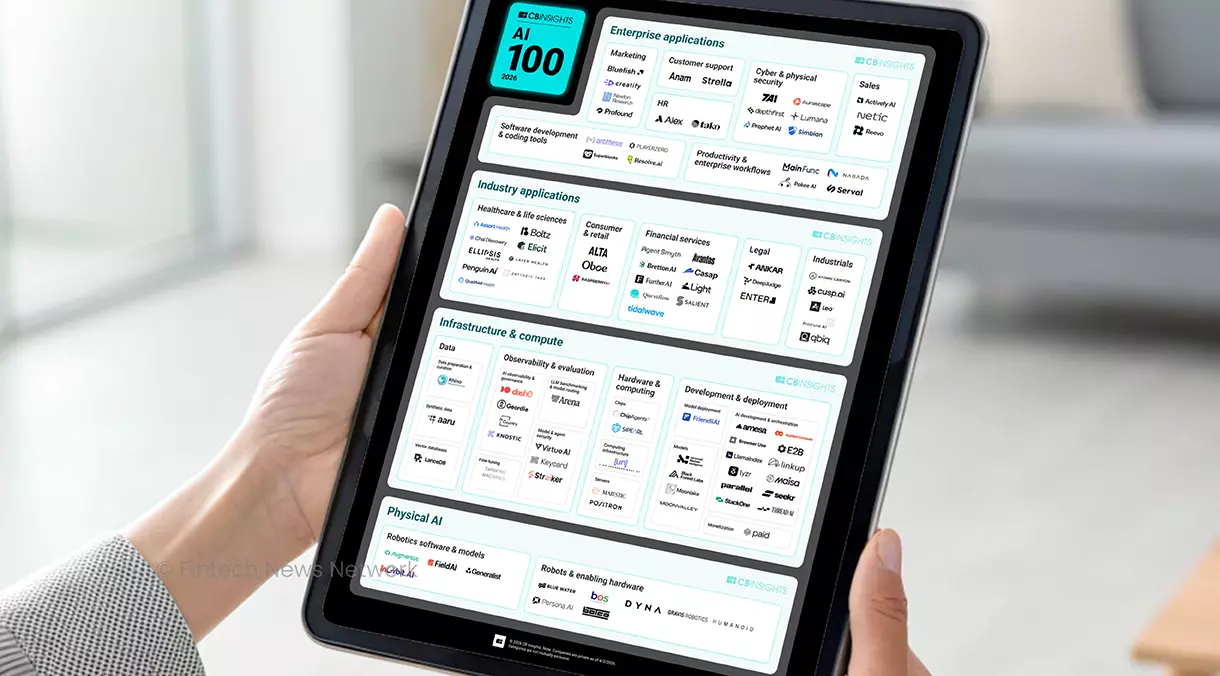

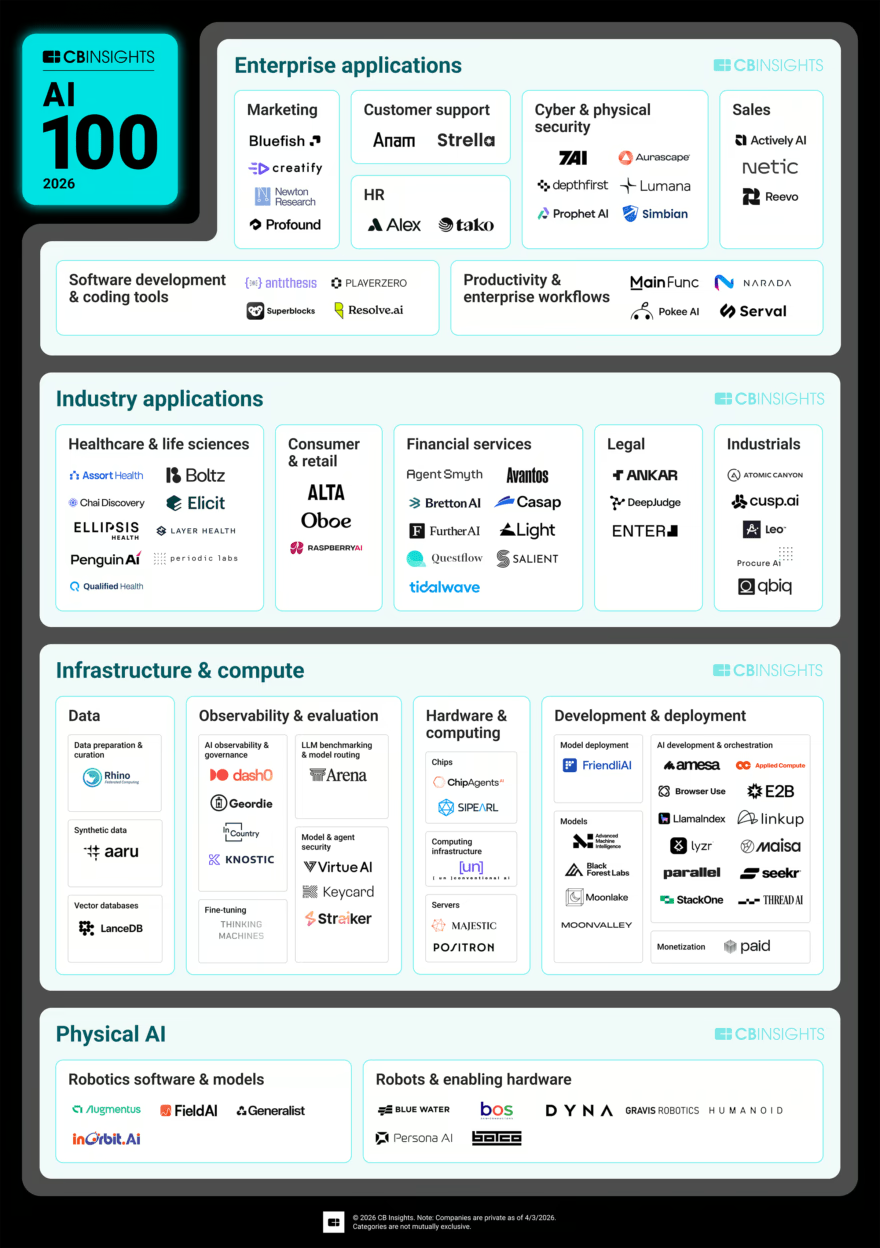

CB Insights has released its annual selection of the world’s most promising artificial intelligence (AI) startups, spotlighting the top emerging private AI companies based on market traction, investor quality, and talent.

This year’s 100 ventures emphasize the AI industry’s emphasis on early growth and market validation. An analysis of the landscape reveals that Series A ventures are the most prominent group on the list, totaling 60 companies.

These companies have moved beyond the prototype phase, and have proven that their products solve real problems. They are now focused on scaling customer acquisition, turning early traction into repeatable business models, and building sales and marketing teams.

These companies include 7AI, DeepJudge, and StackOne. 7AI is a US-based company that deploys autonomous AI agent swarms, automating security alert processing, incident management, and threat hunting.

Founded by former Cybereason CEO Lior Div and backed by Greylock Partners and Index Ventures, 7AI secured a US$130 million Series A in December 2025 just ten months after the company launched from stealth. It plans to use the proceeds to expand its AI security engineering and go-to-market teams. In 2025, its platform reportedly processed more than 2.5 million alerts and 650,000 investigations, cutting investigation times from hours to minutes and eliminating up to 95–99% of false positives in production.

DeepJudge, from Switzerland, provides AI-powered knowledge search and document retrieval platforms connecting law firms’ document management systems to retrieval-augmented AI agents. Founded by former Google researchers with PhDs in AI from ETH Zurich, the company serves elite firms including Freshfields and Holland & Knight, achieving 80-90% active usage rates.

DeepJudge secured a US$41.2 million Series A in November 2025 to deepen product innovation, expand its partner ecosystem, and scale internationally.

