- Magenta is pivoting from running EV fleets to leasing vehicles to drivers, after discovering that competing with owner-operators is structurally unviable.

- The company’s earlier model failed because it was competing with a deeply unorganised market where individual drivers operate at far lower cost structures.

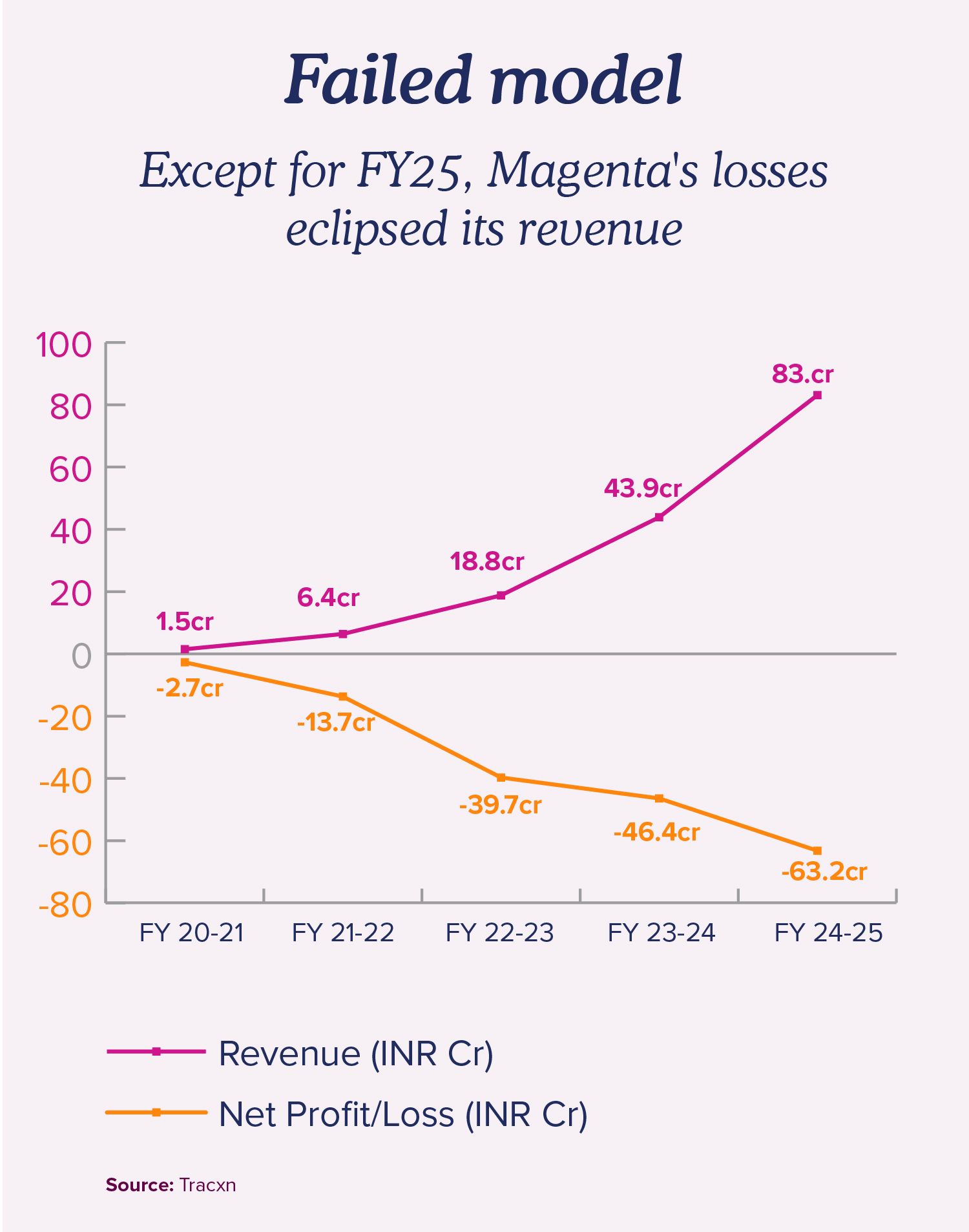

- Despite the pivot, Magenta continues to make losses and remains dependent on fresh capital to survive.

- Investor appetite for EV fleet models has weakened sharply after BluSmart’s collapse and setbacks at companies like Altigreen.

In January 2020, Jeff Bezos climbed aboard an electric cargo three-wheeler in India. The world’s richest man, perched on a squat three-wheeler built for hauling boxes through narrow lanes, looked faintly absurd. But the signal was serious. Amazon pledged to put 10,000 electric vehicles on Indian roads by 2025, and an entire industry leaned forward.

Among those watching closely were Maxson Lewis and Darryl Dias, cofounders of a small startup called Magenta Mobility. At the time, Magenta was in the charging business, a lonely trade in a country with barely any EVs on its roads. The company had even partnered with Tesla during the carmaker’s early attempts to enter India, piloting a supercharger in Pune, according to people aware of the matter. But charging stations without cars to charge made for a grim spreadsheet.

Bezos handed them a reason to pivot. If Amazon and its rivals were going to electrify their supply chains, someone would need to run the fleets. Lewis and Dias pivoted, building an all-electric cargo logistics operation aimed squarely at ecommerce fulfilment.

