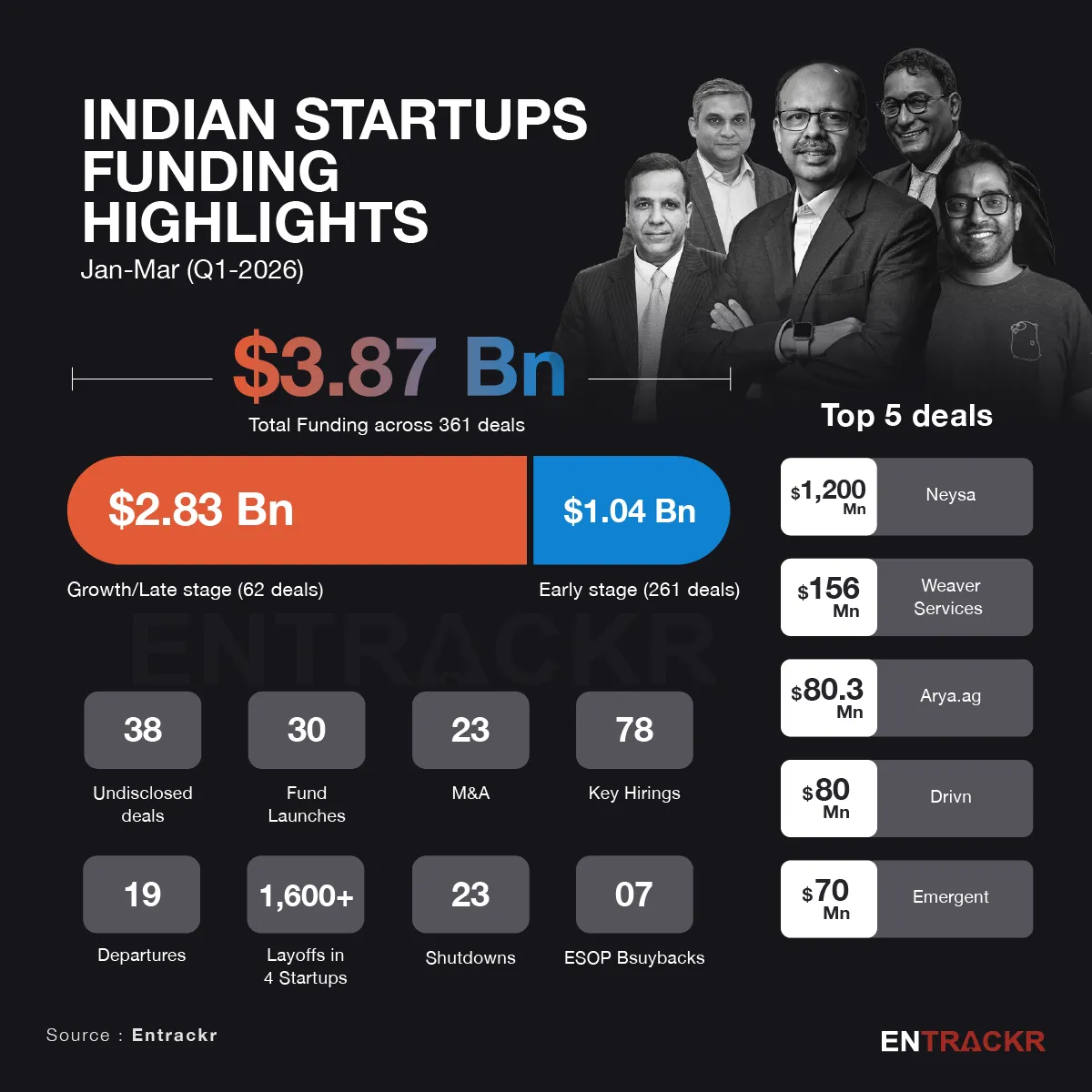

Indian startups saw a sharp rise in funding in Q1 2026 as total funding came close to $4 billion, among the highest quarterly totals in recent years. Neysa’s $1.2 billion round led the surge, while Weaver Services, Arya.ag, Drivn and Emergent also raised large rounds. Early stage funding also stood out in the quarter, as total investments crossed $1 billion, a relatively rare milestone that signals renewed investor appetite at the seed and Series A levels.

The quarter also reflected stress in the ecosystem. Layoffs hit Livspace, Flipkart, Zupee and Dream Sports, while PhonePe paused its IPO plan due to global uncertainty.

