Zimbabwe’s 2026 tech regulations introduce sweeping changes for cryptocurrencies, mobile money, and startups. Key updates include new licensing requirements, increased taxes, and stricter data protection rules, all aimed at formalizing the digital economy. While these measures provide clarity and legitimacy, they also impose higher costs and compliance demands.

Key Points:

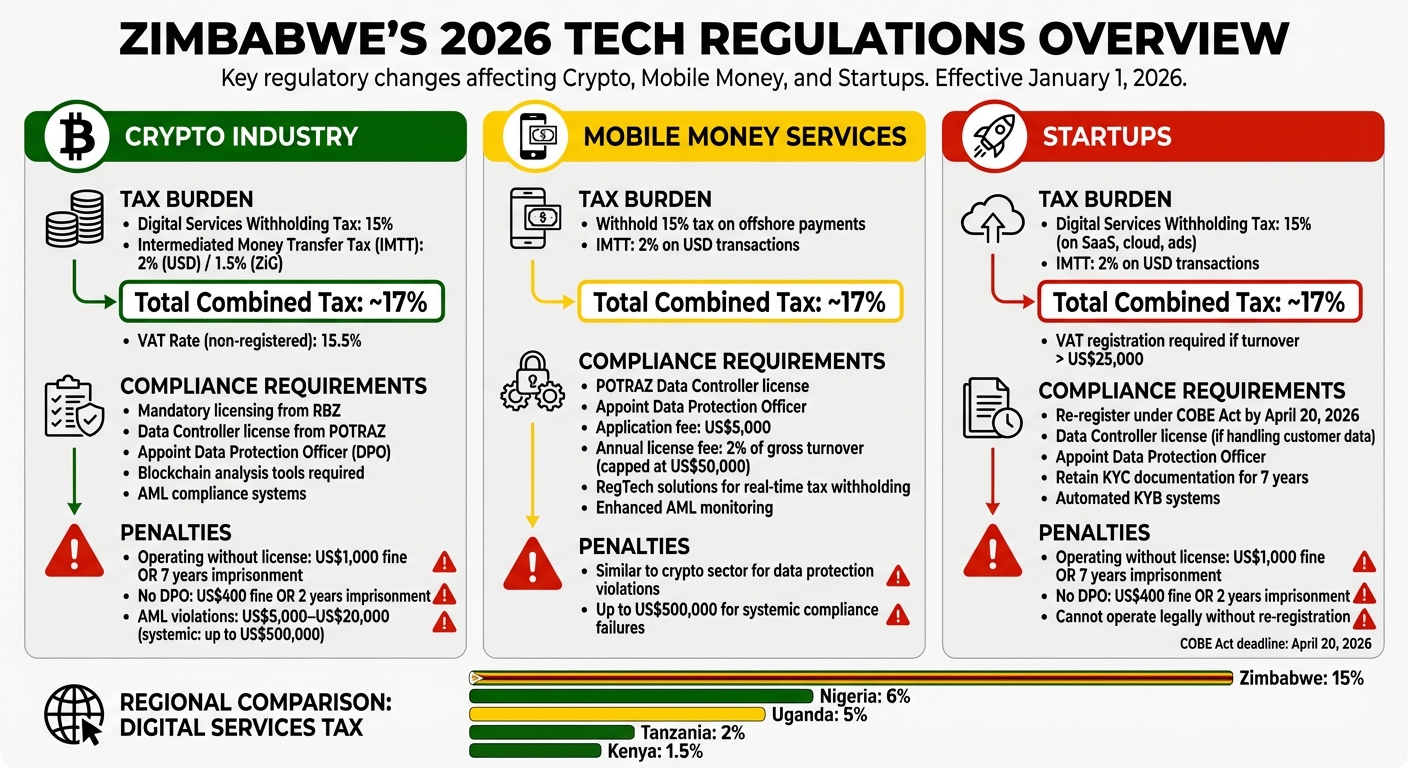

- Crypto: A 15% tax on international digital services, 2% transaction tax, and mandatory licensing for platforms. Non-compliance risks fines and imprisonment.

- Mobile Money: Operators must withhold a 15% tax on cross-border payments and comply with new data protection laws.

- Startups: Face a 15% tax on international tools like SaaS and cloud services, plus mandatory re-registration under the COBE Act by April 20, 2026.

- Compliance Costs: Businesses must invest in AML systems, data protection officers, and blockchain analysis tools.

These regulations aim to tighten oversight but could push some businesses and consumers toward informal channels due to increased costs.

