In 2026, artificial intelligence (AI) funding maintained strong momentum, with volumes surging and major technology firms acquiring AI capabilities at an early stage.

These findings come from the Q1 2026 State of AI report, released in April by CB Insights. The report looks at equity financing activity into private AI companies during the first quarter of the year, sharing funding, thematic, and exit trends.

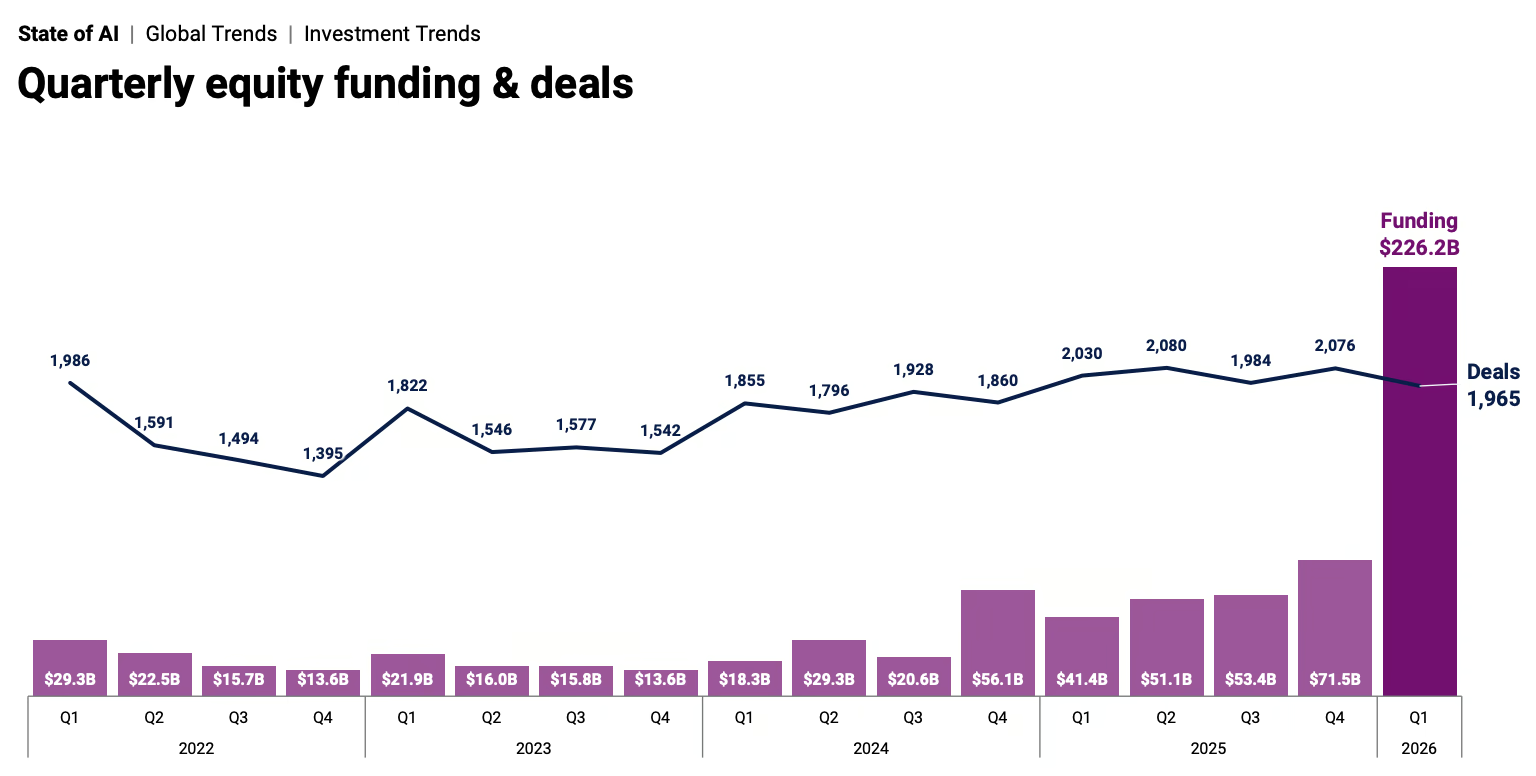

AI funding triples

According to the report, AI funding intensified in 2026. In the first quarter, global private AI funding surged by a staggering 216% quarter-over-quarter (QoQ), jumping from approximately US$72 billion in Q4 2025 to US$226 billion in Q1 2026. Notably, this single quarter already exceeds the entire year of 2025, which stood at US$217 billion.

Deal count remained stable in Q1 2026 at 1,965, compared to 2,076 in Q4 2025 and 2,030 Q1 2025. Mega-rounds of US$100 million and above dominated AI funding activity, with xAI, Anthropic, and OpenAI accounting for more than 70% of total AI funding in Q1 2026.

These transactions comprised:

- US$122 billion raised by ChatGPT parent firm OpenAI in March to build a “unified AI superapp”;

- A US$30 billion Series G raised by Anthropic in February to fuel the frontier research, product development, and infrastructure expansions; and

- A US$7.5 billion Series E secured in January by xAI to scale its compute infrastructure and buildout of the “largest GPU clusters in the world”.

These companies are racing to cover the compute, talent, and energy costs required to stay at the frontier of model development. The transactions reflect the enormous capital requirements of their advanced AI systems.

