Investment activity across the Middle East and North Africa (MENA) cooled in June 2026, with 41 startups collectively raising $148.2 million, marking a 76% decline from the previous month. However, funding was still 190% higher than in June 2025.

The month-on-month decline looks significant at first glance. However, excluding debt financing from both months narrows the gap to just 15%, suggesting that the ecosystem is gradually recovering from the regional turmoil that weighed on investment activity throughout the first half of the year. Notably, deal activity actually increased, with 41 transactions recorded in June compared to 33 in May.

June also brought notable shifts in how capital was distributed across the region, both geographically and sectorally, reshuffling the rankings of the ecosystem’s usual leaders.

Egypt returns to the top tier

The United Arab Emirates remained the region’s top-funded market, with 12 startups raising a combined $93.8 million.

Meanwhile, signs of economic stabilisation have begun to emerge in Egypt, following a pause in regional hostilities. The Egyptian pound has remained relatively stable against the US dollar, while tourism revenues have reached their highest level in years.

Against this backdrop, Egypt climbed to second place among MENA’s most-funded startup ecosystems, with eight startups raising $41.4 million. Saudi Arabia, typically one of the region’s top two markets, ranked a distant third after five startups secured a combined $5.7 million.

Morocco, which did not record any funding in May, returned to the rankings in fourth place after proptech startup Agenz raised a $5 million round.

Oman also recorded an active month, with 10 startups raising a combined $1.3 million. While the funding value remained modest, the high deal volume reflects the growing role of the country’s accelerator programmes in stimulating startup activity.

