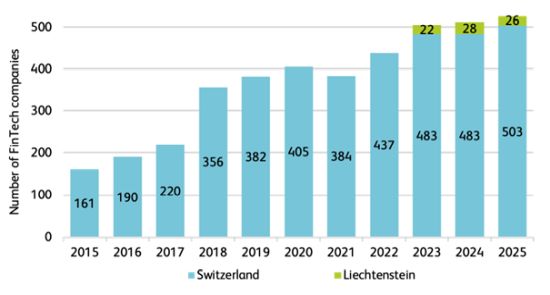

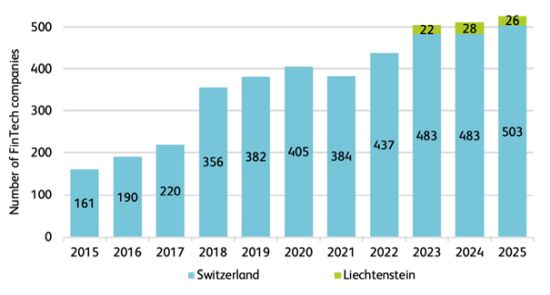

According to the IFZ Fintech study 2026 , there were a total of 529 Fintech companies in Switzerland (503) and Liechtenstein (26) at the end of 2025. This represents a year-on-year increase of 4%. With the exception of a slight decline in 2021, the number of Fintech companies has risen almost continuously since 2015, more than tripling over the period under review. At the same time, annual growth in recent years has been lower than in previous growth phases. The development is characterised by simultaneous market entries and exits: company launches, liquidations, mergers and strategic realignments are largely in balance.

This development points to a new phase in the Fintech ecosystem. After previous years of comparatively stronger growth, consolidation, specialisation and technological repositioning of business models are coming to the fore. Regionally, Fintech activity remains concentrated, with Zurich maintaining its position as the largest location, followed by the canton of Zug.

AI on the rise

Changes in technological composition represent one of the most pronounced developments identified in the study. Analytics, big data, and artificial intelligence have become the largest technology category within the ecosystem, surpassing both process digitisation and distributed ledger technology for the first time in 2025. This shift reflects the growing importance of data-driven financial solutions and the increasing integration of advanced analytical capabilities into Fintech business models. “The growing importance of artificial intelligence is not only due to new start-ups”, says co-author and Head of the Competence Center for Investments at HSLU Thomas Ankenbrand, “existing Fintech companies have also shifted their technological focus towards data- and AI-based applications.”

Distributed ledger technology remains relevant, particularly within infrastructure-related applications. Overall, technological developments point towards a gradual transition to more advanced, scalable, and analytics-oriented innovation structures.

At the product area level, infrastructure became the largest product segment for the first time, ahead of investment management. This highlights the trend of Fintech companies providing technological building blocks for established financial institutions.

B2B- and export oriented

A majority of Fintech companies primarily serve institutional clients and operate beyond domestic markets, highlighting the export-oriented and infrastructure-focused character of Fintech innovation in Switzerland and Liechtenstein. Consumer-focused business models account for a smaller share of the ecosystem and remain comparatively more domestically oriented. Parallel to this development, revenue generation has increasingly shifted towards technology-driven models, with Software-as-a-Service emerging as the dominant monetisation approach over time.

Less venture capital

Switzerland, represented by Geneva and Zurich, continues to rank among the leading global Fintech centres in the IFZ Fintech hub ranking, with both hubs positioned directly behind Singapore, which holds the top position. Despite this strong international standing, venture capital activity declined in 2025 compared with previous peak years. While this development can be observed both globally and in Switzerland and Liechtenstein, it is particularly noteworthy for the Swiss and Liechtenstein financial centres. The underlying drivers remain unclear and constitute an interesting avenue for further research.

Incremental innovation

Recent developments suggest that the adoption of new technologies within financial institutions is primarily incremental rather than disruptive. Since 2010, efficiency indicators of Swiss banks have shown an upward trend, with business volumes, measured by total assets and assets under management, rising relative to costs. This trend should, however, be interpreted with caution, as it is partly driven by external factors such as price effects and structural changes in the banking sector. Although the extent to which these efficiency gains can be attributed directly to Fintech remains difficult to assess, the evidence indicates that banks are pursuing strategies of continuous innovation in close cooperation with IT and technology providers.

(Press release / SK)