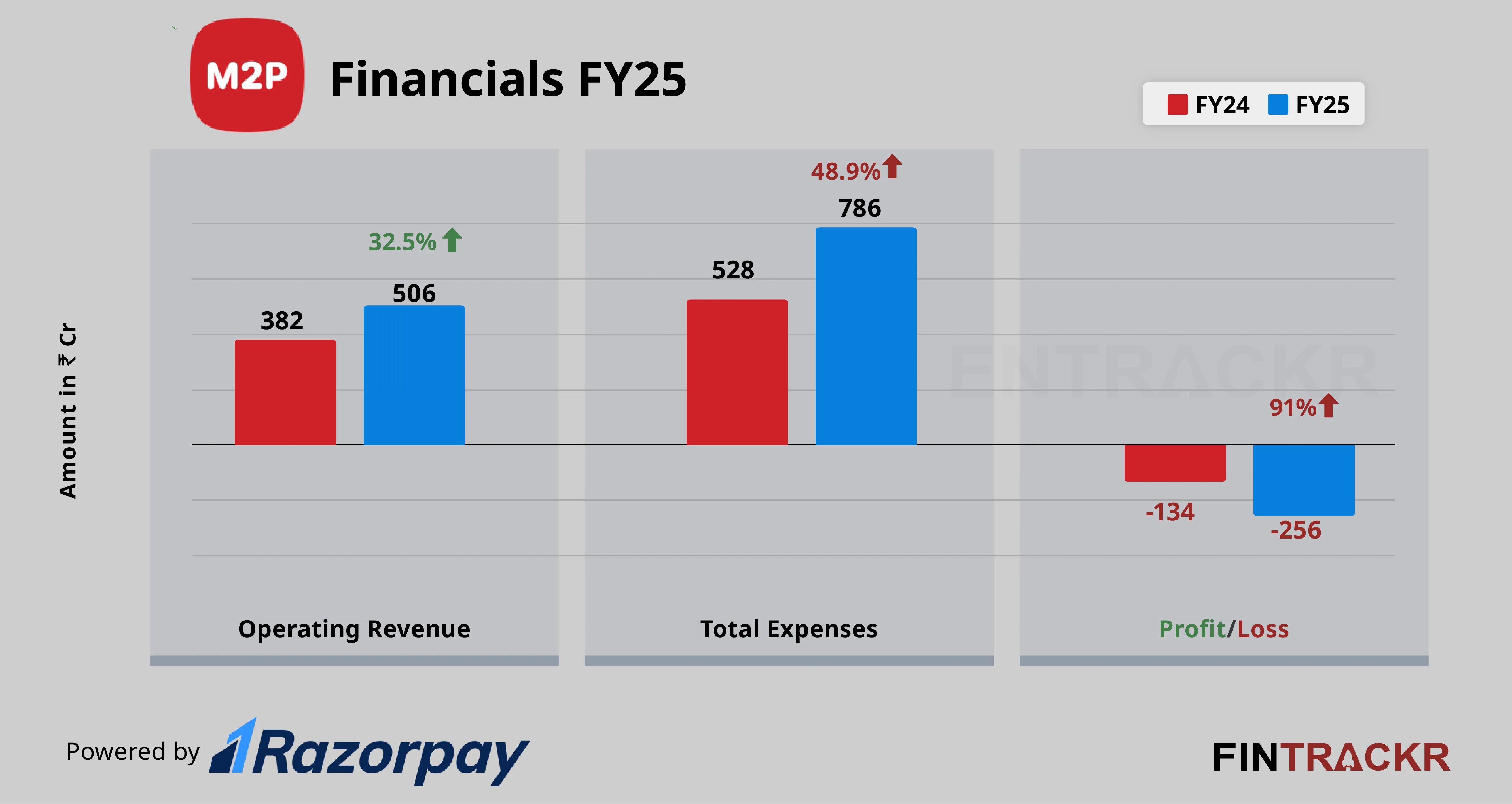

After a dip in scale in the fiscal year ended March 2024, banking infrastructure startup M2P Fintech reported a 33% year-on-year increase in its operating scale and crossed the Rs 500 crore threshold. However, the growth came at a steep cost which surged 90% during the last fiscal year.

M2P Fintech’s revenue from operations grew to Rs 506 crore for the fiscal year ending March 2025 from Rs 382 crore in FY25, its annual consolidated financial statements sourced from the Registrar of Companies (RoC) show.

M2P Fintech offers API infrastructure that allows businesses to launch their own branded financial services through partnerships with fintech firms, while ensuring regulatory compliance. The company operates in more than 30 markets across Asia Pacific, MENA, and Oceania, and claims to support over 200 banks and 300 lenders.

Significantly, the Tiger Global-backed firm has not disclosed its revenue breakdown for the last fiscal year. It earns revenue from multiple streams, including API usage fees, card issuance and management fees, platform subscription charges, commissions from banking partnerships, lending solutions, cross-border forex services and others.

