Hey all, Jason here.

Happy Mother’s Day to my fintech and banking moms out there. It’s also the two-year anniversary of end users in the Synapse/Evolve debacle having their funds frozen for those who celebrate!

After ~10 weeks in Mexico (and two side trips to the U.S.), I’m finally back home in the Netherlands. Not going to lie, it’s good to not be living out of a suitcase.

I’m more or less back to regular programming and have a couple exciting and interesting stories in development that I hope to be able to publish in the coming weeks. It’s good to be back!

Parker, which offered banking/treasury management and credit card products targeting ecommerce-focused small businesses, abruptly shut down last Monday.

As recently as last September, the company was promoting that it had “secured over $200M in funding to help further its mission in transforming how digital businesses scale and financially operate” — though $125 million of that total was in the form of an asset-backed lending facility to scale Parker’s credit card program.

Parker did raise $58 million in equity from names that include Valar Ventures and Y Combinator. Parker partnered with Patriot Bank, N.A. on its credit card. The card offered companies “rolling terms,” in which cardholders had six or even eight weeks to pay interest-free from the date of each purchase, rather than using the typical statement cycle approach.

Parker also partnered with Piermont on its bank account/treasury management offering.

But, according to communications sent from Patriot Bank to Parker customers on Sunday, May 3rd, Parker abruptly shut down the following day, Monday, May 4th.

Patriot didn’t respond to questions about why communications about the shutdown were coming from the bank as opposed to from Parker.

According to sources familiar with the situation, Patriot essentially pulled the plug on the program after a potential acquisition of Parker that the company had been negotiating fell apart, despite Parker having some remaining runway.

