Geographical and temporal trends in AI health startup formation

The evolution of AI health startups illustrates a dramatic rise in innovation and activity, followed by a notable decline in recent years. Geographic analysis of AI health startups further underscores disparities in activity and resource distribution. The United States (U.S.) leads the sector with 1609 startups and over $38 billion in funding, followed by China, which shows considerable activity and investment. The map in Fig. 1 reveals a high concentration of startups in North America, Europe, and parts of Asia, particularly in urban and economically advanced clusters. These clusters benefit from proximity to venture capital, specialized talent, and supporting industries, creating favorable conditions for startup growth. Conversely, the scarcity of startups in underrepresented regions, such as Africa and South America, points to untapped potential that could be unlocked through targeted investments and ecosystem-building efforts, including regulatory support, access to capital, and digital infrastructure. Our geographic analysis of AI health startup formation parallels the findings reported in the Global AI Index (https://www.tortoisemedia.com/data/global-ai#rankings), which highlights the concentration of AI capabilities in a few dominant countries, most notably the United States and China, where robust ecosystems, strategic investment, and innovation infrastructure continue to drive AI leadership.

World map showing the location of 3807 AI health startups founded between 2010 and 2024, with each red dot representing one or more startups in that location. Dense clustering is evident in North America, particularly in the United States, around Silicon Valley, Boston, and New York metropolitan areas. European clusters are concentrated in the United Kingdom, Germany, France, and Switzerland. Asia shows significant activity in China, India, Israel, South Korea, and Japan. Notable gaps exist in Africa, South America, and Central Asia, highlighting geographic disparities in AI health innovation. Australia and New Zealand demonstrate a moderate startup presence. The concentration patterns reflect proximity to venture capital, research institutions, and established healthcare innovation ecosystems.

The maps also highlight the role of economic clusters in supporting AI health startups. In the U.S., for instance, dense clusters around Silicon Valley, Boston, and New York emerged as hubs of innovation, underscoring the advantages of geographical proximity to venture capitalists, research institutions, and specialized industries. Similarly, European clusters around London, Berlin, Paris, and Zurich reveal a strong focus on healthcare innovation. These innovation hubs provide access to essential resources, enabling startups to thrive in highly competitive markets. The lack of similar clustering in developing regions, however, poses challenges for local startups, which may struggle to access the resources and networks necessary for sustained growth and scalability.

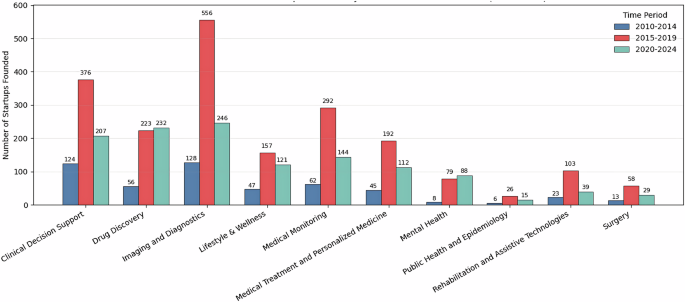

Table 1 shows the number of AI health startups for each medical domain. Figure 2 illustrates the number of AI startups founded across three time periods, 2010–2014, 2015–2019, and 2020–2024, segmented by medical domain. This specific segmentation into 2010–2014, 2015–2019, and 2020–2024 reflects distinct phases in the evolution of AI in healthcare. The years 2010–2014 represent the foundational stage, when traditional machine learning, limited clinical datasets, and slow institutional adoption constrained AI adoption in healthcare. The 2015–2019 period marks a significant shift, characterized by the widespread adoption of deep learning, the release of large medical datasets, clearer regulatory pathways, and substantial growth in venture capital investment, all of which enabled more advanced diagnostic and predictive solutions. Finally, the 2020–2024 period corresponds to the modern era of AI in healthcare, shaped by the acceleration of digital health during COVID-19, broader use of telemedicine, increasing reliance on privacy-preserving machine-learning techniques, and the emergence of foundation models with far greater capabilities48.

Bar chart showing the number of startups founded across ten medical domains during three time periods: 2010–2014 (blue), 2015–2019 (red), and 2020–2024 (teal). Imaging and Diagnostics experienced the highest growth, with 556 startups founded during 2015–2019, followed by Clinical Decision Support (376 startups) and Medical Monitoring (292 startups). A substantial decline in new startup formation is evident across all domains during 2020–2024, except for Imaging and Diagnostics and Drug Discovery, which maintained moderate activity. Emerging domains, including Mental Health, Public Health and Epidemiology, and Rehabilitation and Assistive Technologies, show limited but increasing activity over time. Numbers above bars indicate startup count per period.