StackOne, based in the UK, builds unified APIs and tool-calling interfaces connecting AI agents and software-as-a-service (SaaS) applications to more than 200 enterprise systems across HR, CRM, and collaboration tools.

Founded by ex-Google and Oracle executives, StackOne raised a US$20 million Series A in May 2025 to continue building its state-of-the-art tool-calling large language model (LLM), invest in research and development (R&A), and further expand the number of integrations and depth of actions available in the StackOne platform.

Early-stage innovators and scaling leaders

After the Series A-stage leaders, 21 seed-stage ventures are featured. These young companies are still refining their initial products and searching for product market-fit.

They include Boltz, an American startup developing AI models for molecular structure design and optimization, and Paid, a UK-based billing infrastructure provider for AI agents.

This year, Boltz secured a multi-year collaboration with Pfizer and backing from Andreessen Horowitz, alongside Zetta Venture Partners and Amplify Partners. Paid, which is backed by Lightspeed Venture Partners and Sequoia Capital, has secured prominent enterprise customers including IFS and Artisan, and has grown its headcount 140% year-over-year (YoY), according to CB Insights.

At the other end of the spectrum, 16 companies are in the Series B or later stages. These organizations have established business models and are seeing strong revenue growth. They are now expanding internationally, scaling their teams, and acquiring customers aggressively.

They include Serval, which provides an AI-powered IT service management platform to automate help desk requests; Actively AI, which deploys persistent agents to automate sales accounts; and Positron, which develops purpose-built AI inference hardware optimized for transformer models.