The company earned almost all of its revenue from the domestic market, with only Rs 5.7 crore coming from export services, despite operating in over 30 markets across the Asia Pacific, MENA, and Oceania regions.

The firm also earned around Rs 25 crore from non-operating sources, recorded under miscellaneous income, which took its overall income to Rs 531 crore in the last fiscal year.

For the SaaS firm, spending on technology, cloud services, and co-branding was the largest cost for the firm, around 41%, which doubled to Rs 325 crore in FY25 as compared to Rs 160 crore in FY24. The employee benefits expenses also rose 24% to Rs 311 crore, which includes a non-cash ESOP cost of Rs 40 crore.

Legal, advertising, impairment, depreciation & amortization, travel, and other overhead expenses brought M2P’s total costs to Rs 786 crore, a 49% year-on-year increase compared to Rs 528 crore FY24.

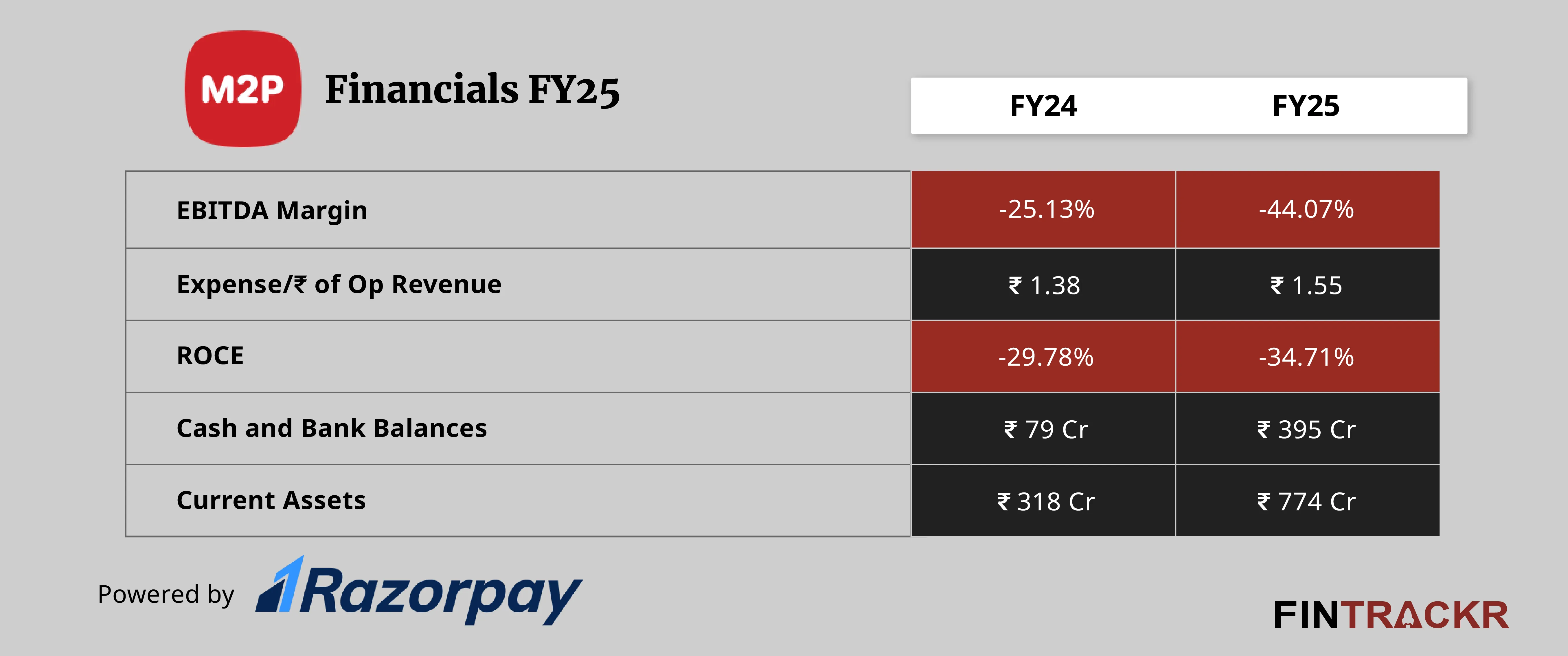

The company’s losses widened 91% to Rs 256 crore in the last fiscal, as technology-related costs doubled during the period, which caused overall expenses to rise faster than operating scale. On a unit level, the company spent Rs 1.55 to earn one rupee in FY24.