From 2010 to 2019, the number of startups increased fourfold, from 512 to 2062, driven by substantial investments and widespread optimism about AI’s potential to revolutionize healthcare. This growth period also witnessed significant diversification across medical domains, with Clinical Decision Support, Drug Discovery, Imaging and Diagnostics, and Medical Monitoring taking center stage. Notably, Imaging and Diagnostics emerged as the leading category, emphasizing the growing focus on precision medicine and early disease detection. Emerging categories such as Mental Health, Public Health and Epidemiology, and Rehabilitation and Assistive Technologies have seen increased activity in recent years, indicating a broadening of AI applications in healthcare. However, the sharp decline in startup entry after 2020 suggests market saturation, shifting investor priorities, and broader economic pressures, indicating a pivotal moment for the sector. As of 2024, about 4% (154) of the startups have been acquired, while 8% (319) have ceased operations. Among the startups that exited the industry, those in the surgery segment had the highest exit rate at 32%, followed by 16% in lifestyle and wellness, and 11% in rehabilitation and assistive technologies. All other segments reported exit rates of 9% or lower.

Investment and validation of AI health innovations

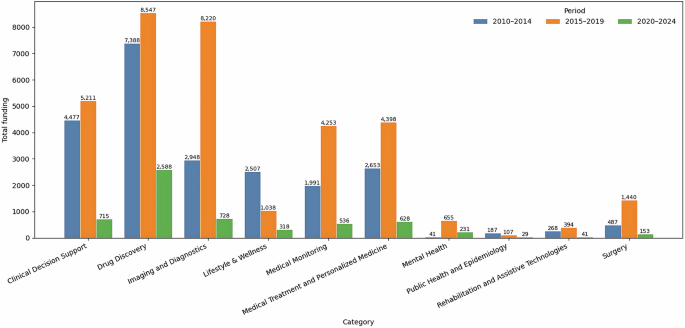

To understand the landscape of AI health innovations and the level of complexity associated with each, we analyzed the distribution of startups and their investment funds across varying levels of AI systems complexity. Figure 3 shows that 3807 AI health startups have raised a total of $63.17B since 2010. Most notably, 2062 startups founded from 2015 to 2019 have received $34.26B in total. Based on our detailed analysis across AI systems complexity levels, imaging and diagnostics ($11.87B) and drug discovery ($18.5B) attract the highest levels of funding, largely due to their compatibility with high and advanced complexity AI systems, respectively, especially deep learning in medical imaging and predictive models for pharmaceutical R&D. In contrast, moderate-complexity AI applications such as those supporting clinical decision support ($10.4B) and medical monitoring ($6.78B) are more widely adopted, suggesting that assistive tools designed to augment rather than replace human decision-making more easily integrate into clinical workflows and overcome fewer regulatory hurdles. Finally, the distribution of private equity funding remains uneven across AI complexity levels and medical domains. Lifestyle and wellness ($3.8B) appear to benefit from Assistive AI focused on personalization and guidance, while mental health, public health, epidemiology, and rehabilitation remain significantly underfunded. Additionally, only 38 startups have gone public, primarily in clinical decision support, drug discovery, imaging and diagnostics, and medical treatment, with 7–9 listings per category. The overall investment trend reveals a persistent gap between social health priorities and private investment flows, suggesting targeted funding and policy interventions may be needed to ensure more equitable AI development in healthcare.

This figure presents a bar chart showing total funding (in millions USD) raised by AI health startups across ten medical domains during three time periods: 2010–2014 (blue), 2015–2019 (orange), and 2020–2024 (green). Drug Discovery, Imaging, and Diagnostics attracted the highest total funding, with peak investment during 2015–2019 across most domains. The 2020–2024 period shows a marked decline in funding across all categories, with Imaging and Diagnostics suffering the highest drop. Mental Health, Public Health and Epidemiology, and Rehabilitation and Assistive Technologies received comparatively minimal funding across all periods. Total values are displayed above each bar segment.