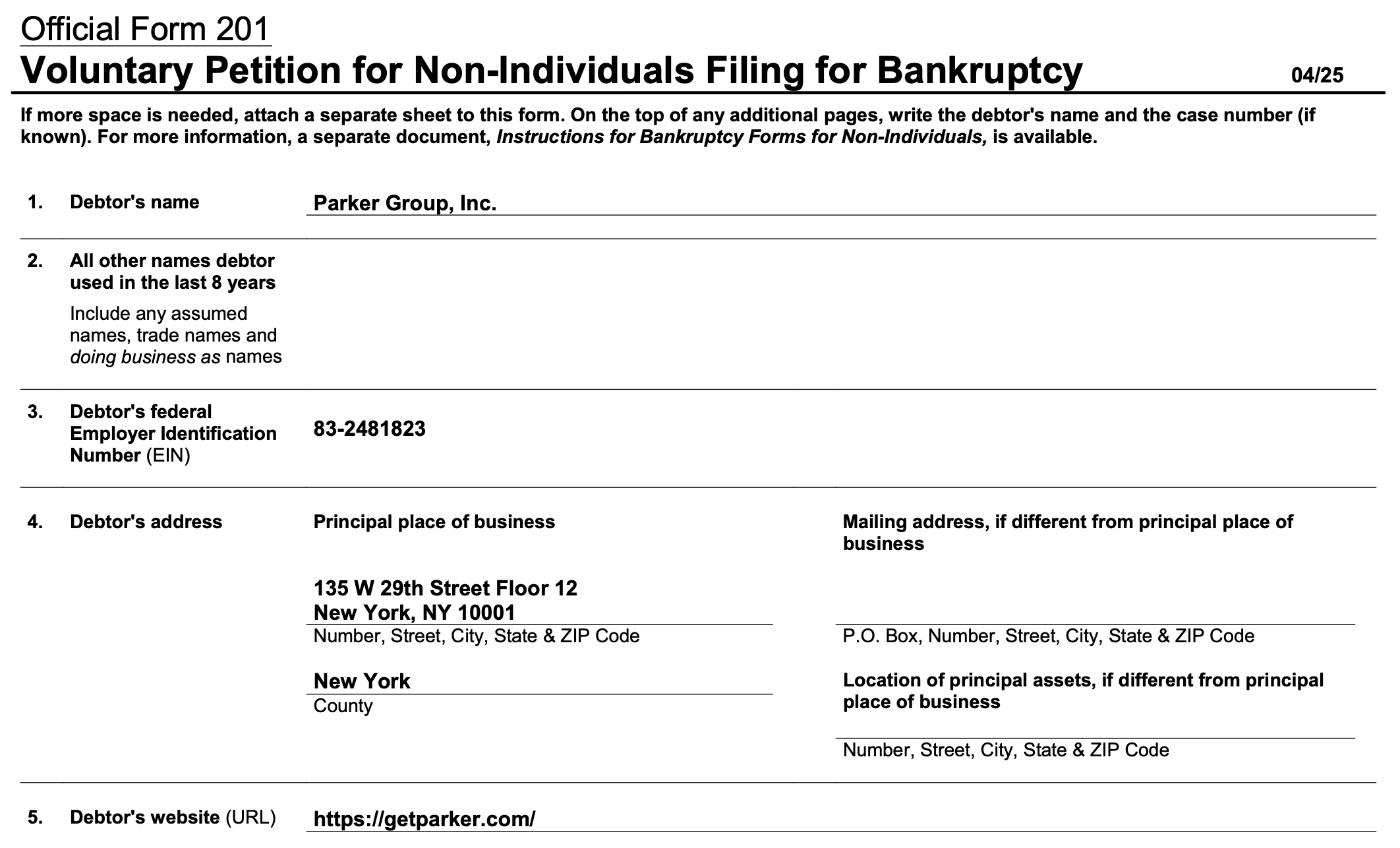

A Parker cofounder described the situation as “a crazy turn of events” in a post yesterday, writing in part, “Three weeks ago, I thought Parker was going to be acquired in a deal worth nearly $90M. Yesterday, we filed for Chapter 7.”

Sources familiar with the situation told Fintech Business Weekly that AI tax compliance startup Avalara was the potential acquirer, but backed out of the deal at the last minute, leading to the abrupt shutdown and subsequent bankruptcy. Representatives for Avalara didn’t respond to questions and a request for comment.

According to Parker’s Chapter 7 petition, the company reports between $50 million and $100 million of assets and between $50 million and $100 million of liabilities, with between 100 and 200 creditors. A note on the court docket indicates Parker’s Chapter 7 filing is currently “deficient,” as it lacks required supporting schedules.

Typically, the next steps would be the automatic appointment of a Chapter 7 trustee to oversee the assets of the estate.

Within 14 days, the estate must file the supporting schedules with the court detailing all assets, all liabilities, executory contracts and unexpired leases, and a statement of financial affairs.

Notably, any customer deposits are held at Piermont and should not be impacted by Parker’s bankruptcy.

However, as has been seen in previous fintech bankruptcies, the failure of a fintech partner can and has impacted end users’ ability to access their funds.

The ability of and time needed for Parker’s small business customers to access any funds likely depends on how Parker’s bank account offering was operationally structured — whether funds were held in an FBO at Piermont and ledgered by Parker (and/or a Parker service provider) vs. whether these accounts were held directly “on core” at Piermont.

Questions and requests for comment sent to representatives for Parker, Avalara, Patriot Bank, and Piermont outside of normal business hours did not receive a response for publication.

This newsletter is made possible thanks to the generous support of paying subscribers. In addition to supporting independent analysis of the banking, fintech, and crypto spaces, paying subscribers get an extended version of this newsletter and access to full archives of past issues (5+ years of newsletter goodness!)

You can support Fintech Business Weekly by upgrading to a paid subscription, or reach more than 90,000+ loyal readers by sponsoring a newsletter.

