The first half of 2026 was driven by artificial intelligence, with startups such as Neysa and Sarvam AI securing some of the largest funding rounds. But the biggest headline arrived towards the end of the period when CRED raised $900 million from Facebook parent Meta, followed by founder Kunal Shah’s appointment as Global CEO of WhatsApp. These developments lifted startup funding to nearly $7.4 billion, making H1 2026 the second highest funded first half after the 2021 and 2022 boom. The six month period also saw D2C beauty and health brands emerge as attractive acquisition targets, while the IPO pipeline gained momentum with OYO, Zepto, Razorpay, Kuku and Zetwerk moving closer to listings. Turtlemint, Fractal, Shadowfax and Kissht also made their stock market debut.

[Overview]

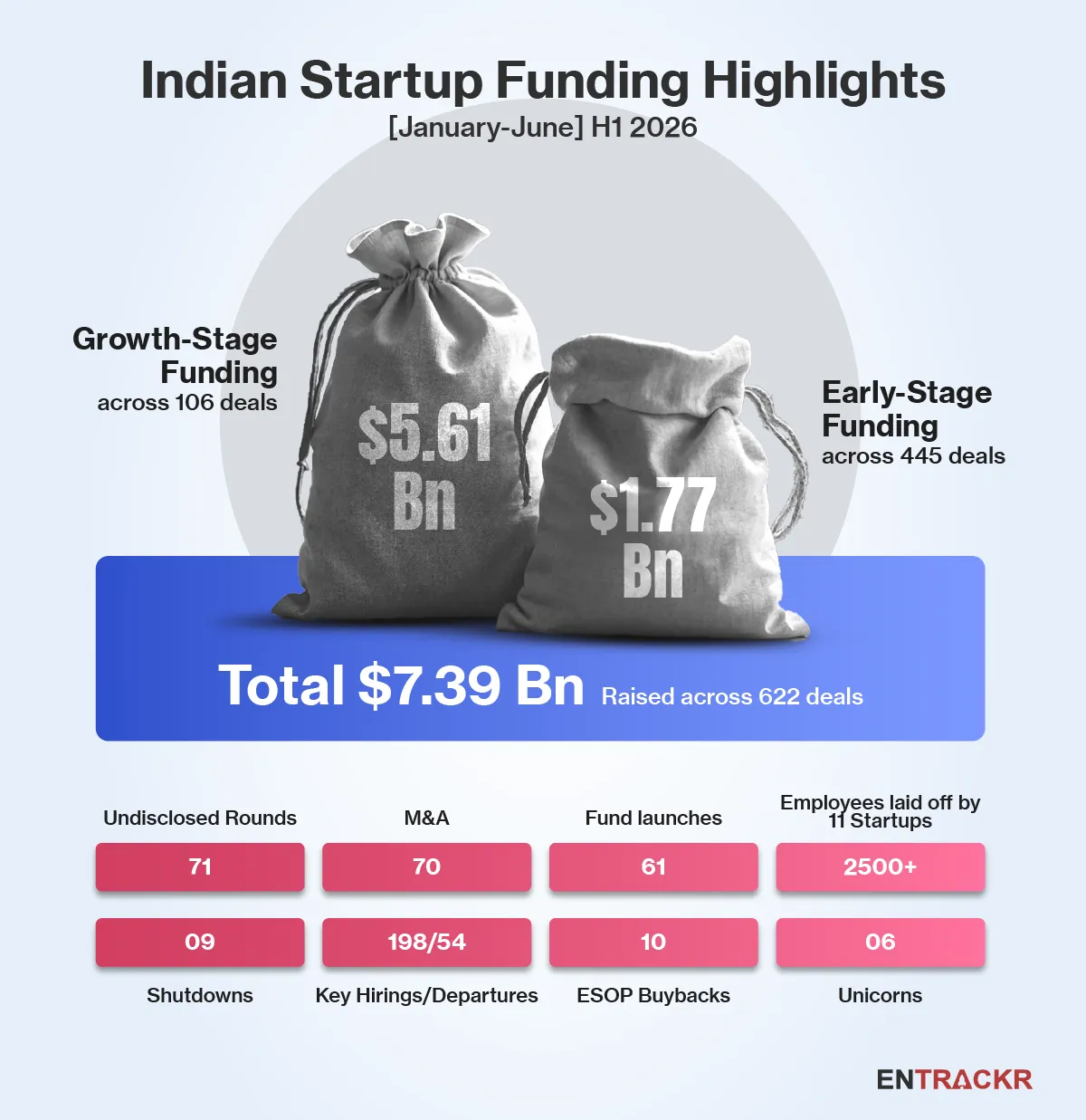

According to data compiled by Entrackr, Indian startups raised approximately $7.4 billion in funding during the first half of 2026. This amount included 106 growth and late-stage deals totaling $5.61 billion, along with 445 early-stage deals worth $1.77 billion. Additionally, there were 71 undisclosed deals during this period.

During this period, six startups including Square Yards, Sarvam AI, Skyroot, KreditBee, Neysa, and Juspay entered the unicorn club. During H1 2025, five startups achieved the feat.

[Y-o-Y and M-o-M trend]

