African start-ups are increasingly turning to debt financing as venture capital becomes harder to secure, reshaping what analysts say is now a $1.2 billion market and changing how the continent’s technology companies raise money.

The estimate is drawn from deal data tracked by Africa: The Big Deal and reflects the total value of publicly disclosed debt facilities raised by African start-ups in 2025.

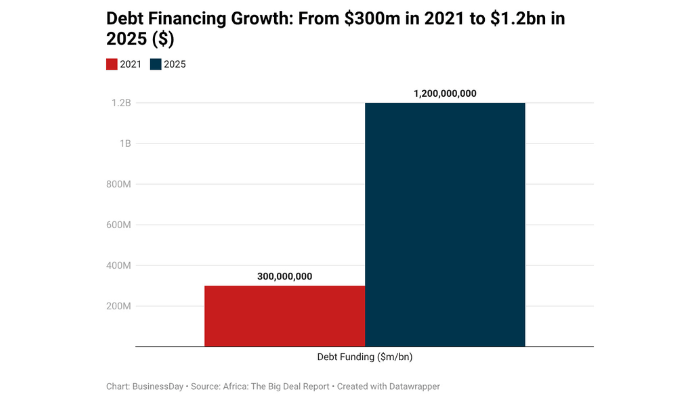

According to the dataset, announced debt funding for African start-ups rose sharply from less than $300 million in 2021 to about $1.2 billion in 2025, showing how loans have moved from a niche financing tool into a major component of the continent’s startup funding landscape.

Read also: African tech debt hits $1.64B in 2025, signaling a structural shift in startup funding

The rise in venture debt comes at a time when the broader technology funding environment across Africa has been under pressure.

After the global venture capital boom slowed and investors became more cautious, many founders began exploring alternative financing structures that allow companies to keep growing without giving up equity stakes.

As a result, loans, structured credit and large financing facilities have started playing a bigger role in supporting expansion across several sectors.

The shift is also visible in how debt now compares with other funding sources. Data from the same research shows that debt’s share of total disclosed startup funding increased significantly over the past four years, rising from about seven percent in 2021 to roughly 38 percent in 2025.

This indicates that debt is no longer just a supplementary option tied to equity rounds but is increasingly used as a standalone funding strategy for companies with strong revenue models.

Despite the growth in overall volume, debt financing still reaches a relatively small number of companies. Over the past five years, only about 169 African start-ups announced debt deals compared with nearly 1,900 companies that secured equity funding during the same period.

This gap highlights a key feature of the market, in that lenders tend to focus on later-stage firms that have predictable income streams and operational scale, Lola Masha, a partner at Antler Africa told BusinessDay.

Many of the companies securing large debt facilities are operating in sectors where revenues are recurring and measurable, particularly energy, financial technology and mobility.

These industries have proven attractive to lenders because repayment structures can be tied to customer payments, equipment financing or other assets that reduce risk.

Some of the continent’s most prominent technology companies have emerged as major borrowers. Solar energy provider d.light, which operates across several African markets, secured one of the largest debt facilities in recent years valued at about $300 million, a deal that alone accounted for a significant portion of total debt announced in 2025.

Nedjip Tozun, d.light CEO commented on the significance of such financing, stating, “The expansion of BLd marks a pivotal moment in our journey to provide affordable solar energy to millions. Securitisation has been a crucial innovation that has allowed us to scale our consumer financing offering, unlocking affordability and enabling us to reach more households, improve livelihoods, and contribute to a sustainable future.”

Other companies frequently appearing in venture debt transactions include Sun King, M-Kopa, Wave and Moove, which operate in sectors ranging from off-grid solar energy to digital payments and vehicle financing.

Firms such as Planet42, Spiro, valU and Burn have also raised structured debt financing to support expansion into new markets and scale their services.

Analysts tracking the sector say a relatively small group of companies now captures the majority of venture debt funding across Africa. Since 2019, the largest borrowers, including companies operating in energy access, fintech lending and mobility infrastructure, have collectively accounted for a substantial share of all disclosed debt raised on the continent.

This level of concentration is significantly higher than what is typically seen in equity funding rounds, where capital tends to be spread across a wider range of start-ups.

The structure of deals also reveals how the market is evolving. In many cases, debt rounds are now announced independently rather than alongside equity financing.

This suggests that lenders are becoming more confident in African startup business models, particularly those that generate steady cash flows through consumer financing or subscription-based services.

Regional patterns are also becoming clearer as the debt market expands. West Africa has often led in terms of the number of debt deals recorded, driven in part by the region’s fast-growing fintech sector and large digital consumer base.

However, East Africa has repeatedly captured the largest loan facilities, particularly in the energy sector, where solar companies have developed scalable financing models in countries such as Kenya and Uganda.

Industry observers note that because the market is still relatively concentrated, a single large transaction can significantly shift regional rankings in any given year.

Another notable development is the changing profile of lenders participating in venture debt deals across Africa.

Earlier in the decade, crowdfunding and retail lending platforms played a more visible role in providing financing to start-ups.

In recent years, however, institutional lenders have become increasingly dominant.

Development finance institutions, commercial banks and specialist private credit funds are now providing a growing share of the capital flowing into the sector, often through structured facilities designed to support long-term expansion.

Patrick Walsh, Sun King co-founder and CEO noted that these debt deals “highlight the growing appetite of Kenyan and regional financial institutions in supporting Africa’s fast-maturing clean energy ecosystem.”

This shift toward institutional funding is widely seen as a sign that Africa’s startup ecosystem is entering a more mature phase.

Larger lenders typically require stronger financial reporting, operational stability and clear repayment structures, meaning the companies receiving debt financing are often those that have moved beyond early-stage experimentation and into scale-up mode.

Tidjane Dème, general partner at Partech Africa, observed: “This year’s rebound highlights the resilience of African founders and the growing sophistication of capital markets across the continent. Debt capital reached an all‑time high… These indicators reflect a healthier, more mature ecosystem.”

Still, analysts caution that the rise of venture debt could deepen existing divides within the ecosystem. While established companies are gaining access to larger financing pools, early-stage start-ups without strong revenues may find it harder to secure either loans or equity funding in a more cautious investment climate.

Read also: Debt financing in tech rivals equity, hits $1bn

Even so, the rapid growth of venture debt is reshaping how Africa’s technology sector finances its expansion. What was once considered a secondary funding option is now becoming a central pillar of the market’s financial structure.

For many founders, the calculation is increasingly straightforward: raising debt allows them to fund growth while retaining control of their companies.

For lenders and institutional investors, Africa’s expanding digital economy presents an opportunity to back businesses with scalable models and growing demand.

As venture capital flows adjust to new global realities, Masha said the role of debt in Africa’s startup ecosystem is likely to expand further, and the continent’s $1.2 billion venture debt market may only be at the beginning of a much larger transformation in how innovation is financed.

Source link