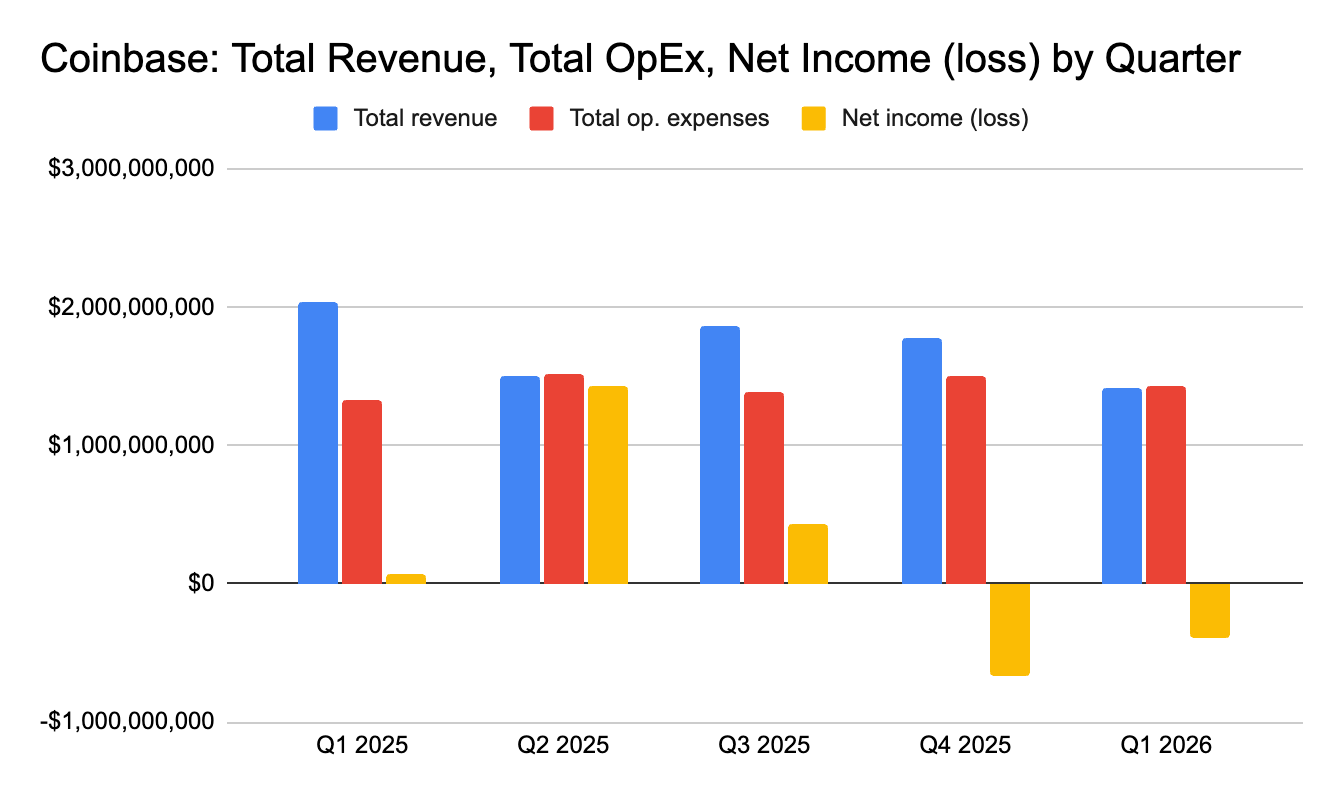

Coinbase had a rough week: in a note laying off 14% of the company’s staff in advance of revealing a 30% drop in revenue and a $394 million loss in the first quarter, company cofounder and CEO Brian Armstrong pointed, in part, to AI, writing, “Non-technical teams are now shipping production code and many of our workflows are being automated.”