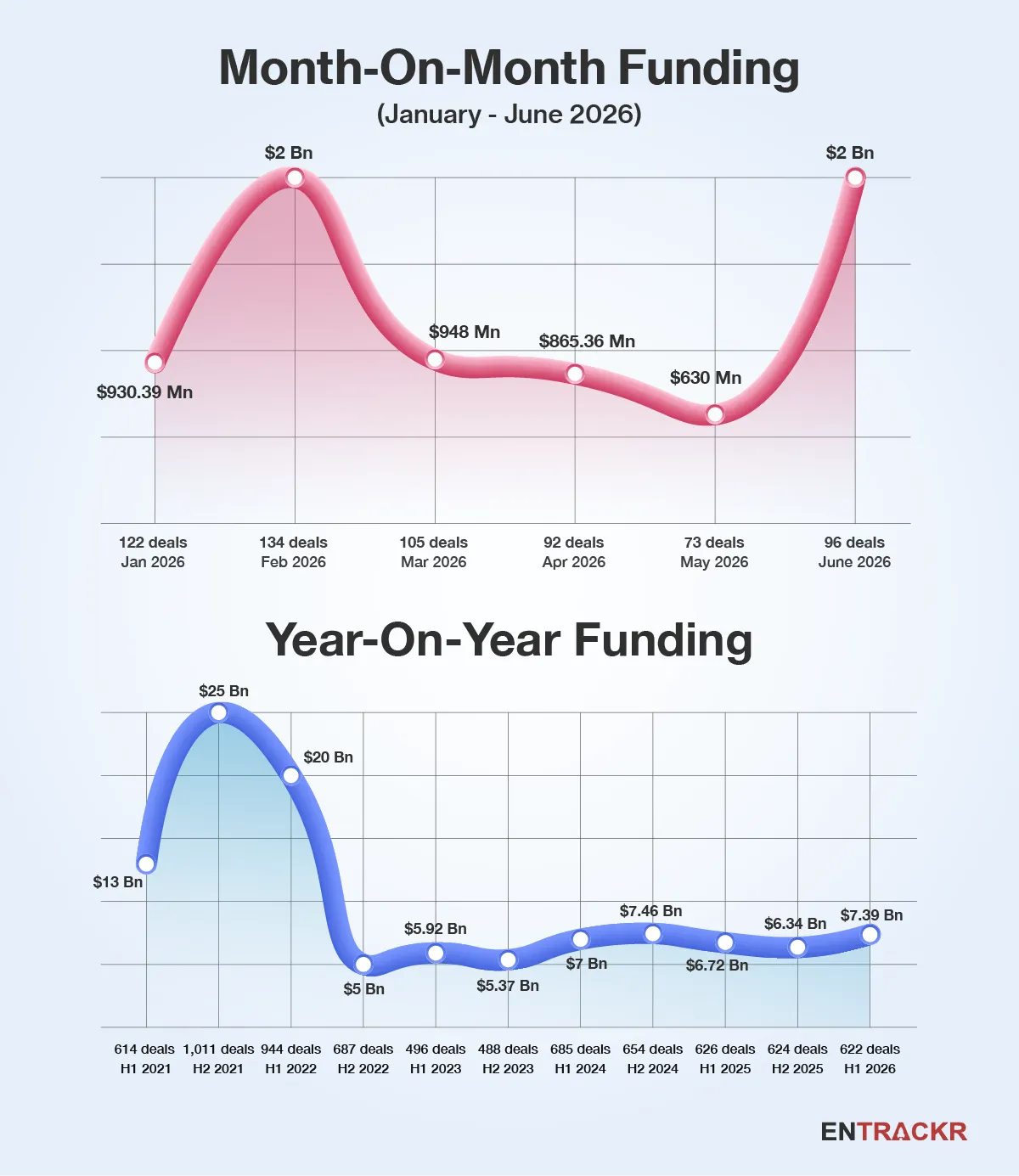

H1 2026 ended on a stronger note than the previous two years, with startups raising $7.39 billion, the highest first half total since 2022. The total surpassed H1 2025 ($6.72 billion) and H1 2024 ($7 billion) but remained well below the $20 billion raised in H1 2022 and the $13 billion recorded in H1 2021.

On a month on month basis, funding more than tripled to $2 billion in June from $630 million in May. This came after three consecutive months of decline.

[Top 10 growth stage deals in H1]

H1 2026 was led by a handful of large growth stage deals, with AI infrastructure startup Neysa topping the chart after raising $1.2 billion. Fintech unicorn CRED followed with a $900 million round, while KreditBee, Rapido, and Sarvam AI rounded out the top five with $280 million, $240 million, and $234 million, respectively. The list also featured Weaver Services, SquareYards, Arya.ag, Drivn, and Polaris, highlighting investor interest across fintech, AI, mobility, proptech, agritech, EV, and manufacturing during the first half of the year.

[Top 10 early stage deals in H1]