Toward the end of the quarter, sentiment improved as a few companies filed DRHPs, which may lead to a pickup in IPO activity in the coming months.

According to data compiled by Entrackr, Indian startups raised approximately $3.9 billion in funding during the first quarter of 2026. This amount included 62 growth and late-stage deals totaling $2.83 billion, along with 261 early-stage deals worth $1 billion. Additionally, there were 38 undisclosed deals during this period.

Q-o-Q and M-o-M trend

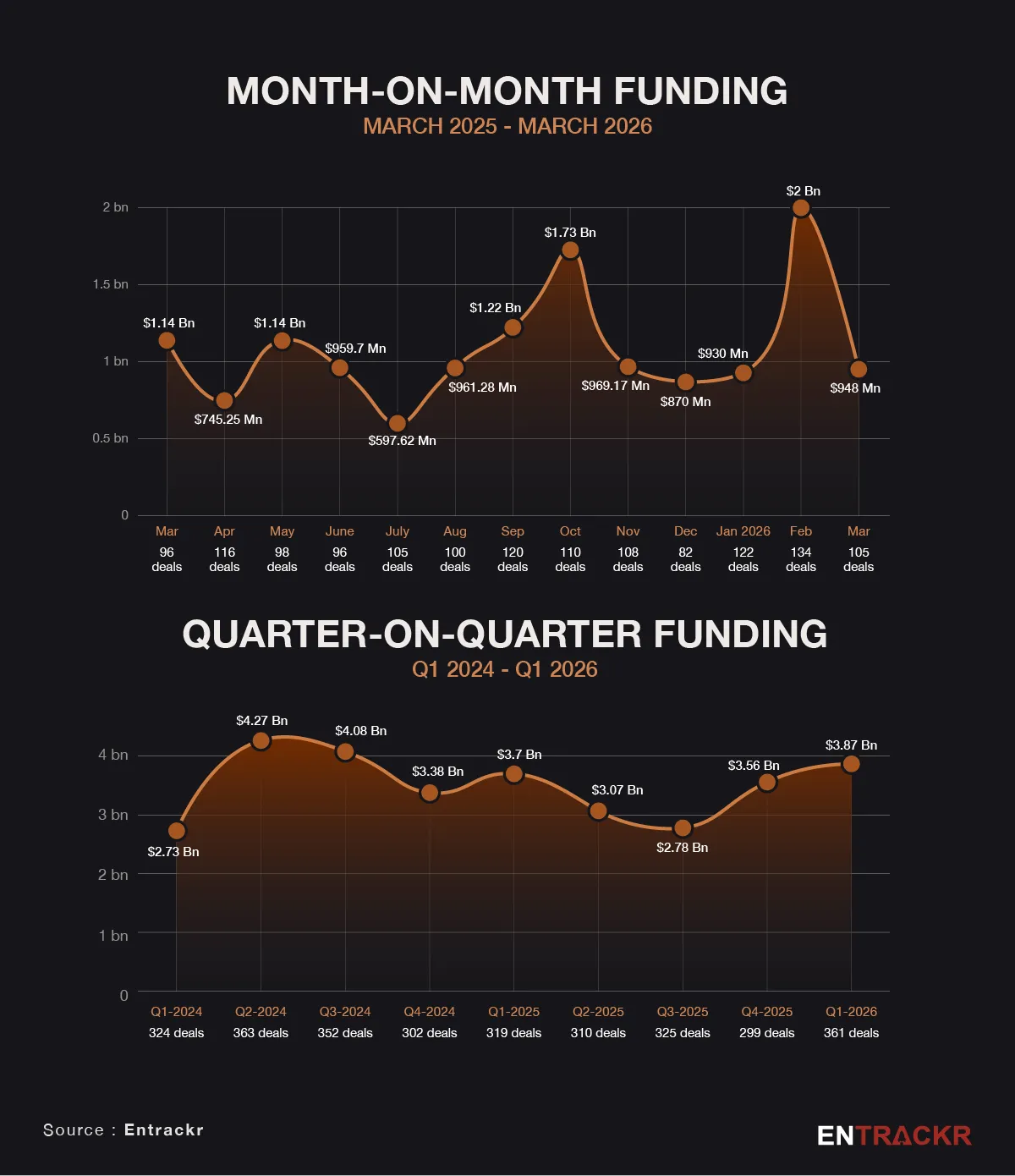

Q1 2026 saw a clear uptick in funding compared to Q4 2025, rising to $3.87 billion from $3.56 billion. This pushed the quarter to its strongest level in a year and reversed the recent slowdown. The momentum was largely driven by February, which recorded $2 billion in funding after a modest $930 million in January, before moderating to $948 million in March. Despite the pullback, March remained just below the $1 billion mark, while February stood out as the peak month of the quarter.