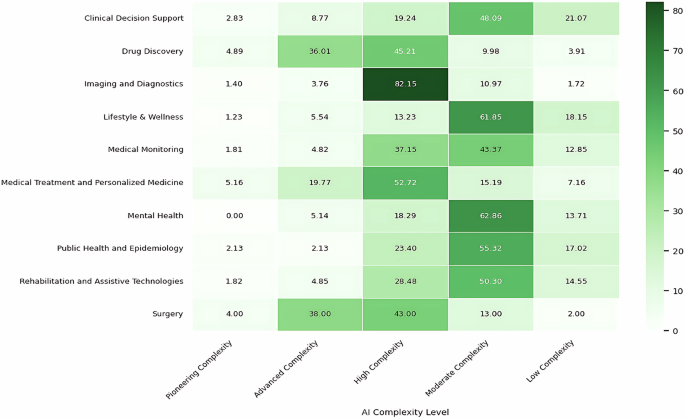

Figure 4 shows the proportion of startups operating in each domain across the AI complexity spectrum, from low to pioneering. The map reveals that high and moderate AI system complexity dominate most categories. A small proportion of startups in drug discovery, medical treatment, personalized medicine, and surgery are increasingly shifting towards advanced, pioneering complexity, indicating the need for robust AI knowledge and infrastructure. This is unsurprising given the demands of multimodal and continuous learning systems for integrating diverse datasets, such as genomic and biochemical data, and for operating with minimal human intervention. Next, imaging and diagnostics demonstrates a significant association with high complexity, reflecting the advanced capabilities required to analyze unstructured data such as medical images12. These insights underscore the technological and resource-intensive barriers to entry in the health sector, emphasizing the importance of innovation and expertise for startups aiming to succeed in these AI-driven medical domains. Six other domains, including clinical decision support, lifestyle and wellness, and medical monitoring, lean towards moderate to high complexity, reflecting their reliance on structured data and machine learning techniques for practical applications. The map and industry data reveal a nuanced landscape: startups are predominantly deploying moderately to highly complex AI in core technical domains, while deployments in consumer and population health are more cautious. Operational and infrastructure use cases are increasingly validated in practice, though broader adoption hinges on robust governance and strategic ecosystem partnerships26.

Heatmap showing the percentage of startups (n = 3807) operating at each AI complexity level across ten medical domains. Color intensity represents the proportion of startups, with darker green indicating higher concentration. Imaging and Diagnostics shows the highest concentration in High Complexity (82.15%), followed by Medical Treatment and Personalized Medicine (52.72%), reflecting the prevalence of deep learning for medical images and unstructured data analysis. Drug Discovery and Surgery demonstrate substantial representation in Advanced Complexity (36.01% and 38.00%, respectively), indicating adoption of multi-modal AI systems. Lifestyle & Wellness and Mental Health predominantly operate at Moderate Complexity (61.85%, 62.86%, respectively), suggesting a focus on assistive AI tools that augment clinical workflows with human intervention. Clinical Decision Support, Medical Monitoring, Public Health and Epidemiology, and Rehabilitation and Assistive Technologies show balanced distribution across Moderate to High Complexity. Pioneering Complexity remains minimal across all domains (

While the recent decline in startup activity might indicate emerging challenges, regulatory developments provide a contrasting narrative of progress. Since 1995, the U.S. Food and Drug Administration49, has approved 1,016 AI/ML-enabled medical devices, with 989 of those approvals occurring in the past decade. FDA approvals have increased significantly, particularly in fields such as radiology (766 devices) and cardiovascular care (103 devices). Consistent with the landscape of AI health startups shown in Fig. 4, the advancement of FDA-approved medical devices reflects the maturation of AI technologies at moderate and high complexity levels and their alignment with stringent regulatory standards, which are critical for widespread adoption. This pattern is evident in the distribution of devices across AI systems complexity: the vast majority fall into Assistive AI and Perceptual AI, as shown in Table 2, which together account for over 97% of all approvals. These complexity levels represent systems that support or augment clinical tasks using structured or unstructured data, such as imaging, and align with well-established clinical workflows.

In contrast, more advanced systems, such as Integrative AI and Autonomous-Agentic AI, remain rare, each representing less than 1% of approvals. Their limited presence underscores both the technical and regulatory challenges associated with real-time adaptability and multi-modal data integration50. In Table 3, among the top 10 companies with the most devices receiving FDA approvals, six are AI health startups founded between 2011 and 2016. Overall, the FDA approval landscape mirrors startup activity, emphasizing mature, targeted AI applications while highlighting cautious progression toward more complex and autonomous systems.

Table 4 maps detailed investment patterns across healthcare application areas and AI systems complexity levels, revealing a distinctly non-linear and context-specific relationship between technological sophistication and funding. Our analysis indicates only a weak positive correlation between overall AI complexity and total funding, suggesting that higher technical sophistication alone does not systematically translate into greater investment. Instead, funding patterns appear to be shaped by the interaction between complexity and domain-specific characteristics, including data structure, regulatory exposure, clinical adoption barriers, and commercialization readiness41. In some cases, increasingly complex AI systems coincide with greater capital inflows, while in others, investment peaks at moderate complexity and declines as systems become more technically advanced or autonomous. These findings emphasize that AI capability should be interpreted alongside the practical and institutional realities of each healthcare subdomain.

Based on Table 4, the concentration of investment and innovation in imaging and diagnostics startups (the second-highest total funding raised after drug discovery) can be better understood through the lens of moderate- to high-complexity AI systems. These domains often leverage convolutional neural networks and other deep learning architectures that are well-suited to standardized, high-resolution imaging data and benefit from relatively mature regulatory pathways in radiology. This alignment between technical capability, data structure, and regulatory clarity lowers barriers to clinical integration and supports investor confidence. In contrast, domains that demand more advanced system integration or real-time decision-making, such as personalized medicine or surgical robotics (the second- and third-highest funding raised at the advanced complexity level after drug discovery), often require more complex AI architectures and higher capital intensity. These higher-complexity tiers not only entail greater development risks but also create entry barriers for clinician-founded ventures that may lack advanced computational expertise. As a result, these areas tend to see more frequent partnerships with technical co-founders or institutional collaborators, particularly hospitals and clinical research centers, who help bridge the validation and implementation gaps. These patterns illustrate how AI system complexity interacts with data availability, regulatory maturity, and human capital to shape innovation trajectories across different healthcare domains.