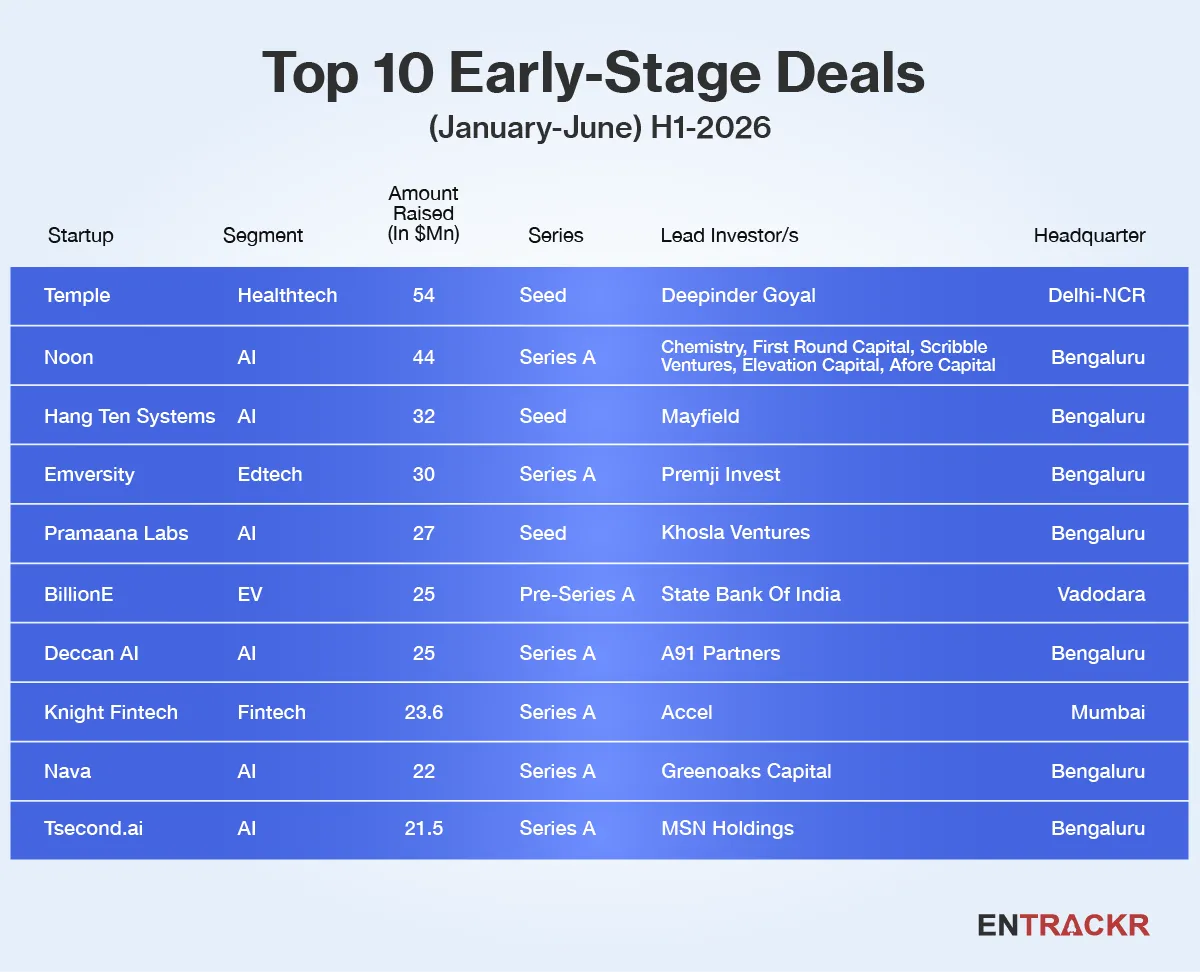

Early stage funding in H1 2026 reflected strong investor interest in AI startups, with Temple leading the chart after raising $54 million, followed by AI native design platform Noon at $44 million and enterprise AI startup Hang Ten Systems at $32 million. Emversity and Pramaana Labs completed the top five with $30 million and $27 million, respectively. The list also included BillionE, Deccan AI, Knight Fintech, Nava, and Tsecond.ai, with AI startups accounting for six of the ten largest early stage funding rounds during the first half of 2026.

[Mergers and Acquisitions]

M&A activity remained steady during H1 2026, led by transactions across consumer brands, healthcare, and fintech. Among the disclosed deals, L’Oréal’s majority stake acquisition of Bare Anatomy parent Innovist, reportedly valued at $350 million to $450 million, was the largest, followed by BillDesk’s proposed acquisition of Worldline SA’s India business for $70.8 million. The D2C beauty and consumer segment saw notable consolidation as Marico acquired a 60% stake in Cosmix for $42 million, Emami bought a 60% stake in InCut Digital for $32.1 million and agreed to acquire Axiom Ayurveda for $26 million, while Honasa picked up a 58% stake in Fluence Pharma for $13.5 million. Healthcare also remained active as Innovaccer, Vaidam Health, MedGenome, CureBay, and Care.fi expanded through acquisitions, reflecting continued consolidation across healthtech and healthcare services.