Top 15 growth-stage deals

In the first quarter of 2026, India’s top 15 growth and late-stage deals signalled strong momentum led by large AI bets and sectoral diversity. Neysa topped the list with a massive $1.2 billion Series B round for its AI infrastructure platform, far ahead of Weaver Services, which raised $156 million to expand its affordable housing finance play. Agritech player Arya.ag secured $80.3 million, while EV-focused Drivn also brought in $80 million. Emergent continued the AI push with a $70 million Series B round, and SaaS firm Rocketlane raised $60 million to scale its enterprise delivery platform. IDfy followed with $53 million, while clean-label brand The Whole Truth secured $51 million. Fintech major Juspay raised $50 million, and EV manufacturer Euler Motors added $47 million. Climate-focused lender Ecofy raised $42 million, alongside Mozark at $40 million in the SaaS segment. Foodtech startup Swish secured $38 million for its quick delivery model, while Namdev Finvest raised $37 million in debt. Travel tech platform Atlys rounded out the list with $36 million.

Top 15 early-stage deals

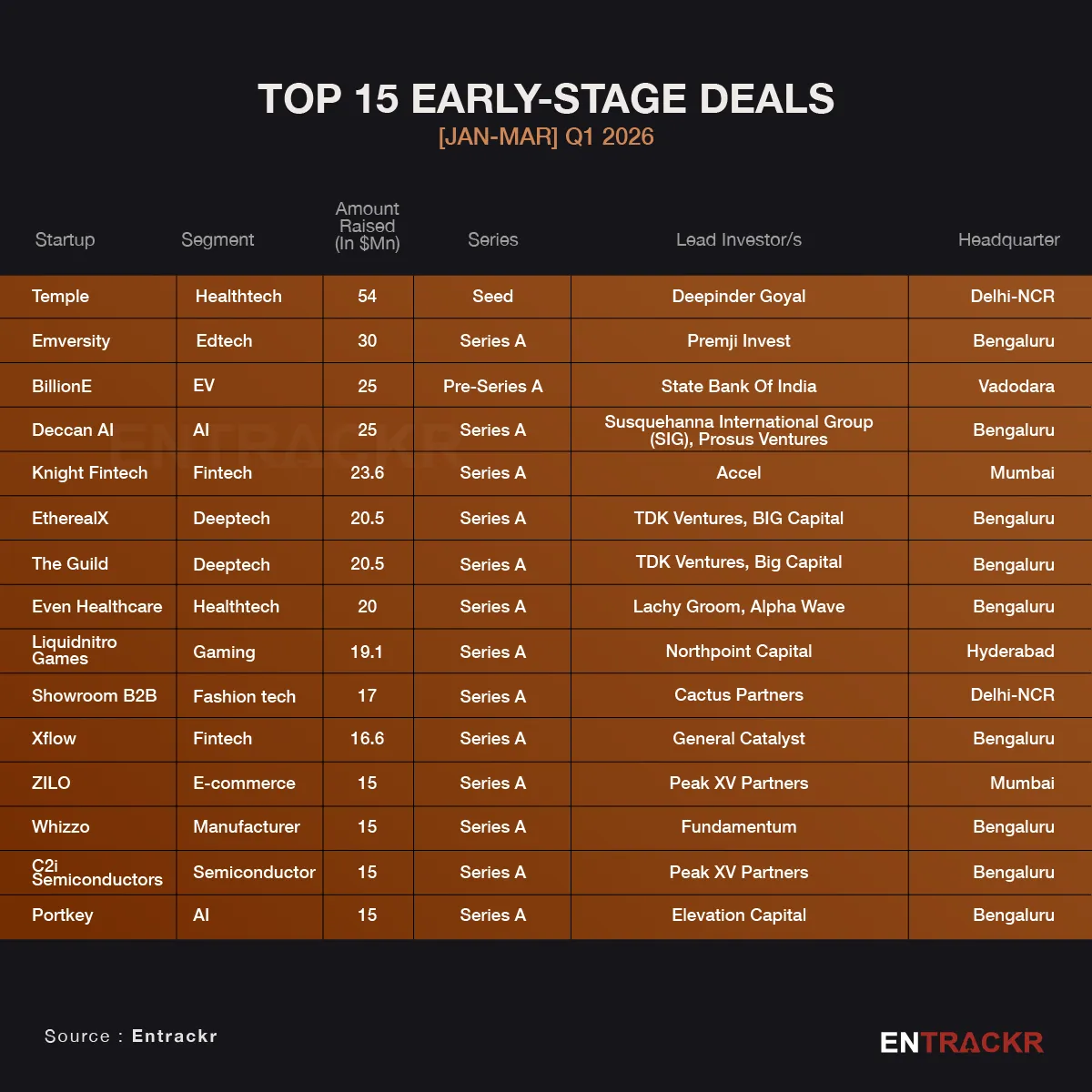

Early-stage activity in Q1 2026 remained strong, led by Temple’s $54 million seed round and Emversity’s $30 million Series A. Most deals clustered in the $15–25 million range, indicating steady Series A momentum.

AI, deeptech, and healthtech dominated funding, with startups such as Deccan AI, EtherealX, The Guild, Portkey, Temple, and Even Healthcare attracting significant interest. Fintech and e-commerce also saw consistent activity through players like Knight Fintech, Xflow, and ZILO.