The pivotal role of founder experience and team composition

In addition to the challenges of securing investment and navigating technological and regulatory barriers, access to human capital with relevant, diverse experience, particularly at the founding level, is a strategic resource for AI health startups. Founders play a pivotal role in early-stage decision-making, network formation, and shaping the company’s overall direction. Teams with complementary expertise are better positioned to adapt to uncertainty, secure investor confidence, attract partnerships with healthcare institutions, and incorporate ethical, clinical, and technical considerations into product development and deployment51,52.

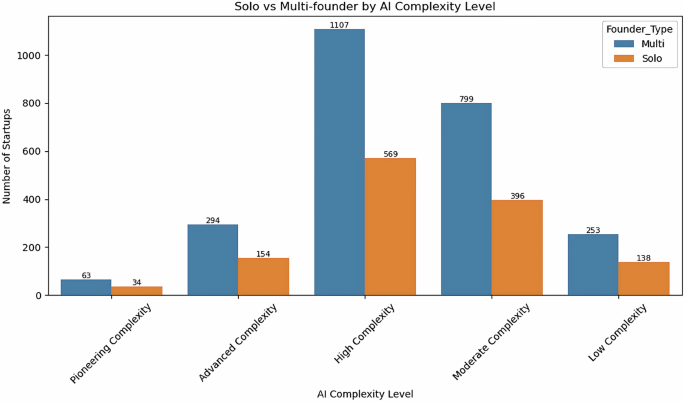

Figure 5 reveals important insights into the founding structures of AI healthcare startups. Of the 3807 startups, 2516 (66.1%) were established by multi-founder teams, while 1291 (33.9%) were initiated by solo founders. Notably, this preference for team-based founding is consistently observed across all levels of AI complexity, with approximately 65% of startups at each tier launched by founding teams. This distribution reflects a strong tendency toward collaborative entrepreneurship in this sector, echoing findings from the broader literature on high-tech and healthcare startups53,54,55. Such a team-based approach is often necessary to address the interdisciplinary challenges of human-AI integration in healthcare56. Effectively navigating these challenges requires the convergence of diverse forms of expertise, including medicine, data science, software engineering, and business management. At the same time, teams composed of such varied backgrounds may also be vulnerable to interpersonal conflict, which can hinder collaboration and compromise decision-making.

Bar chart comparing the number of solo-founded (orange) and multi-founder (blue) startups across five AI complexity levels. Multi-founder teams consistently outnumber solo founders across all complexity tiers, representing approximately 66% of all startups (2516 multi-founder vs. 1291 solo-founder ventures). The pattern remains remarkably consistent across complexity levels: High Complexity shows the most enormous absolute numbers (1107 multi-founder, 569 solo), followed by Moderate Complexity (799 multi-founder, 396 solo). Advanced Complexity startups show a 2:1 ratio (294 multi-founder, 154 solo), while Pioneering Complexity demonstrates the smallest cohort (63 multi-founder, 34 solo). This consistent preference for team-based founding across all levels of AI complexity suggests that collaborative entrepreneurship is fundamental to AI health ventures, regardless of technological sophistication. Numbers above bars indicate the startup count for each category.

The formation of founding teams is a strategic response to the multifaceted demands of launching an AI health venture, which often operates within highly regulated, technically sophisticated, and clinically sensitive environments. By combining clinical, technical, and managerial perspectives from the outset, team-based startups are more likely to align their innovations with market needs and regulatory requirements. Additionally, teams with diverse experiences can benefit from access to broader professional networks, more funding opportunities, and a greater capacity for iterative problem-solving. Founding teams also confer distinct advantages in terms of strategic direction, resource acquisition, and organizational resilience. Collectively, these factors—complementary expertise, diverse professional experience, and strategic and organizational strengths—contribute to the scalability and sustainability of AI health startups, positioning founding teams as a critical asset in the venture creation process.

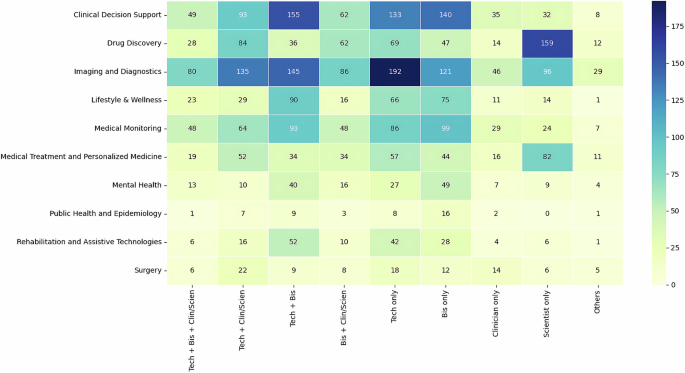

Figures 6 and 7 present the professional composition of founding teams and solo founders from 3807 startups across medical domains and AI complexity levels. The data reflects not just the experts in the founding teams but the dominant professional backgrounds shaping each startup’s foundation. In many cases, teams are composed entirely of individuals with the same professional background, while others span technical, business, clinical, and scientific expertise.