[City and segment wise deals]

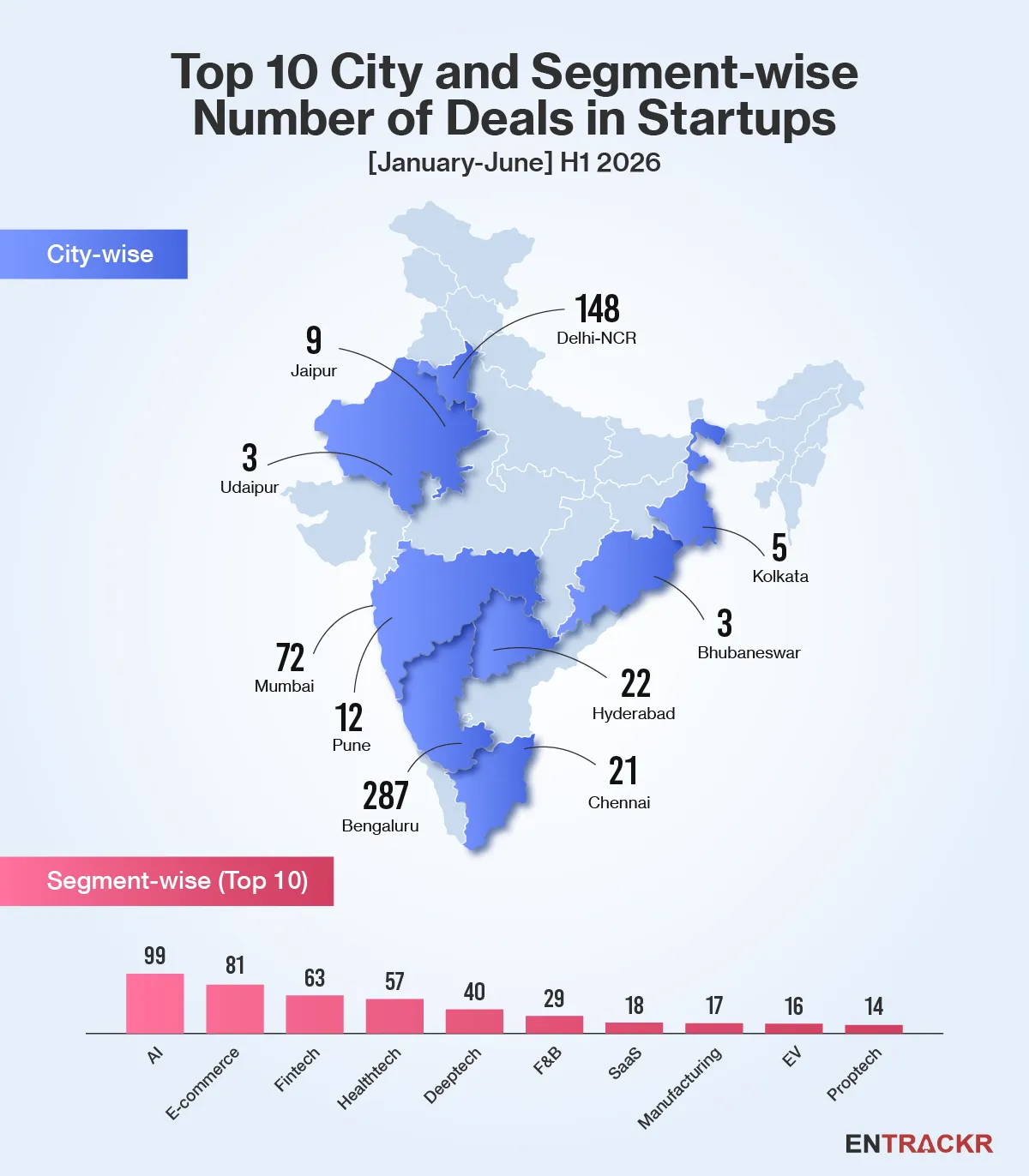

Bengaluru remained the leading startup hub in H1 2026, attracting $3.8 billion across 287 deals, which accounted for 51.45% of the total funding during the period. Mumbai ranked second with $1.96 billion from 72 deals, followed by Delhi NCR, which raised $984.56 million across 148 deals. Hyderabad and Chennai recorded $173.45 million and $154.93 million, respectively. Together, these five startup hubs accounted for more than 95% of the total funding raised in H1 2026.