Overall, the quarter reflected a clear preference for tech-led and scalable models, with Series A emerging as the most active stage.

Mergers and Acquisitions

In Q1 2026, India’s startup ecosystem saw steady acquisition activity across fintech, foodtech, edtech, and consumer brands. Among disclosed deals, Polygon Labs’ $250 million acquisitions of Coinme and Sequence were the largest transactions of the quarter. Marico’s $42 million majority stake in Cosmix and ixigo’s $13.8 million deal in Trenes showed continued interest in consumer and travel segments. In edtech, upGrad remained active through acquisitions of Internshala and Unacademy, while BillDesk’s proposed $70.8 million acquisition of Worldline SA marked a notable move in fintech. Wider consolidation was visible through deals by MakeMyTrip, MedGenome, and Nazara, which reflect strategic expansion across sectors.

City and segment-wise deals

In Q1 2026, Mumbai led in funding with $1.64 billion, which accounted for 42.4% of total capital despite just 36 deals. Bengaluru recorded the highest deal volume at 166 transactions, with $1.21 billion (31.2%), while Delhi-NCR followed with 89 deals worth $631.6 million (16.3%). Hyderabad and Chennai saw lower activity, with 16 and 11 deals that raised $79.5 million (2.05%) and $125.7 million (3.24%) respectively.

In Q1 2026, AI led in funding with $1.48 billion, which accounted for 38.3% of total capital across 51 deals. Fintech followed with 34 deals that raised $538.2 million (13.9%), while Healthtech recorded 35 deals worth $290.3 million (7.49%). E-commerce saw 44 deals with $188 million (4.85%), whereas Deeptech accounted for 28 deals that brought in $105.8 million (2.73%).

