The round, if completed, is likely to come at a valuation under $1 billion, these people said. Slice’s last known valuation was around $1.3 billion.

“They are in the market to raise, but the valuation will likely take a hit,” a person in the know said. “The company has held talks with venture capital funds but nothing has fructified yet. The West Asia war and the focus on AI has kept some of the big global funds away.”

Last year, Slice had held discussions to raise $250-300 million from a group of financial investors and family offices, as per a board resolution notice, but that process did not materialise.

In October 2024, Slice founder and CEO Rajan Bajaj infused around Rs 71.7 crore ($8.5 million approximately) into the company.

ETtech

ETtech

ET has reviewed a pitch deck shared with investors, outlining projected growth in Slice’s lending, deposits and revenue run rate as it expands its UPI-led credit and digital banking business.

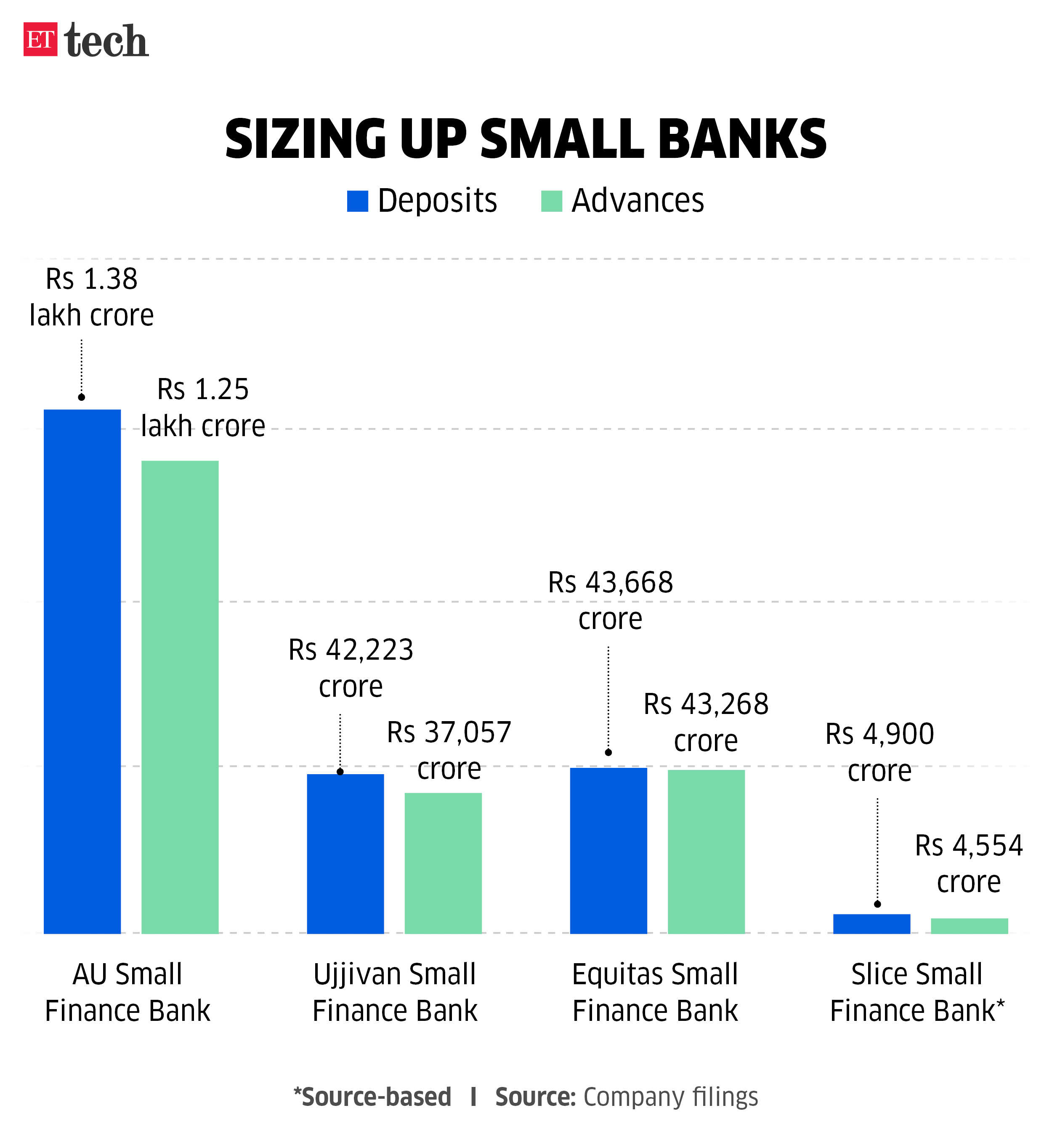

Slice’s lending book has nearly doubled in a year. AUM ( asset under management) hit Rs 4,554 crore in March 2026, up 78% year-on-year and is projected to go up to Rs 8,091 crore by March 2027. The company’s revenue is pegged at Rs 1,300 crore for the year ended March 31, 2026.

Queries sent to Slice on its fundraising plans, valuation expectations and financials did not receive a response.

However, a Slice spokesperson said the company has strengthened its financial position since its merger with Guwahati-headquartered North East Small Finance Bank (NESFB).

“Since the merger in October 2024, we’ve scaled decisively, hitting profitability ahead of schedule and building unit economics that are among the strongest in Indian banking. The business today is larger, leaner and more resilient than it was at the time of the merger. We continue to see strong inbound interest from investors,” the spokesperson said.

Founded as a fintech startup offering credit through prepaid cards, Slice found its core business disrupted in 2022 after the Reserve Bank of India (RBI) banned such products.

The Tiger Global-backed startup then pivoted to its core lending business until the RBI approved the merger with NESFB.

Now operating as a small finance bank (SFB), Slice offers savings accounts, UPI-linked credit cards and a fund management platform, competing primarily as a digital bank against the likes of Equitas SFB and Ujjivan SFB.

In its investor pitch, the company highlights improving unit economics driven by a lower cost of funds, data-led underwriting and deeper engagement across lending, payments and deposits.