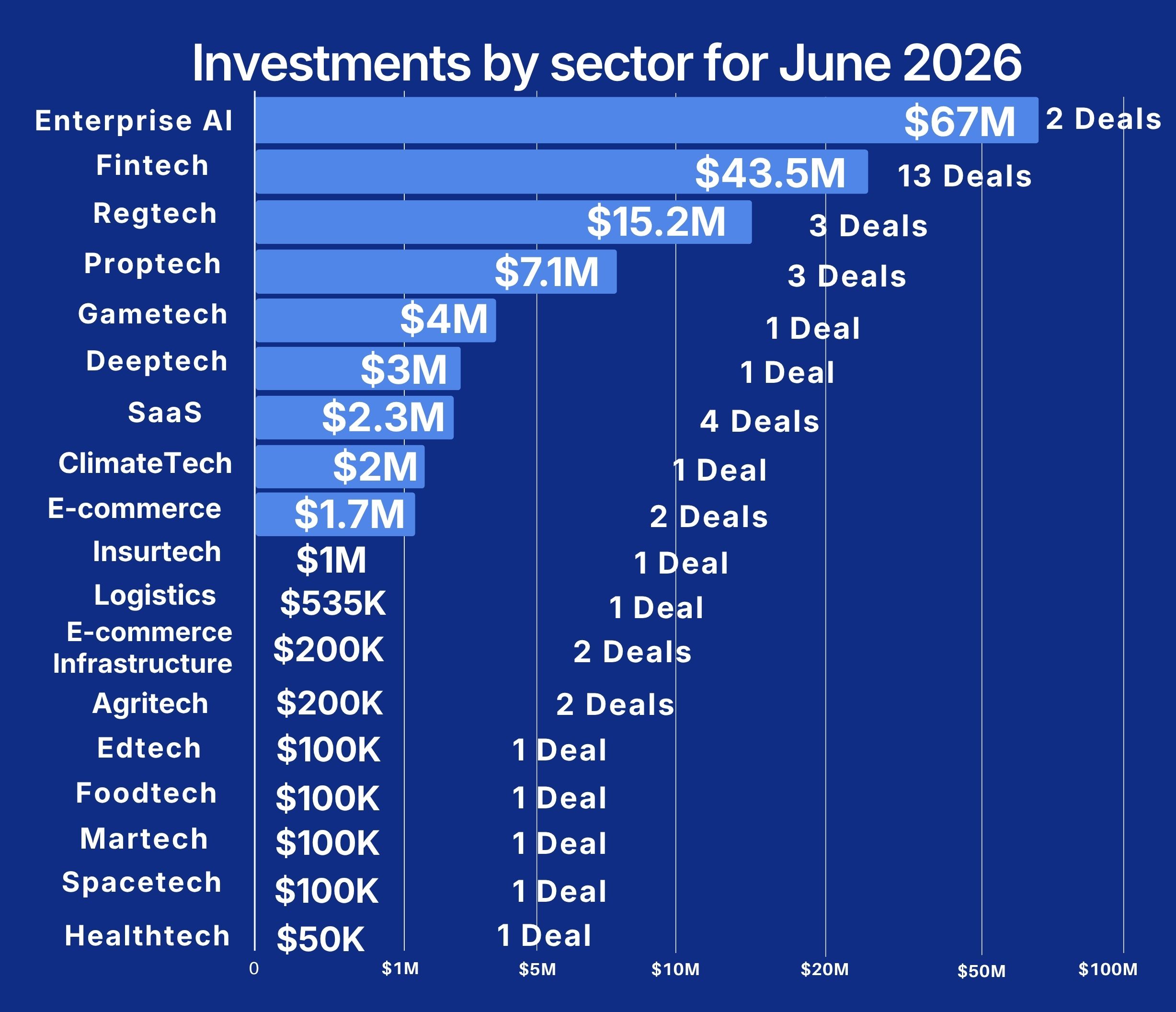

Enterprise AI takes the lead

The sectoral landscape also shifted in June. Enterprise AI emerged as the largest recipient of capital, with just two startups raising a combined $76 million. Fintech remained the second most-funded sector for the second consecutive month, while retaining the highest deal count, as 13 startups secured $43.5 million. Regtech followed with $15.2 million raised across three rounds, while proptech startups attracted $7 million through three deals.

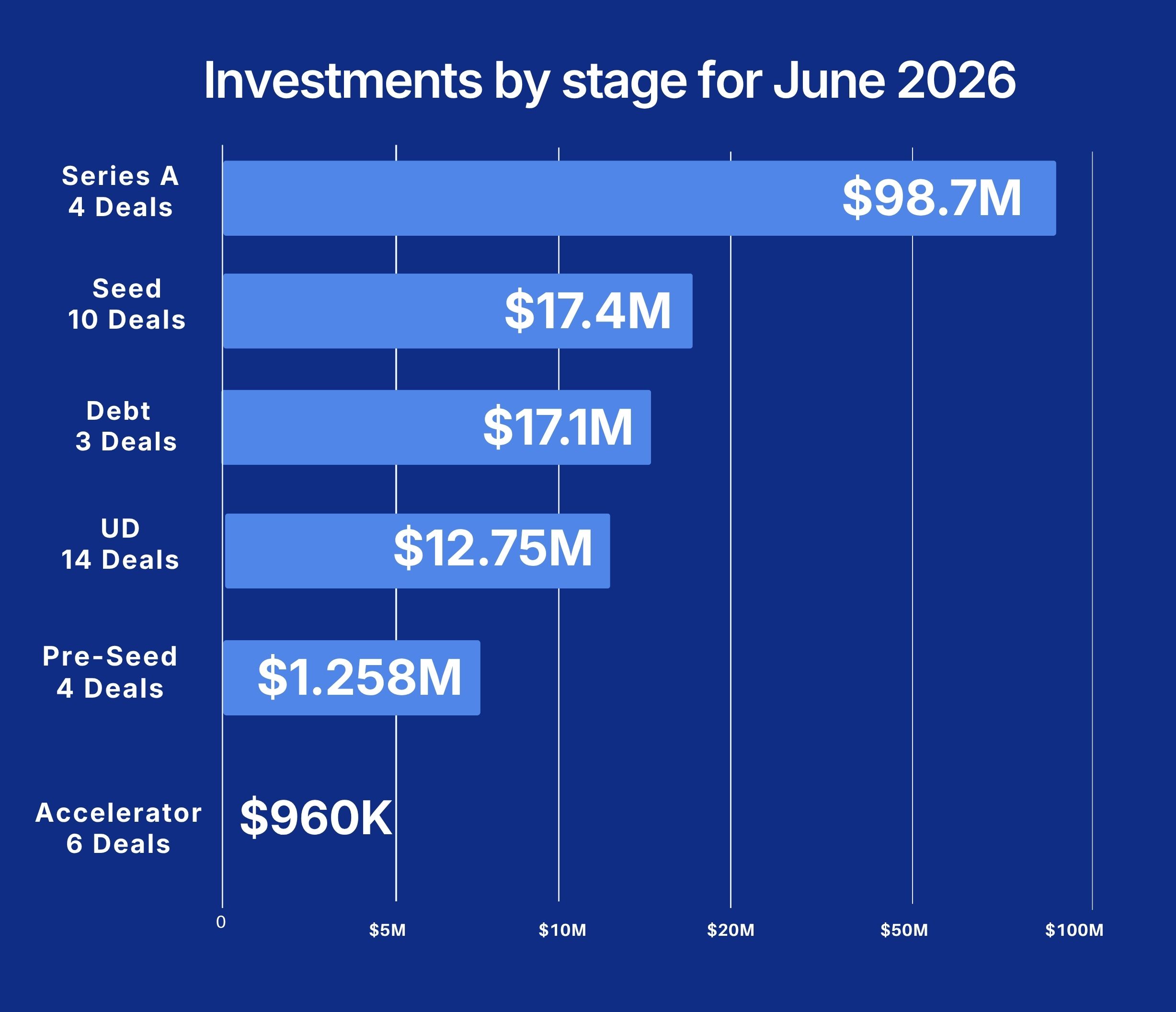

Early-stage founders dominate investor appetite

June recorded no later-stage equity rounds, with capital flowing almost exclusively to early-stage startups and debt financing. Meanwhile, 14 startups did not disclose the stage at which they raised funding.