Series-wise deals

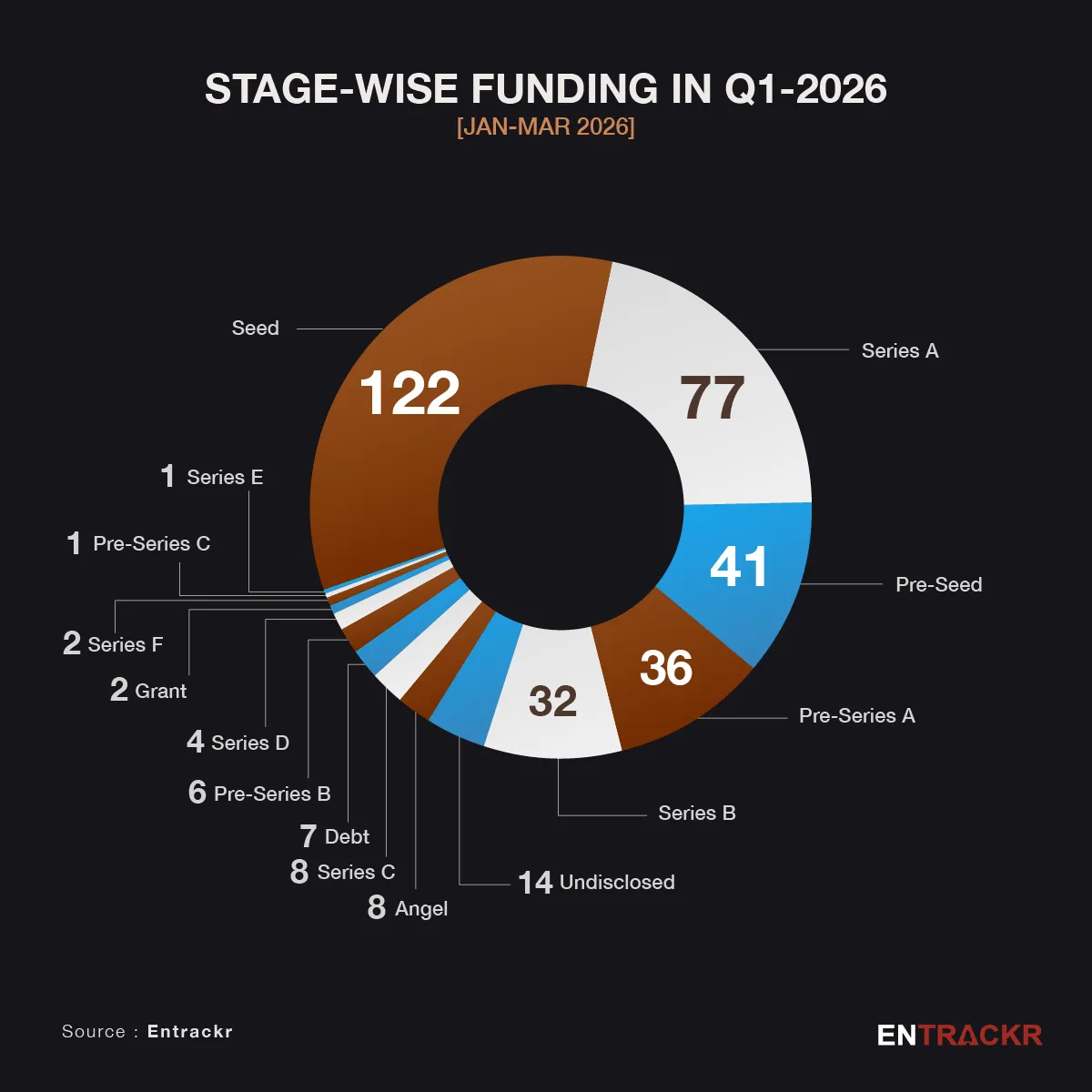

In the latest quarter, India’s startup ecosystem saw a clear skew toward growth-stage capital, led by Series B rounds that brought in $1.82 billion across 32 deals. Early-stage activity remained steady, with 122 Seed deals raising $287.3 million and 41 Pre-seed rounds contributing a modest $22.2 million. Series A also saw strong traction, accounting for $628.2 million across 77 deals, while Pre-Series A funding stood at $108.7 million from 36 deals. Additionally, 14 undisclosed rounds together added $300 million to the overall funding mix.

​​Layoffs, shutdowns and departures

layoffs continued across several Indian startups, which reflected ongoing cost optimization efforts and a push toward profitability. Livspace saw the largest workforce reduction with around 1,000 employees affected, followed by Flipkart with 300 layoffs. Zupee and Dream Sports also trimmed their teams, with 200 and 100 employees impacted respectively.

The quarter also saw three shutdowns – Alle, Pync and Covrzy.

Meanwhile, the startup ecosystem experienced notable departures of top executives in Q1. According to data, 19 top-level executives, including CEOs, CBOs, CFOs, co-founders, managing directors, and presidents, have resigned. During the period, there were 78 key hirings.

Trends

Early-stage momentum: Early-stage startups accounted for around $1 billion in funding, which reflects steady investor interest in new ventures.

Edtech M&A revival: After earlier talks were called off, upGrad and Unacademy have resumed discussions, with upGrad agreeing to acquire the SoftBank-backed firm. The deal includes a break-free clause.

ESOP buybacks return: ESOP buybacks made a comeback in Q1 2026. At least seven startups, including BrowserStack, Innovaccer, Unacademy, and CoinDCX, announced buybacks worth $200 million in total.

Mumbai overtakes Bengaluru: Mumbai-based startups led funding activity and secured 42% of total capital, compared to 31% raised by Bengaluru-based startups.

Conclusion

We expected start up funding to recover strongly in 2026, something that was well on its way till the Trump disruption happened. The quality of growth stage deals will ensure funding remains relatively strong, even as a recalibration is ongoing when it comes to valuations and projections. With exits set to be hit this year due to market weakness, that will also hurt, although India has truly delivered vis a vis other comparable markets. Newer opportunities in climate financing are emerging, besides a renewed interest in EVs and Storage. Expect sizeable bets in these areas soon.

Source link