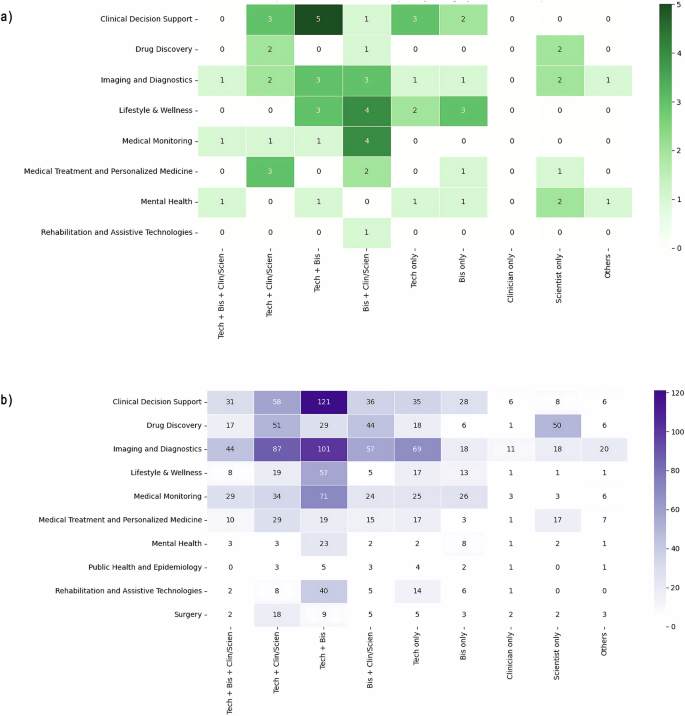

Heatmap showing the distribution of 3,807 AI health startups by founders’ professional backgrounds and medical domain. Color intensity indicates startup count. Technical and business expertise dominate across most domains, with technical-cum-business combinations being the most common. Scientist-only founders focus on Drug Discovery, Medical Treatment, and Personalized Medicine. Clinical practitioners remain underrepresented in founding roles across all medical domains, with business and technical founders significantly outnumbering clinicians in leadership positions.

Heatmap showing the distribution of 3807 AI health startups by founder professional background and AI complexity level. Color intensity indicates startup count. High-Complexity startups are predominantly founded by technical founders, particularly technical-only founders or those with technical backgrounds combined with business or scientific and clinical expertise. Moderate Complexity ventures show the highest concentration of founders with technical-business and business-only backgrounds. Startups at the Advanced and Low Complexity levels exhibit a broad range of expertise, whereas clinical practitioners remain underrepresented across all levels of complexity.

Our descriptive analysis shows that most AI health startups are co-founded by two or more individuals, with an average team size of 2.14 (SD = 1.15). In Fig. 6, technical expertise is the most common foundation for startup formation, either combined with business expertise, as seen in 663 (17%) startups, or as the sole domain of expertise in 698 (18%) startups, out of which 410 (11%) are solo-founder startups and 288 (8%) are team-based startups. This pattern underscores the central role of technical capability in shaping the early direction of AI health ventures, especially involving highly complex AI systems in medical domains such as clinical decision support, imaging, and diagnostics. Business expertise is the next most common professional background among founders. Of the 631 (16.6%) startups led by business-only founders, 454 (12%) are solo-founder startups, while only 177 (4.6%) are team-based startups.

In contrast, clinical experts, particularly founders with direct patient-care experience, play a more limited role. In Fig. 6, 178 startups were founded by clinicians only, while 135 of these were by solo clinician-founders, less than 5% of the total sample. Although clinical insight is essential for healthcare innovation, founding teams tend to rely more heavily on medical scientists with academic or research backgrounds. Specifically, scientist-only teams accounted for 161 (4.2%) startups, while solo scientist-founders accounted for 267 (7%).

Figure 7 shows that AI health startups involved in high-complexity AI systems are predominantly founded by technical-only (329) or technical with business (233) or scientific and clinical (253) expertise. Moderate-complexity ventures show the highest concentration of founders with a technical-business background (278) and a business-only background (257). Clinical practitioners remain underrepresented across all complexity levels, while advanced and low complexity startups demonstrate diverse expertise that is relatively well represented.

The two figures (Figs. 6 and 7) indicate that AI health startups generally include technical and scientific expertise, with business skills commonly present and clinical expertise less frequently or selectively involved in team composition. This pattern may be influenced by factors such as limited entrepreneurial training for clinicians, time constraints, or regulatory requirements. It also highlights the growing importance of scientific research and data science in developing AI-based healthcare solutions. These findings are consistent with survey results57, which show that a higher proportion of researchers (37% of 2284 respondents) than clinicians (26% of 1007 respondents) have used AI tools for work-related purposes.