AI emerged as the most funded sector in H1 2026, attracting $2.07 billion across 99 deals, which accounted for 27.95% of the total capital raised during the period. Fintech followed closely with $1.91 billion from 63 deals, contributing 25.89% of overall funding. E-commerce and healthtech raised $436.47 million and $406.61 million, respectively, while deeptech startups secured $147.22 million across 40 deals. Together, AI and fintech accounted for more than half of the startup funding raised during the first six months of 2026.

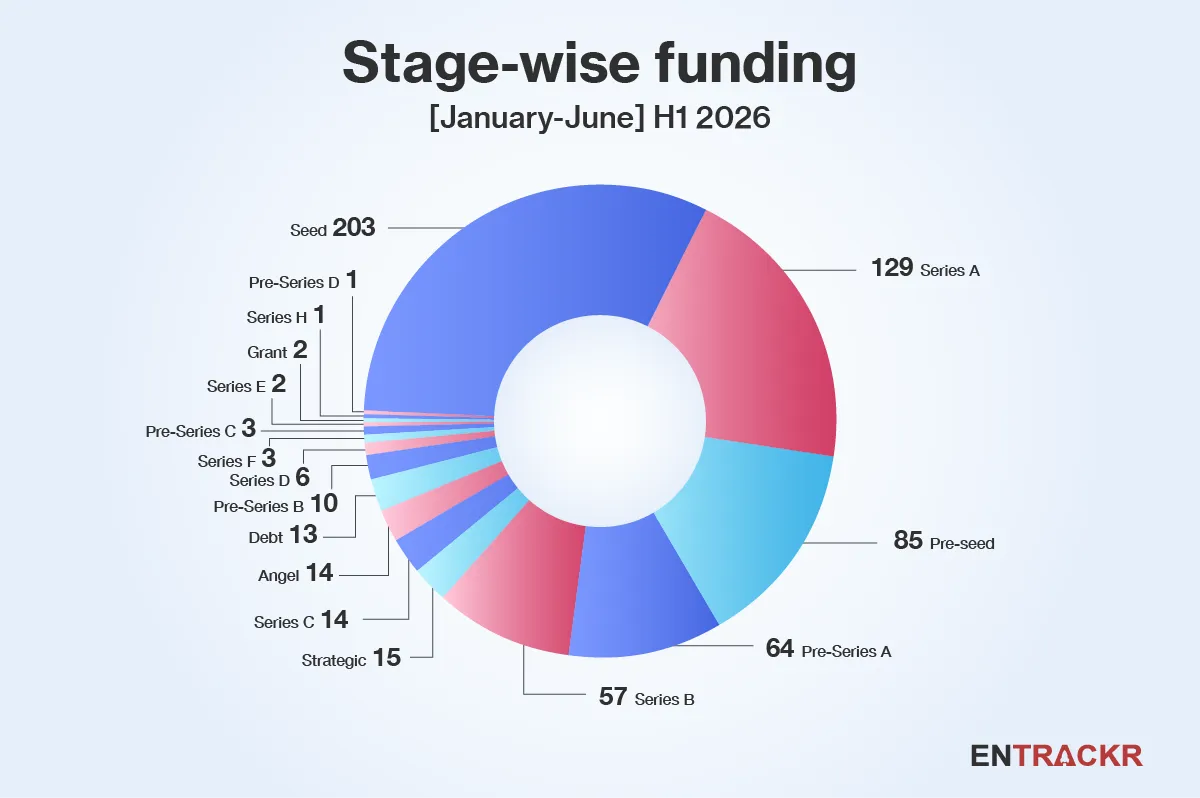

[Stage wise deals]

Series B emerged as the largest funding stage in H1 2026, attracting $2.54 billion across 57 deals, which accounted for 34.42% of the total capital raised during the period. Series A followed with $1.03 billion from 127 deals, while seed-stage startups secured $483.94 million across 202 deals, the highest deal count among all funding stages.