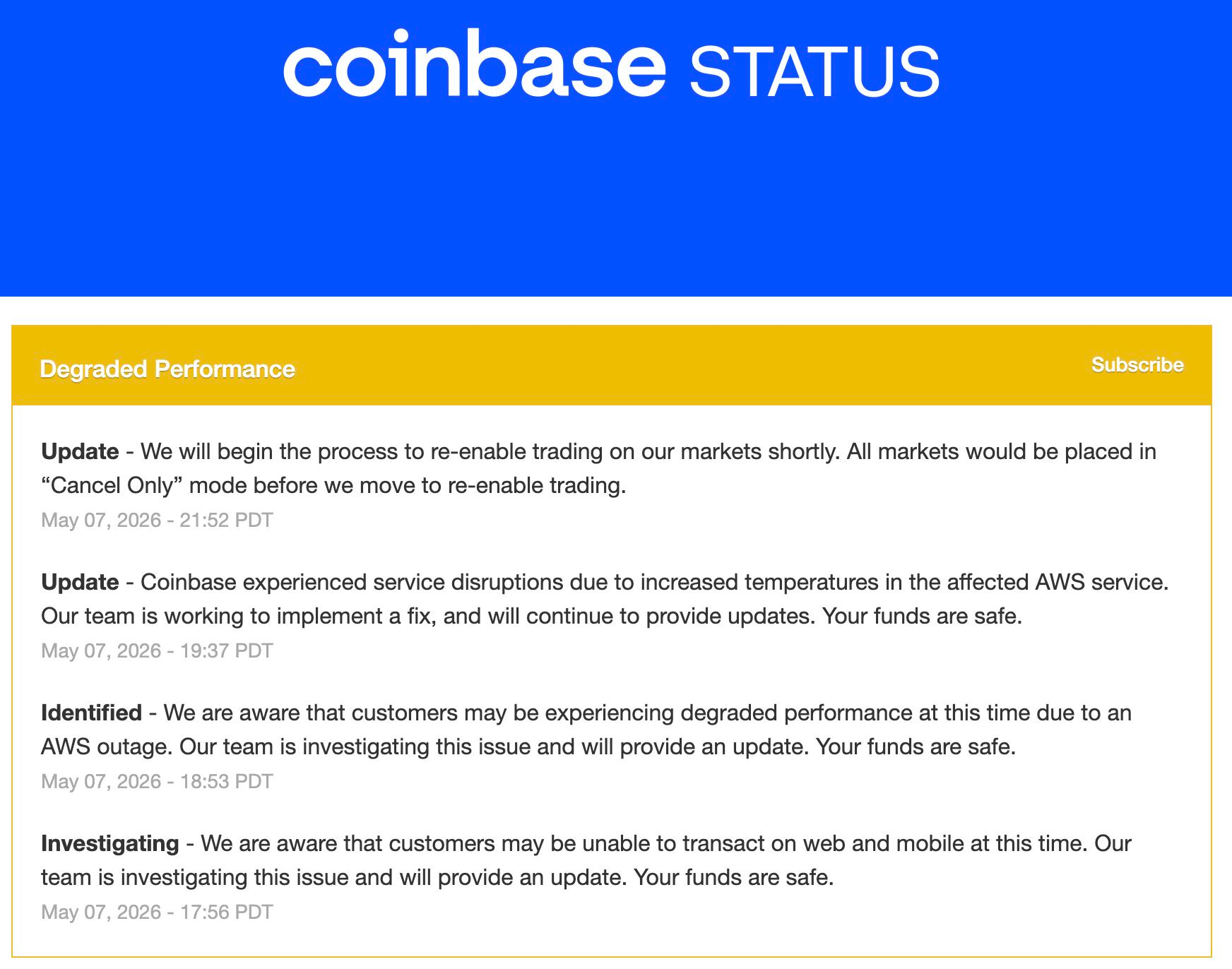

Less than a week after the layoffs, Coinbase experienced a nearly 8-hour outage, including the ability for users to trade on the crypto exchange.

Coinbase blamed a “a room overheating in an [Amazon Web Services] datacenter when multiple chillers failed” for the outage. So much for “decentralization,” I suppose.

Although Armstrong’s layoff note pointed to AI, describing a future vision of Coinbase as “an intelligence, with humans around the edge aligning it,” he also acknowledged the as-of-late lackluster state of crypto markets.

Armstrong wrote, “Crypto is also on the verge of the next wave of adoption, with stablecoins, prediction markets, tokenization, and more taking off. However, our business is still volatile from quarter to quarter. While we’ve managed through that cyclicality many times before and come out stronger on the other side, we’re currently in a down market and need to adjust our cost structure now so that we emerge from this period leaner, faster, and more efficient for our next phase of growth.”

The cyclicality Armstrong describes is crystalized by Coinbase’s quarter-to-quarter performance. The company’s revenue and net income are highly sensitive to cryptoasset prices, particularly bitcoin and ethereum, which comprised 40% and 19%, respectively, of trading volume on the exchange in the first quarter of 2026. Logical or not, users tend to trade more when asset prices are elevated.