Moreover, the underrepresentation of clinician-exclusive or clinician-dominant teams may affect the alignment of these AI solutions with real-world clinical needs and workflows. While scientists and technologists can provide the foundational tools for innovation, the absence of front-line healthcare practitioners in leadership roles may lead to a disconnect between problem identification, technical solutions, and patient care outcomes. To assess whether the low representation of clinicians simply reflects investor selection (i.e., investors favoring teams with stronger technical/business profiles), we conducted a split-sample analysis comparing funded and non-funded AI health startups. If investor screening were the primary driver, we would expect clinician under-representation to be concentrated among funded firms; instead, the observed patterns remain qualitatively stable, with clinically involved teams present at all funding levels rather than systematically excluded. Thus, our data not only highlight current trends in founding team composition but also raise important questions about how entrepreneurial ecosystems can better support clinician involvement to ensure the clinical relevance and adoption of AI healthcare technologies.

Gendered patterns in founding structures and expertise across AI health startups

Table 5 provides a gender representation among founders of AI health startups. Overall, male founders overwhelmingly dominate the landscape, comprising 6872 individuals (84%), compared to 1293 female founders (15.8%). Although the proportion of women remains low, the 15.8% figure falls within the 10–15% range reported in comparable datasets of startups founded from 2010 onwards58,59,60,61. In Dowd’s58 report, women comprised just 13.2% of startup founders in 2023, which was the lowest since 2018. Among industry sectors, healthtech had the highest percentage of female founders.

Further disaggregation by founder expertise reveals meaningful variation in gender representation across domains. Women are most represented among scientific founders, comprising 20.1%, reflecting the growing participation of women with advanced degrees, particularly PhDs in biomedical and life sciences. Business and clinical founders follow with 18.1% and 16.8% female representation, respectively. Strikingly, technical founders exhibit the lowest female participation rate at 10.7%, despite being the largest group driving AI health ventures.

Nevertheless, the continued underrepresentation of expertise among female founders, particularly in technical founding roles, calls for proactive, ecosystem-level interventions, such as mentorship programs, funding opportunities, and institutional support structures, to sustain and amplify female participation in shaping the future of AI in healthcare. These disparities also raise important considerations for building more diverse founding teams capable of developing equitable and context-sensitive healthcare technologies51,55.

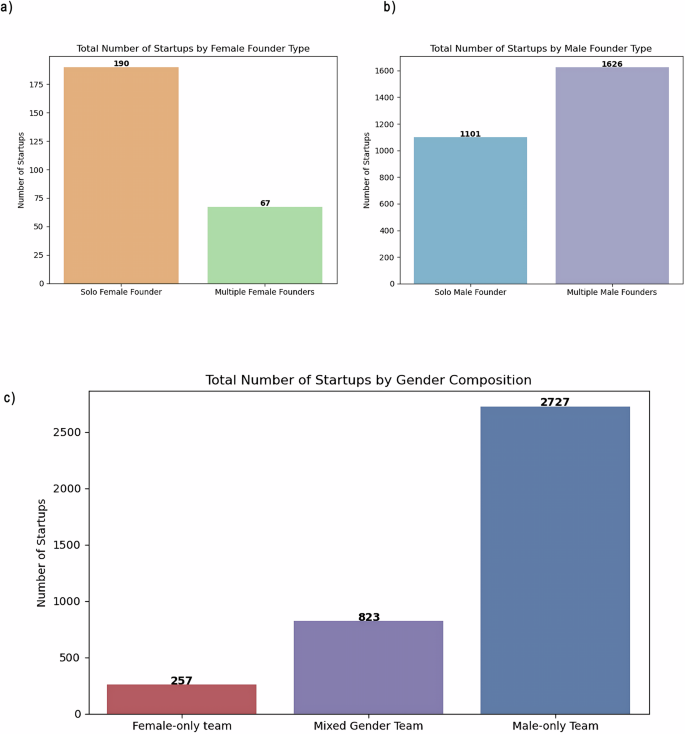

Further analysis of gender composition across AI health startups in Fig. 8a–c reveals a pronounced skew toward male-only founding teams and solo male founders, who together account for approximately 71.6% of all startups in the sample. In contrast, mixed-gender founding teams represent about 21.6%, while startups founded exclusively by women comprise just 6.75% of the total, highlighting the persistent gender imbalance in the entrepreneurial landscape.

a Distribution of startups by gender composition showing male-only teams comprise the majority (2727 startups, 71.6%), followed by mixed-gender teams (823 startups, 21.6%), and female-only teams (257 startups, 6.75%). b Female-only startups by founding structure reveal a strong skew toward solo entrepreneurship, with 190 solo female founders (74%) compared to only 67 multi-female founder teams (26%). c Male-only startups demonstrate more balanced founding structures, with 1626 multi-male founder teams (60%) and 1101 solo male founders (40%). The differences in founding patterns between female-only and male-only ventures highlight the distinct challenges men and women face in AI health entrepreneurship.