Pre-Series A rounds brought in $175.17 million through 64 deals, whereas pre-seed startups raised $41.31 million across 79 deals. The data indicates that investors continued to deploy larger cheques in relatively mature startups while maintaining steady activity in early-stage funding.

[Layoffs, shutdowns and departures]

Layoffs continued across the startup ecosystem during H1 2026, affecting nearly 2,500 employees across private startups. The total rises to more than 3,600 employees after including listed companies Freshworks and Ola Electric. Livspace announced the largest workforce reduction among private startups, cutting 1,000 jobs, followed by Innovaccer (340), Flipkart (300), and Zupee and Adda247, which each laid off 200 employees. Other startups, including Dream Sports, Pocket FM, 91Trucks, Acko, SuperOps, and Apna Mart, also reduced their workforce during the first half of the year.

Meanwhile, at least nine ventures ceased operations across sectors such as AI, fintech, media, commerce, and D2C.

Leadership churn remained active across the startup landscape, with 54 senior level departures during the period. At the same time, startups recorded 194 key leadership appointments, including Kunal Shah as Global CEO of WhatsApp, Amit Nanda as CEO of BigBasket, Kiran Mani as APAC Head at OpenAI, Kulmeet Bawa as Managing Director of ServiceNow India, Sameer Gandhi as CFO of Cashfree Payments, Deepak Rastogi as CFO of Ola Electric, Anup Purohit as Strategic Advisor at Neysa, and Ankit Sood as CEO of NimbusPost, among others.