The effect on Coinbase’s net income is compounded, as the company also holds crypto on its on balance sheet for investment. Per its most recent quarterly earnings statement, Coinbase holds 16,492 bitcoin and 150,193 ethereum.

The volatility in Coinbase’s primarily transaction-based business helps explain the company’s efforts to diversify by expanding its product offerings, including its recent push into prediction markets.

This January, Coinbase, via a partnership with Kalshi, launched Coinbase Predict, enabling users to speculate on the outcomes of events that include elections, politics, entertainment, and sports.

Progress on the CLARITY Act, commonly described as crypto market structure legislation, has been stalled on a number of issues, most notably the topic of stablecoin “rewards.”

The “rewards” matter has been the subject of fierce, if disingenuous, debate between various stakeholders in crypto world, most vocally Coinbase and its CEO Brian Armstrong, and traditional banking world.

As an avatar for the crypto point of view, Coinbase and Armstrong have, confusingly, describing prohibiting stablecoin rewards as a “bailout” for banks.

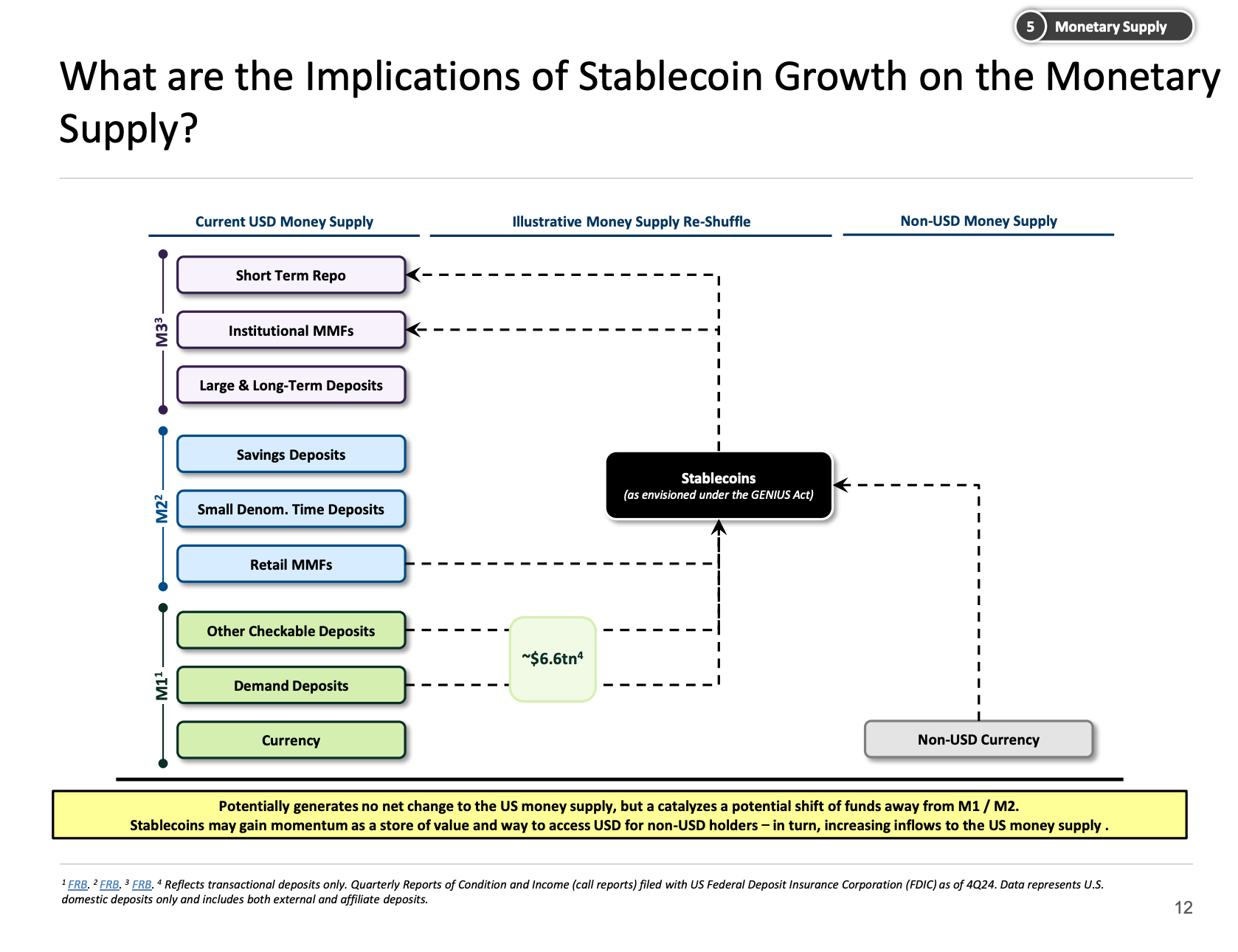

Conversely, banks have latched on to an eye-popping if extremely unlikely risk highlighted in a U.S. Treasury Department report: namely, that as much as $6.6 trillion in deposits could be displaced from the banking system by stablecoins.

That, the banking industry argues, would be a catastrophe for their ability to lend to consumers and business.

The only issue with the “$6.6 trillion” claim? It represents the totality of checkable and demand deposits in the U.S. banking system. It seems exceedingly unlikely ALL consumers and businesses would entirely transition from holding funds in insured depositories to holding funds in stablecoins.

The core piece of the compromise text specifies:

“No covered party shall, directly or indirectly, pay any form of interest on yield (whether in cash, tokens, or other consideration) to a restricted recipient — (A) solely in connection with the holding of such restricted recipient’s payment stablecoins; or (B) on a payment stablecoin balance in a manner that is economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit.”

However, the restriction would not apply to incentives paid “based on bona fide activities or bona fide transactions,” akin to how credit card issuers pay rewards based on purchase activity.

Coinbase CEO Armstrong, who has been a key agitator arguing “rewards” should be permitted, seemed to approve of the new language, posting regarding the updated bill, “Mark it up.”

Some in banking world, though, were less convinced.