When disaggregating by founding structure, the pattern is especially notable among 257 female-only startups: 74% of exclusively female-founded ventures are led by solo founders, compared to just 26% involving multiple female founders. This contrasts with 2727 male-only startups, where founding structures are more balanced: 40% are led by solo male founders, and male teams co-found 60%. These trends suggest that women in AI health entrepreneurship are not only underrepresented but also more likely to pursue solo ventures, potentially reflecting broader structural barriers to team formation, resource access, or professional networks.

Domain-specific gender patterns (Fig. 9a, b)

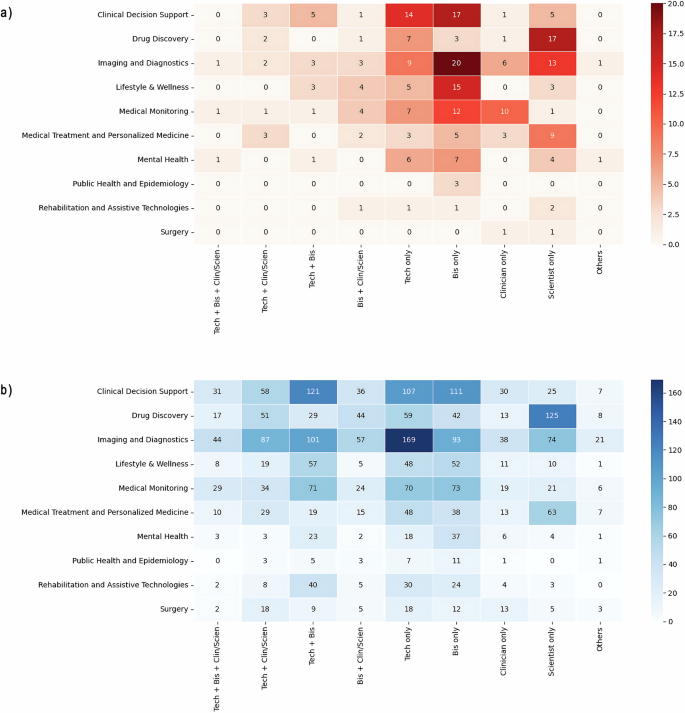

Figure 9a, b presents the distribution of female-only and male-only AI health startups across medical domains, combining both solo and team-based founders. A strong gendered concentration emerges, with both female- and male-only startups being heavily represented in Clinical Decision Support and Imaging and Diagnostics. However, female-only startups are more frequently led by founders with business-only backgrounds, while technical founders predominantly lead male-only startups. This divergence in founders’ expertise suggests gender differences in pathways into AI healthcare innovation. This is consistent with broader research highlighting gendered differences in technical versus managerial entry into entrepreneurial ecosystems53,54.

a Female-only startups (n = 257) show concentration in Clinical Decision Support and Imaging and Diagnostics, with business-only founders (dark red cells) being most prevalent. Scientist-only founders appear prominently in Drug Discovery and Medical Treatment. Clinical-only founding teams are notably sparse, with Medical Monitoring showing the highest count at 10 founders. b Male-only startups (n = 2727) demonstrate substantially higher absolute numbers across all domains and founder types. Technical-only founders (dark blue cells) dominate in Imaging and Diagnostics (169) while scientist-only founders concentrate in Drug Discovery (125). Technical-business combinations are most common in Clinical Decision Support (121) and Imaging and Diagnostics (101). The comparison reveals that female-only startups are more focused on business-led ventures. In contrast, male-only startups exhibit stronger representation of technical backgrounds, suggesting different experiential pathways into AI health entrepreneurship.

Founding structures—female startups (Figs. 10a and 11a)