Zimbabwe 2026 Tech Regulations: Tax Rates and Compliance Costs by Sector

1. Crypto Industry

Tax Implications

Zimbabwe’s 2026 tax framework introduces a challenging landscape for both crypto users and platforms, with hefty tax obligations that stand out even in comparison to neighboring countries. The Digital Services Withholding Tax (DSWT) imposes a 15% charge on payments to offshore crypto exchanges. For example, a US$1,000 deposit to an offshore platform would incur an extra US$150 in taxes. This rate is significantly higher than Kenya’s 1.5% and Tanzania’s 2%. Additionally, the Intermediated Money Transfer Tax (IMTT) applies to all crypto on-ramp and off-ramp transactions, charging 2% on USD transfers and 1.5% on ZiG currency transactions. Together, these taxes can total approximately 17% on digital outflows.

For non-resident crypto service providers not registered for VAT, a standard 15.5% VAT rate will be withheld at payment starting January 1, 2026. However, there is a slight relief for locally registered crypto-asset service providers, as the IMTT is now tax-deductible for Corporate Income Tax purposes.

The government’s Tax and Revenue Management System (TaRMS) plays a central role in monitoring transactions in real time, making it nearly impossible for high-volume crypto-to-fiat trades to go unnoticed. Explaining the rationale behind these measures, Finance Minister Mthuli Ncube stated:

The rapid expansion of the digital economy has enabled offshore digital platforms to supply services directly to domestic users without establishing a physical presence in the country.

While these tax measures aim to regulate the growing crypto sector, they also create significant hurdles for platforms, especially when combined with stringent data protection requirements.

Data Protection Requirements

In addition to taxation, Zimbabwean regulators are implementing strict data protection rules to safeguard users and align with international practices. Under SI 155 of 2024, crypto platforms are now classified as “data controllers”. This classification comes with several obligations, including:

- Obtaining a data controller license from POTRAZ.

- Appointing a Data Protection Officer (DPO) and submitting their details in writing.

- Facing penalties of up to US$1,000 or seven years’ imprisonment for operating without a license.

- Incurring fines of US$400 or two years’ imprisonment for failing to appoint a DPO.

Moreover, crypto businesses must ensure corporate clients meet compliance deadlines. For instance, all corporate clients need updated, QR-coded certificates from PACRA before the April 20, 2026, re-registration deadline under the COBE Act. Non-compliance with Anti-Money Laundering (AML) regulations can lead to fines ranging from US$5,000 to US$20,000, with systemic violations resulting in penalties as high as US$500,000.

These data protection requirements significantly increase operational expenses, adding to the financial strain caused by the country’s tax policies.

Compliance Costs

The financial burden on crypto platforms doesn’t stop at taxes and data protection. Blockchain-based projects overseen by the Carbon Market Management Authority (ZCMA) require government approvals, with authorities historically demanding up to 50% of revenues from such initiatives. This has led to a climate of mistrust among investors. Although the exact fees for 2026 crypto licenses remain unclear, platforms are expected to invest in expensive blockchain analysis tools to comply with AML and “Travel Rule” obligations.

Mercy Kamau, Communications Officer at Tax Justice Network Africa, highlighted the need for accountability in the crypto space:

Cryptocurrencies should be tools for empowerment, not enablers of crime. It is time regulators step up, and perpetrators face the consequences.

However, industry experts caution that the steep 15% digital tax could push users toward informal “black market” channels as they try to avoid the formal banking system. This shift could undermine the very goals of regulation and taxation, creating new challenges for the government and the industry alike.

sbb-itb-dd089af

2. Mobile Money Services

Tax Implications

Mobile money platforms in Zimbabwe now serve dual roles: service providers and tax collectors. Starting January 1, 2026, these operators are required to withhold a 15% tax on payments made to offshore digital service providers, covering areas like cloud services, streaming platforms, and digital advertising. This tax is in addition to the existing 2% Intermediated Money Transfer Tax (IMTT) on USD transactions, creating a combined tax load of about 17% on digital transactions.

This policy impacts mobile money providers in two key ways. First, they face higher costs for essential imported digital tools and IT infrastructure now subject to the 15% tax. Second, they must implement real-time tax withholding systems, adding operational complexity. Christopher Mugaga, CEO of the Zimbabwe National Chamber of Commerce, highlighted the broader impact:

It means minimum prices are going to increase by 15%. This is going to increase service inflation, telecoms inflation and the cost of doing business.