A joint statement from American Bankers Association, Bank Policy Institute, Consumer Bankers Association, Financial Services Forum and Independent Community Bankers of America noted the groups appreciated legislators “address[ing] the concerns from banks of all sizes around the risk of deposit flight from paying yield on stablecoins,” but noted that the groups “will be sharing [their] detailed suggestions for strengthening the proposed language with lawmakers in the coming days.”

Despite the seeming compromise, a legal challenge from one or both sides seems likely if and when the bill is finalized and passed into law.

In other stablecoin news last week, the U.S. Department of the Treasury issued a joint notice of proposed rulemaking (NPRM) through the Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) that would define the BSA/AML and sanctions obligations of permitted payment stablecoin issuers, as called for by the GENIUS Act.

Under the proposed rule, stablecoin issuers would be required to:

establish and maintain an anti-money laundering and countering the financing of terrorism (AML/CFT) program;

report suspicious activity;

have the technical capabilities, policies, and procedures to block, freeze, and reject specific or impermissible transactions that violate Federal or State laws, rules, or regulations;

have the technical capabilities to comply, and do comply, with the terms of any lawful order; and

maintain an effective sanctions compliance program.

Also last week, Brazil’s central bank, the Banco Central do Brasil, banned electronic foreign exchange/remittance providers from using cryptocurrencies, including stablecoins, for settling cross-border transactions.

The rule, promulgated by BCB Resolution No. 561 and taking effect on October 1, 2026, would not impact retail users’ ability to buy, sell, hold, or transfer cryptocurrencies or stablecoins.

Rather, the measure requires transactions between an electronic foreign exchange service and any foreign counterparty to be conducted by a foreign exchange transaction or a non-resident real-denominated account in Brazil. This functionally requires electronic foreign exchange providers to work through institutions authorized by the Brazilian central bank.

Impacts will include prohibiting a remittance service from accepting reais from an end users, converting them into stablecoins, and settling the transaction outside of Brazil via a blockchain transaction.

Core banking giant FIS announced a partnership with AI firm Anthropic centered on one of the trendiest areas in financial services at the moment: agents. But is the news more focused on building Anthropic’s narrative (and FIS’ share price) than substance?

Source link