Physical AI leads

In Q1 2026, physical AI led all sectors with an 11% deal share and capital flowing into defense, industrial, and mobility. Industrial humanoid robot developers dominated with 17 deals as investment shifts from research and development (R&D) toward commercial deployment.

Pilot programs are already underway. Boston Dynamics’ new Atlas robot will be deployed at Hyundai facilities and Google DeepMind this year, European airplane manufacturer Airbus will use UBTech’s Walker S2 humanoid robots on its assembly line, and the BMW Group has launched a pilot project with humanoid robots at the Leipzig plant in Germany.

According to CB Insights, humanoid robot companies are on pace for a record US$10 billion in 2026 funding.

Autonomous driving was another significant investment theme in Q1 2026. Notably, Waymo, Wayve, and Waabi together raised US$18 billion and are already operating at commercial scale. Waymo now operates more than 3,000 robotaxis completing over 500,000 paid rides every week. Wayve, from London, plans to run its own robotaxi rides in London and Tokyo in 2026 in partnership with Uber and Nissan.

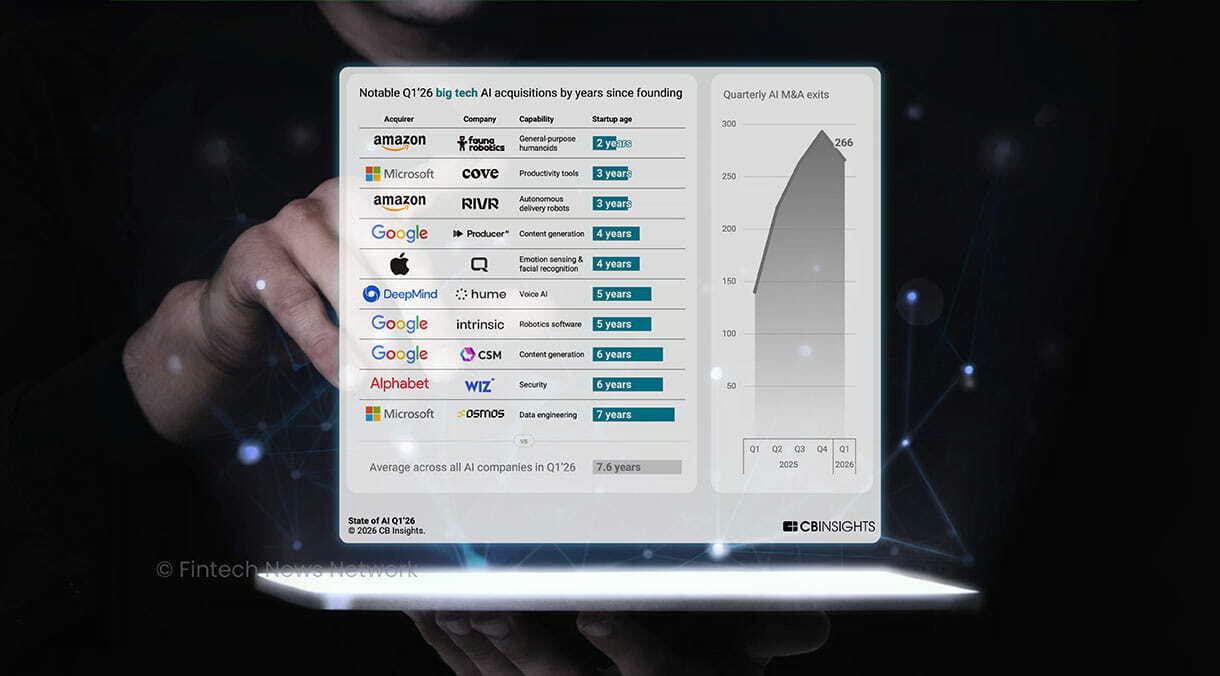

Bigtechs drive AI M&A activity

Mergers and acquisitions (M&A) activity in AI continued in Q1 2026, driven by bigtech firms. A total of 266 AI M&A transactions were recorded, representing a slight 9% QoQ decline, but a 90% year-over-year increase.

Bigtech firms focused primarily on young startups with an average time of exit of 4.5 years. Across all AI M&A transactions, the average time to exit stood at 7.6 years, reflecting how bigtech firms acquired AI capabilities before they scale. At the stage, many targets are still built around a single core capability, making them more affordable and easier for incumbents to integrate into existing product stakes.

Google was the most active dealmaker, with at least five acquisitions: Intrinsic, a software and AI robotics company; Common Sense Machines, which develops generative AI (genAI) models producing three-dimensional assets from two-dimensional images; Hume AI, an AI voice startup; ProducerAI, an AI music editor; and Wiz, a cloud and AI security platform.

Microsoft acquired at least two AI startups – Cove, an AI collaboration startup, and Osmos, an agentic AI data engineering platform -, while Amazon purchased Fauna Robotics and Rivr, two robotics startups.

Looking at regional distribution, CB Insights data show that the US continued to dominate AI funding, securing US$206 billion through 980 deals. The US accounted for 91% of the global AI funding volume, and 50% of the total deal count.

Europe followed with US$10.5 billion across 44 deals, while Asia secured US$8 billion and 438 deals. Africa trailed significantly with US$3 billion with just six deals.

Overall, AI led venture capital (VC) funding in Q1 2026, capturing 79% of all VC funding for the quarter, according to CB Insights data, reflecting how AI remains the primary focus for capital deployment.

Featured image: Edited by Fintech News Switzerland, based on image by rawpixel.com via Freepik