Zimbabwe’s 15% rate stands out as notably higher than those in neighboring countries – Kenya charges 1.5%, Tanzania 2%, Uganda 5%, and Nigeria 6%. Jacob Mutisi, Chairperson of the Zimbabwe Information and Communication Technology Division, expressed concerns:

The tax will increase the cost of doing business and accessing services, encourage avoidance through diaspora-based payments and cash transactions, and push users away from formal banking channels.

These tax measures align with Zimbabwe’s broader efforts to regulate its digital economy, mirroring steps taken in the cryptocurrency sector.

Data Protection Requirements

Mobile money operators must now secure a POTRAZ data controller license and appoint a Data Protection Officer (DPO). Non-compliance carries penalties similar to those imposed in the crypto sector. These rules aim to strengthen user data security under heightened regulatory oversight. They apply to any entity processing personal data electronically for profit, expanding the scope of responsibilities beyond those outlined in the previous Cyber and Data Protection Act.

Compliance Costs

The financial and operational demands on mobile money providers continue to grow. They are required to pay a $5,000 application fee for new licenses, an annual license fee of 2% of gross turnover (capped at $50,000), and invest in RegTech solutions. These technologies are essential for managing real-time tax withholding, foreign exchange reporting, and stricter Anti-Money Laundering (AML) monitoring.

These rising costs are likely to be passed on to consumers, potentially driving more transactions into Zimbabwe’s informal economy, which already accounts for 76% of economic activity.

Omari – Digital wallet, Regulatory Reforms, Tax Burdens, Gold price surge & Bitcoin | Friday Drinks

3. Startups

Just like crypto platforms and mobile money providers, startups in Zimbabwe are now navigating stricter regulatory landscapes.

Tax Implications

Zimbabwean startups are now subject to a 15% Digital Services Withholding Tax on all international payments for essential digital tools like cloud hosting, online advertising, and SaaS platforms. Starting January 1, 2026, banks and mobile money operators will automatically deduct this tax at the point of payment. When combined with the existing 2% Intermediated Money Transfer Tax on USD transactions, startups effectively face a 17% tax on digital outflows. For instance, on January 3, 2026, Stanbic Bank began informing customers via SMS that international card payments would include the 15% withholding tax.

Defending this policy, Finance Minister Mthuli Ncube explained:

“I therefore propose to introduce a Digital Services Withholding Tax at a rate of 15 percent, in lieu of VAT on imported services, for payments made to offshore digital platforms…”

Zimbabwe’s tax rate far surpasses those of regional competitors: Nigeria at 6%, Kenya at 1.5%, and Tanzania at 2%. However, startups registered for VAT can offset this tax if they provide valid invoices from foreign suppliers. Additionally, non-resident service providers must register for VAT in Zimbabwe if their annual turnover exceeds US$25,000.

Data Protection Requirements

Startups handling customer data electronically must comply with strict data protection rules. This includes obtaining a Data Controller license from POTRAZ and appointing a Data Protection Officer (DPO). Non-compliance comes with steep penalties: operating without a license can result in a US$1,000 fine or up to seven years imprisonment, while failing to appoint a DPO may lead to a US$400 fine or two years imprisonment. By late 2025, only 831 organizations had achieved formal compliance with these data protection regulations.

Startups are also required to retain KYC documentation and digital onboarding logs for seven years – two years longer than the global FATF recommendation of five years. Dr. Gift Machengete, POTRAZ’s Director General, highlighted the importance of these measures:

“By certifying Data Protection Officers and licensing Data Controllers, Zimbabwe has sent a clear message that the country is committed to international best practices for ethical digital transformation.”

While these regulations aim to align Zimbabwe with global standards, they add significant operational challenges for startups.

Compliance Costs

Startups must also re-register under the COBE Act by April 20, 2026, or risk being barred from formal operations. Non-compliance means losing the ability to operate legally, enter contracts, or maintain financial accounts. In addition to re-registration, startups must account for the 15% digital services tax, implement automated KYB systems to meet verification requirements, and comply with resident director mandates.

With Zimbabwe’s informal economy making up about 76% of all economic activity, Jacob Kudzayi Mutisi expressed concerns about these policies:

“The policy sends a message… that banking formally attracts penalties, while informal alternatives offer flexibility and cost savings.”

These measures reflect Zimbabwe’s broader effort to formalize its economy while addressing the challenges of a rapidly digitizing landscape.