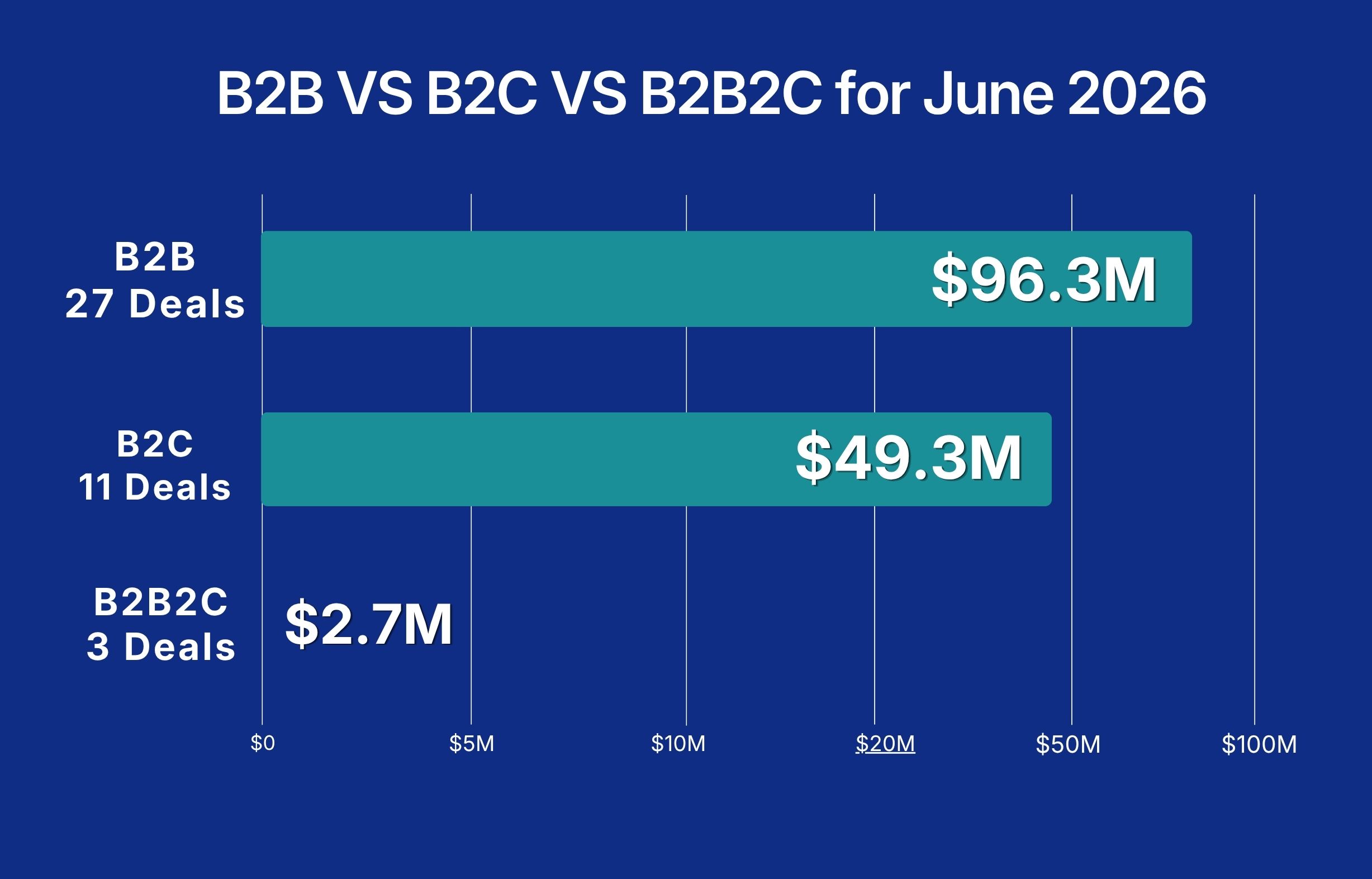

Business-to-business startups continued to dominate investor interest, attracting $96.3 million across 27 deals. Consumer-focused startups raised less than $50 million through 11 transactions, while the remaining capital was invested in hybrid business models.

The funding gap persists

The funding gap between male and female founders continued to widen. Female-led startups secured just $260,000 across two deals, while mixed-gender founding teams raised $5.6 million. Male-founded startups accounted for the overwhelming majority of capital, raising $142.3 million across 37 transactions.

Looking ahead

While the first half of 2026 was marked by geopolitical uncertainty and heightened investor caution, the latest funding trends offer encouraging signs that the MENA startup ecosystem is regaining its footing. The resilience shown over recent months reflects growing confidence among both regional and international investors in the region’s ability to absorb the economic fallout of the conflict that erupted in February. Although a final agreement between the United States and Iran has yet to be reached, the ecosystem continues to adjust, positioning itself for what could be a considerably stronger second half of the year, should macroeconomic and geopolitical conditions continue to stabilise.

For a deeper analysis of investment activity across the first half of 2026, stay tuned for Wamda’s H1 investment report, to be published on 13 July 2026.

Source link