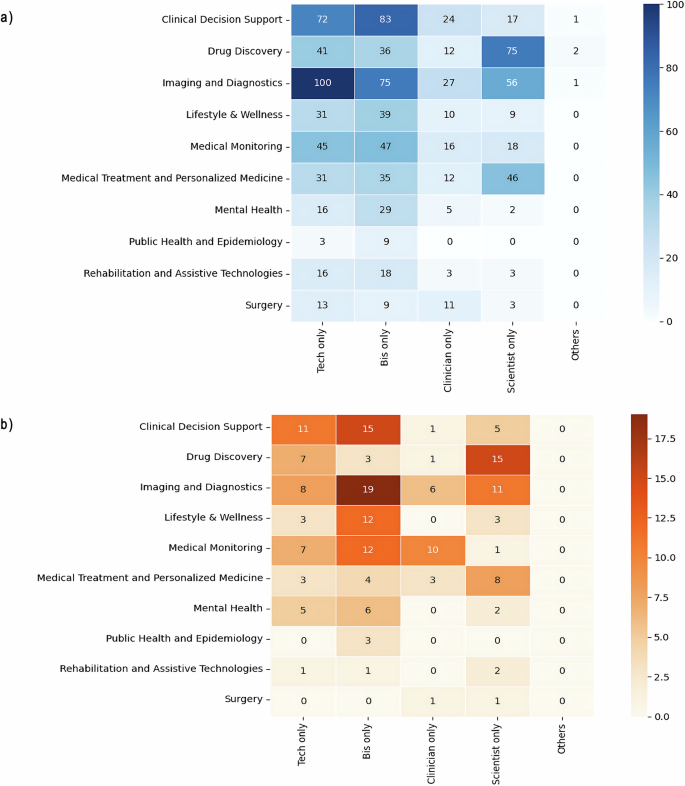

Figures 10a and 11a show that 190 startups are led by solo female founders, compared to 67 founded by female-only teams, highlighting a strong individual entrepreneurial presence among women. This solo dominance persists across medical domains. For instance, in Imaging and Diagnostics, 44 startups are led by solo female founders compared to 14 by all-female teams. Notably, no female-only teams were identified in Public Health and Epidemiology or Surgery (Fig. 11a), indicating limited representation of all-female teams in some specialties.

a Solo female founders (n = 190) predominantly have business backgrounds, particularly in Imaging and Diagnostics (19) and Clinical Decision Support (15). Scientist-only female founders concentrate in Drug Discovery (15). Clinician-only female founders remain sparse, with Medical Monitoring showing the highest representation (10). Female solo founders with clinical-only backgrounds are present in only six medical domains. b Solo male founders (n = 1101) show stronger technical representation, with technical-only founders most prominent in Imaging and Diagnostics (100) and Clinical Decision Support (72). Business-only male founders are also most represented in Clinical Decision Support (83) and Imaging and Diagnostics (75). Scientist-only male founders concentrate in Drug Discovery (75) and Imaging and Diagnostics (56). Male solo founders with clinical-only backgrounds are underrepresented across domains, except in Surgery. The comparison reveals gendered patterns in solo entrepreneurship: female solo founders are more likely to have business backgrounds, while male solo founders are more likely to have technical expertise.

a Female-only teams (n = 67) show limited formation across domains, with the highest representation in Clinical Decision Support (14) and Imaging and Diagnostics (14). Business-clinical combinations (dark green) are the most common in Lifestyle & Wellness (4) and Medical Monitoring (4), while Technical-business teams lead in Clinical Decision Support (5). Notably absent are female-only teams in Public Health, Epidemiology, and Surgery. b Male-only teams (n = 1626) demonstrate substantially higher numbers across all domains and team compositions. Technical-business combinations (dark purple) dominate in Clinical Decision Support (121), Imaging and Diagnostics (101), and Medical Monitoring (71). Technical-scientific/clinical teams are well represented in Imaging and Diagnostics (87), Clinical Decision Support (58), and Drug Discovery (51). The stark difference in team formation patterns—with female-only teams representing just 4% of all team-based startups—suggests significant challenges women likely experience in forming all-female founding teams in AI health entrepreneurship.

Among solo female founders, the most prevalent professional background is business, with 75 founders possessing business expertise, followed by 48 founders with a scientific background (Fig. 10a). Nineteen of the solo business founders are concentrated in Imaging and Diagnostics, while only one team startup has a business-only composition. In Drug Discovery, 15 of the 26 solo female founders have a scientific background, compared to just two female-only teams with similar expertise (Figs. 10a and 11a). These findings suggest that women with scientific or business expertise are more likely to launch ventures individually rather than as part of all-female teams. Taken together, the above findings align with prior studies indicating that female entrepreneurs in science-based and high-tech fields often face higher barriers to entrepreneurship due to constraints on forming complementary teams and accessing network resources62,63.

Founding structures—male startups (Figs. 10b and 11b)

Conversely, male-only founder startups exhibit greater balance between solo and team-based structures. In Imaging and Diagnostics, for example, 259 solo male-founded startups are matched by 425 team-based male-only ventures. Across medical fields, most male-only startups have teams with both technical and business expertise (475 teams), followed by technical and scientific/clinical (223), technical-only (206), and business and scientific/clinical expertise (196). Similar to female-only startups, male founders who are clinical or scientific-only are less likely to form startups alone or in teams. This supports prior findings that interdisciplinary team formation is especially critical in health technology startups55.

In summary, this comparative analysis underscores a notable difference in team dynamics: exclusively female-founded ventures are skewed toward individual entrepreneurship, whereas male-founded ventures exhibit greater balance between solo and team startup models. Among female-only teams that do form, the most common composition combines business and clinical/scientific expertise (16 teams). Although 22 solo female founders have clinical expertise, no female-only startups have been founded solely by clinicians. This pattern may reflect a structural preference, or necessity, for clinically trained women to pursue ventures individually or within mixed-gender teams, potentially due to limited access to like-minded co-founders or institutional support. The low presence of clinician-only teams may also result from the high demands and time constraints of clinical practice, which make team entrepreneurship more difficult unless complemented by partners with managerial or technical expertise. Together, these patterns point to persistent barriers in forming diverse, interdisciplinary founding teams, an important consideration for efforts to broaden participation and leadership in AI health innovation.

Source link