Advantages and Disadvantages

Zimbabwe’s 2026 tech regulations bring a mix of opportunities and challenges for fintech, mobile money providers, and startups. While regulatory clarity offers some benefits, the associated costs and requirements create hurdles that businesses must navigate.

For fintech companies, the regulations provide a clear licensing framework under the Reserve Bank of Zimbabwe (RBZ). This formalizes operations and adds legitimacy. However, the application fees and the requirement to partner with local banks create significant barriers to entry, making it harder for smaller players to compete.

Mobile money providers enjoy the benefit of a capped annual fee, which is particularly helpful for high-turnover providers. But this comes at a cost: they face higher operational expenses, including investments in automated anti-money laundering (AML) systems, and risk penalties of up to $500,000 for compliance failures.

Startups face unique challenges under the new tax framework. The 15% Digital Services Withholding Tax significantly increases the cost of using international tools like AWS, Google Ads, and cybersecurity platforms. ZimCyberSecurity has raised concerns, stating:

Applying a similar tax framework in a smaller, import-dependent digital economy… risks turning digital taxation into a consumption penalty rather than a tool for digital equity.

That said, startups can leverage modernized infrastructure improvements, such as QR-coded business certificates and remote biometric onboarding, introduced under Directive RU 2024/02.

Here’s a quick breakdown of the key trade-offs across sectors:

| Sector | Primary Advantage | Primary Disadvantage |

|---|---|---|

| Crypto / Fintech | Clear licensing and legitimacy via RBZ | High entry costs and mandatory local bank partnerships |

| Mobile Money | Capped annual fee for high-turnover providers | 15% digital tax on international payments and increased compliance costs |

| Startups | QR-coded security in corporate registry | 15% tax on international digital tools and SaaS |

The regulations also carry the risk of driving more businesses into Zimbabwe’s large informal economy. With informal activity already making up 76% of the country’s economy, the high tax burden could push users toward alternatives like diaspora cards, offshore fintech platforms, or even cash transactions to avoid formal banking costs.

For businesses that comply, there are clear advantages. Compliance not only secures legitimacy but also offers access to regulatory sandboxes for testing tokenized assets and advanced tools like ZimDigital ID, which streamlines secure customer verification. These developments could pave the way for further regulatory adjustments as Zimbabwe continues its digital evolution.

Conclusion

Zimbabwe’s 2026 tech regulations mark a shift from outright bans to a structured regulatory framework. Crypto firms now have the opportunity to secure licenses and establish banking partnerships, while mobile money providers face an annual fee cap of $50,000. Startups stand to benefit from modernized systems like QR-coded certificates and biometric onboarding.

However, these changes require businesses to act quickly. Companies must re-register under the COBE Act by April 20, 2026, account for the 15% digital services withholding tax, and establish local banking relationships to meet RBZ licensing requirements.

Vusa Chimanikire from Entry highlighted the benefits of this new approach:

Being able to speak directly with regulators presents a simpler gateway to building scalable products instead of having to try to bypass existing regulations because there are no enabling regulations.

With Zimbabwe ranking among the top five in cryptocurrency adoption in sub-Saharan Africa, licensed exchanges have a chance to capture market share from informal operators. Tools like the RBZ Regulatory Sandbox and ZimDigital ID system simplify testing and customer verification, giving companies that invest in automated KYC and AML systems a clear edge. As enforcement ramps up – with fines for serious non-compliance reaching as high as $500,000 – early movers in compliance infrastructure will be better equipped to thrive.

FAQs

How can I reduce the 15% digital services tax on overseas payments?

To lower the 15% digital services tax on overseas payments, you might want to use local payment intermediaries. These intermediaries can automatically deduct the tax when you make a payment, simplifying the process. Another approach is to look into legal avenues, such as challenging the tax or applying for exemptions through relevant regulatory or legislative channels. This tax is enforced through a mandatory withholding system handled by local financial institutions.

What do I need to get a POTRAZ data controller license fast?

To get a POTRAZ data controller license without delays, start by filling out Form DP1 and paying the applicable fees, which range between $50 and $2,500. Make sure you comply with the Cyber and Data Protection Regulations, 2024, and, if required, appoint a Data Protection Officer. Careful preparation and following the regulations closely can make the process much smoother.

What happens if my business misses the COBE re-registration deadline?

If your business fails to meet the COBE re-registration deadline on April 20, 2026, it risks automatic de-registration. This would prevent your business from operating, entering into contracts, or maintaining financial accounts. To steer clear of these serious consequences, make sure to complete all re-registration requirements before the deadline.

Related Blog Posts

Source link