Slice is betting that UPI-led credit will structurally reshape the traditional credit card market and help digitally native players gain share from legacy banks over time.

Sectoral stress

The broader SFB sector, however, has faced significant headwinds from rising bad loans and deposit-gathering stress.

A rating report by Icra in December 2025 noted that slippages in the microfinance segment pushed SFBs’ gross bad loans by 120 basis points through March 2025, inching up further to 3.5% by September 2025. “Given the reduced net-interest margins and elevated credit costs, Icra expects SFBs to report a return on assets (RoA) of 1.0-1.2% in FY2026, versus 1.3% in FY2025, followed by some improvement in FY2027,” it said.

An investor who has closely tracked the space said, “There are still lingering concerns on the valuation for Slice SFB and how this niche banking business will build up over the coming months.”

The fundraising discussions come at a time when capital has grown more selective for fintech startups, with investors increasingly prioritising sustainable growth, asset quality and a clear path to profitability.

Also Read: Early-stage funding value ticks up 46%, but numbers decrease

Looking for a turnaround

Several late-stage startups have seen valuation resets over the past two years as public market benchmarks tightened and global liquidity conditions shifted.

India’s neo-banking space broadly has failed to gain traction. Tiger Global-backed Jupiter’s bid to pick up a minority stake in SBM India fell through, while neobanking startup Fi recently shut down its banking operations.

Slice secured a coveted banking licence after its merger with the beleaguered NESFB, but has yet to attract significant venture investment since the deal closed.

According to its FY25 annual report, Slice posted total income of Rs 603 crore against total expenses of Rs 820 crore, resulting in a net loss of Rs 216 crore.

Also Read: Slice Small Finance Bank turns profitable on monthly basis; targets IPO in 3–4 years

A credit note by Care Edge in December 2025 said the bank reported a provisional profit of Rs 7 crore, with pre-Esop (employee stock ownership plan) profit at Rs 43 crore for the first half of FY26.

The bank’s net non-performing assets (NPA) stood at 4.2% as of September 30, down from 8.4% as of March 31, 2024.

“The post-merger portfolio is exhibiting better performance, but seasoning remains limited given the rapid pace of recent disbursements,” the note said.