Serval serves clients like Perplexity, allowing them to achieve over 50% ticket automation. Backed by Sequoia and Redpoint Ventures, the company has grown headcount 347% YoY, according to CB Insights.

Actively AI, founded by Stanford AI researchers, is driving measurable ROI, allowing clients like Samsara achieve 2x conversion rates. Actively AI has grown its headcount 107% YoY with top-4% hiring momentum.

Finally, Positron, which manufactures chips in Arizona, claims 3.5x better performance-per-dollar than Nvidia’s H100 with 93% memory bandwidth utilization versus 10-30% in GPU systems. The company has grown headcount 120% YoY.

Nine startups focused on financial services make the list

This year’s CB Insights’ AI 100 list spans three broad categories:

- Enterprise application providers, which deliver AI products that deploy agents and workflows to automate or augment business functions across an organization;

- Industry application providers, which offer verticalized AI products built for the specific data, compliance, requirements, and workflows of an industry; and

- Infrastructure and compute, which provide the foundational layer of models, tooling, and hardware, and observability upon which AI applications are built on.

Within the industry application category, financial services emerges as the largest subsector, featuring nine companies. This count makes it neck-and-neck with healthcare.

The nine financial services-focused AI companies are:

- Agent Smyth, a New York-based autonomous agent platform for trading and investment;

- Avantos, an AI native operating system for client management, empowering financial institutions to onboard, service, and grow client relationships;

- Bretton AI, an AI agent platform for financial crime compliance;

- Casap, an award-winning dispute automation platform that streamlines compliance, reduces operational costs, and enhances consumer satisfaction for banks, credit unions, and fintech startups;

- FurtherAI, a domain-specific AI for the insurance industry, automating workflows like submission intake, policy comparisons, and underwriting processes;

- Light, a AI native finance platform automating payments, expense management, bookkeeping, and financial reporting across jurisdictions;

- Questflow, a collaborative AI automation tool for teams to create, orchestrate and automate tasks across platforms;

- Salient, an AI workflow automation tool for lenders, automating collections, customer service, disputes, chargebacks, and total-loss mitigation with compliance-first AI; and

- Tidalwave, an agentic AI company that aims to eliminate bottlenecks in the mortgage process.

Physical AI becomes a standalone category

A defining trend in this year’s AI 100 list is the debut of physical AI as a standalone category. Physical AI refers to AI systems that perceive, decide, and act in the physical world through autonomous machines and robotics. The sector has witnessed significant momentum over the past years, with companies in the space raising a record US$78 billion 2025.

11 companies comprise this new category, spanning robotics software, autonomous hardware, and enabling chips. These companies’ inclusion reflects a critical inflection point for physical AI, as the entire stack required to deploy autonomous systems in the real world is maturing simultaneously.

Beyond these capabilities, the sector is also seeing a surge in solutions that coordinate multiple autonomous units toward shared objectives. Key players exemplifying this shift include:

- InOrbit, which builds AI-powered software to monitor, coordinate, and optimize fleets of autonomous robots in warehouses, factories, and other industrial environments;

- FieldAI, which develops AI systems that let different kinds of robots operate autonomously in complex real-world environments like construction, energy, and logistics sites; and

- Gravis Robotics, which retrofits excavators and other heavy construction equipment with AI and autonomy technology to improve productivity, safety, and precision on job sites.

InOrbit grew its customer base 200% in the past year, according to CB Insights; FieldAI raised a US$314 million Series A at a US$2 billion valuation in August 2025; and Gravis Robotics, founded in 2022, is already deployed across seven countries, early signals that the market is forming fast.

Observability and evaluation tools emerge amid rising agentic AI

Another defining trend this year is the evolution of AI agents into a distinct class of actors. As these agents move from experimental prototypes to active participants in enterprise workflows, they require their own layers of identity, credentialing, and accountability.

The observability and evaluation category in this year’s AI 100 list is addressing this. The nine companies in this category are building the necessary infrastructure to govern these non-human actors, establishing the operational rulebook for letting autonomous systems participate in enterprise workflows. These companies include:

- Keycard, which builds identity and access-management infrastructure that lets companies securely authenticate, authorize, and manage AI agents;

- Geordie AI, which provides governance and security monitoring for enterprise AI agents, giving teams visibility into how agents behave and what risks they pose;

- Virtue AI, which develops AI security software that red-teams, monitors, and applies guardrails to AI models and autonomous agents; and

- Straiker, which secures AI agents at runtime by detecting vulnerabilities, testing agents against attacks, and preventing malicious AI behavior in enterprise systems.

Collectively, the nine companies in the observability and evaluation category have raised US$278 million in the last three years. This capital influx underscores the nascent stage of the category and highlights the growing recognition that robust governance and oversight are critical for autonomous systems to safely integrate into enterprise workflows.

Featured image: Edited by Fintech News Switzerland, based on image by arslantanoli via Magnific