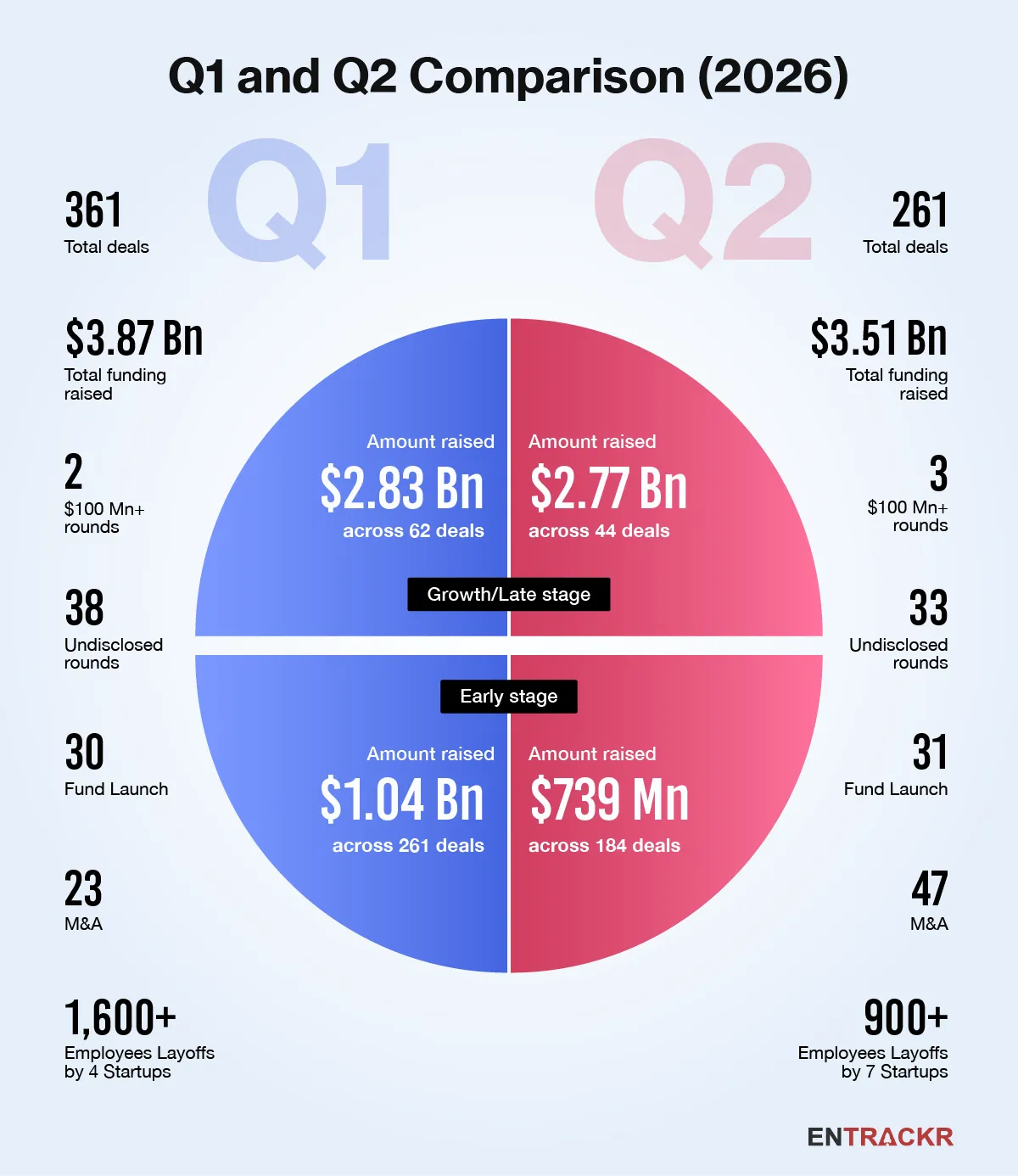

[Q1 vs Q2]

[Trends in H1 2025]

Debt platforms move closer to public markets: The IPO pipeline for digital lending platforms gained momentum with Kissht completing its stock market listing, while Moneyview and Fibe filed their DRHPs. The developments position debt focused fintechs as the next wave of public market candidates.

Delhi EV policy boosts electric two wheeler adoption:Delhi’s new EV policy is expected to accelerate electric two wheeler adoption through purchase incentives, charging infrastructure expansion and a phased transition to EV only registrations for new two wheelers from 2028. The policy could benefit manufacturers such as Ather Energy, Ola Electric and Ultraviolette.

Salon services emerge as the next startup battleground: Salon services have become the latest focus area for startups. New initiatives from Snabbit and NoBroker, along with funding for organised salon chains such as Bodycraft, reflect growing investor interest in tech enabled beauty and personal care services.

Leadership transitions reshape startup ecosystem: The year witnessed several high profile leadership exits and role changes, including Kunal Shah at CRED, Hari Menon from BigBasket, Prabhjeet Singh from Uber India and South Asia, Akash Dongre from Indus Appstore, and Deepinder Goyal and Nandan Reddy from Eternal. The changes point to a broader leadership transition across India’s startup ecosystem.

Jio IPO could lift sentiment for tech listings: The proposed Jio IPO is expected to be one of India’s largest public offerings. A successful listing could attract global investors, set fresh valuation benchmarks for technology companies and encourage more startups to tap the public markets.

[Conclusion]

H1 2026 reflected an evolving startup ecosystem, with funding activity improving alongside stronger investor interest in AI, fintech and other emerging sectors. The period also witnessed steady progress in the IPO pipeline, continued consolidation through acquisitions and several leadership changes across startups. At the same time, new themes such as debt platform listings, EV policy support and salon services emerged during the first six months of the year. As a number of startups prepare for public listings and investors continue to remain selective, H2 2026 is expected to provide greater clarity on the direction of India’s startup ecosystem.

Source link