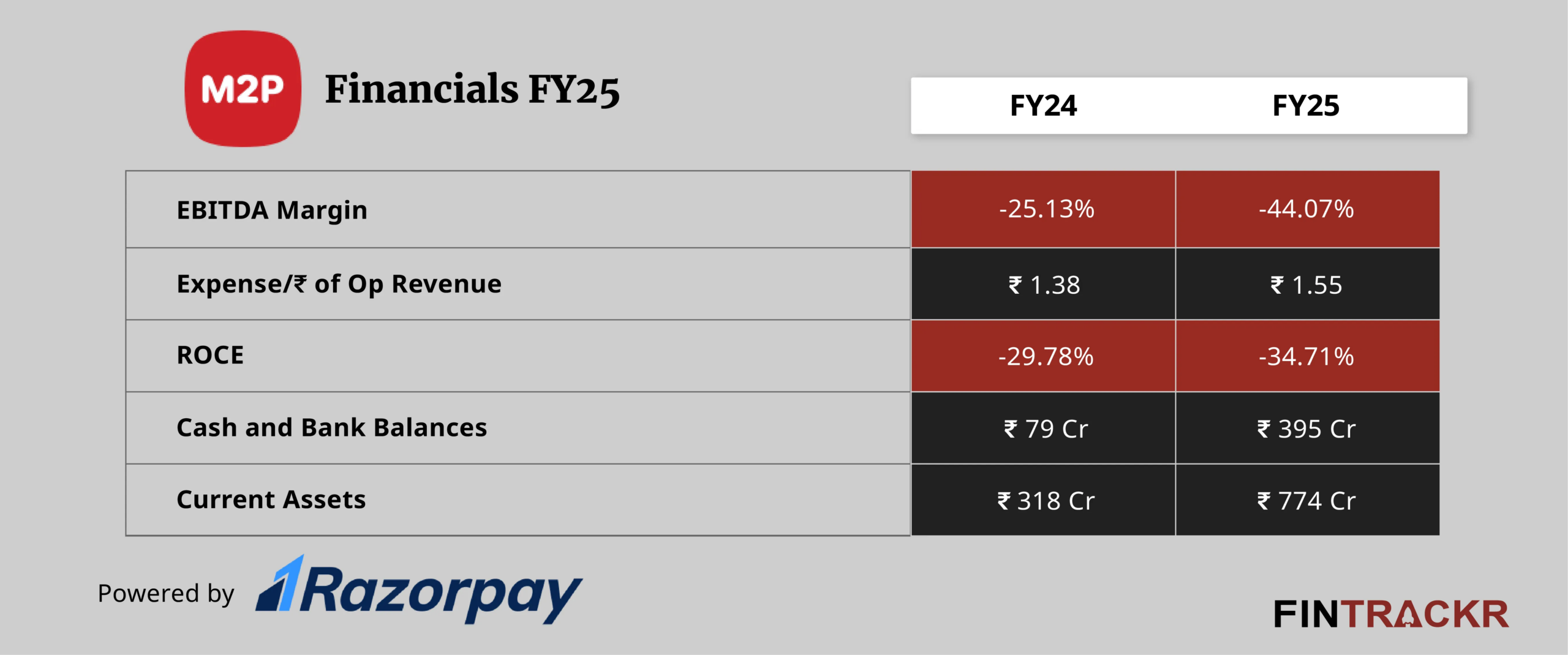

M2P Fintech recorded a negative ROCE of -34.71% and an EBITDA margin of -44.07%. Its EBITDA (loss) stood at Rs 223 crore during the period.

The Chennai-based company’s total current assets stood at Rs 774 crore, including Rs 395 crore in cash and bank balances as of March 2025.

M2P has raised over $200 million to date, including $100 million in its Series D round through a mix of primary and secondary transactions led by Helios Investment Partners in September 2024. In March last year, the company also acquired Chennai-based Mad Street Den in a distress sale valued at around $10–15 million.

M2P does come across as a firm that may have benefited from relatively easy funding, if one goes by the numbers. The overseas numbers are pitiably poor, even if the names might have helped raise funding in the lost round perhaps. Negative margins, and that too heavily, in the segments it operates in make the road to profitability even stiffer, with volatility the order of the day in these segments today. While miscellaneous income does indicate reserves in hand for the near future, raising a fresh round at a reasonable valuation might be tougher than it looks, considering the disintermediation that is always looming over the fintech sector, especially in India.

The firm’s aggressive acquisition strategy which ended with the acquisition of Mad Street Den, also includes Goals101 (AI transaction intelligence, 2023), Syntizen (identity verification). The idea behind these, to bolster AI, personalization, and core capabilities, considered key for future-proofing against trends like agentic AI and composable finance have not convinced enough people. Disruptions of the kind we are seeing right now thanks to the West Asia conflict will only queer the pitch further. The firm could soon find itself finding a choice between conserving funds and keep investing in promising products that have not delivered yet. It’s a luxury that comes with a definite expiry date to make that choice itself, and M2P might just find its more consequential than ever if an IPO was the best hope it had for riding through FY27 and beyond.

Source link