For a while, it worked well. The pandemic sent ecommerce volumes soaring. Magenta scaled to around 2,600 electric three-wheelers across 21 cities and grew to over 400 corporate employees. In 2021, it raised $17 million from investors including LetsVenture and Shell. Its early backers include oil company HPCL. By 2023, it had sold its charging business to Jio-BP, as first reported by The CapTable, and raised another $22 million, bringing in BP Ventures and Morgan Stanley. The sale of the charging arm was also part of the agreement for BP Ventures’ entry, given potential conflicts of interest.

Then the music stopped.

Cut to 2026, and much of that early promise has curdled. In FY25, Magenta reported Rs 83 crore in revenue and Rs 63 crore in losses. In previous years, its losses had consistently exceeded its revenue. Fresh capital has been scarce since 2023, with both Morgan Stanley and BP Ventures putting in $5 million in March 2025, according to Tracxn, along with another $5 million in debt from SIDBI.

According to three people aware of the matter, the company has laid off over 100 employees since August 2025, with one estimating the number closer to 200, or about half the workforce. Though headquartered in Mumbai, the company gave up its Bengaluru office—its largest—which also housed most of its CXOs. Lewis has moved into the role of chairman. The other cofounder, Dias, exited the company in November 2025. And a new CEO, Sujit Cherian, a former Leap India executive, has taken the wheel, in a move that multiple industry executives see as driven by lead investor Morgan Stanley, which also backed Leap India.

The parallels with BluSmart, the electric cab company whose spectacular collapse scorched investors and chilled the entire EV sector, are hard to ignore. Overlapping backers. Asset-heavy fleet models. Early-generation vehicles that could not hold up. And a market that moved on faster than either company could adapt.

Cherian is aware of the comparison. He is also determined to outrun it.

Cherian is a chartered accountant who has spent two decades moving between consulting, aviation and private equity. He worked at PricewaterhouseCoopers and Andersen, spent five years at Jet Airways in leadership roles, served as CFO of GoAir, and later joined a Hong Kong-based fund called Bravia Capital. At Leap India, a returnable packaging company, he helped lift the valuation from Rs 100 crore to nearly Rs 9,000 crore over nine years, a run that caught Morgan Stanley’s attention.

“I always say I gave an exit to Morgan Stanley in 2023 and they gave me an entry into Magenta in 2025,” he said. “One good exit always begets a good entry.”

In a conversation with The CapTable, Cherian pushed back firmly on the narrative of decline. He disputed claims of halving the workforce, saying headcount has come down by 20 to 25 per cent, from around 400 to about 300, which he called a reorganisation rather than a downsizing. New hires, he said, are coming in at the top: a new chief technology officer, a new head of finance, a new asset head, and so on.

“I would not characterise it as a downscaling of business. It is more a reorganisation and reskilling of the workforce,” he said.

He also laid out a new strategy, one that amounts to a wholesale reinvention of Magenta’s reason for being.

Magenta’s core problem was simple. The company, a venture-backed corporate with offices, managers and employee benefits, was competing for logistics contracts against individual drivers who owned their own vehicles and had virtually no overheads.

Cherian put it plainly. “The Amazon delivery that comes to our house does not come in an Amazon-branded fancy vehicle. Very often it comes in a public goods carrier. The guy driving it is very often the owner of the vehicle as well.”

A driver with a single truck, willing to work for Rs 500 on a slow day, will always undercut a company that must cover EMIs, fuel, insurance and a sales team. “If you compete with transporters and drivers as a corporate, you will always fail,” Cherian said.

This is why small-format trucking in India has remained stubbornly unorganised for decades, and why building a venture-scale business on top of it proved so punishing.

The economics of EVs made it worse, not better. A 1.7-ton Bolero pickup costs about Rs 11 lakh. An equivalent electric vehicle runs to Rs 15.5 lakh or more. Yes, running costs are lower over time. But the upfront premium is brutal, and at a small scale, the savings may never catch up.

“When you combine total cost of ownership, given the premiums being charged, it just does not work,” Cherian said. “What we realised is that if you do this business at scale, the upfront premium can be managed better and the operating costs can reduce further.”

On top of this, the market itself was shifting beneath Magenta’s feet. The company had built its fleet around three-wheeler cargo vehicles, the natural workhorses of last-mile ecommerce. But the rise of quick commerce, where speed matters more than payload, rewrote the rules. Two-wheeler EVs became the preferred mode for high-frequency, time-sensitive deliveries, pushing three-wheelers into more fragmented and price-sensitive corners of the market.

“Magenta has a lot of three-wheeler cargo vehicles, and those were built for the ecommerce era, not the quick commerce era,” said an investor in the EV space. “Flipkart, Zomato—these platforms have taken control of their own supply chains. The question became: why go through Magenta? Drivers can sign up directly with whoever gives them a vehicle.”

Cherian did not deny the shift but argued its limits. “Yes, two-wheelers are the toast of the town today—they serve a purpose. Food comes on two-wheelers. Urgent requirements come on two-wheelers. But everything cannot come on two-wheelers,” he said. “When a household buys groceries for a month, that may be 15 kilos. Fifteen kilos cannot move on a two-wheeler.”

If competition was one half of the problem, the vehicles themselves were the other.

The CapTable had reported last year how early versions of Tata Motors’ Tigor EV made it nearly impossible for fleet operators to break even. Faster battery degradation, longer charging downtime and the sheer inability of first-generation models to withstand the rigours of commercial use in India meant that the core asset of any fleet business was also its weakest link.

“These early fleet companies—their core asset is vehicles, which is a traditional, depreciating asset,” said the investor quoted earlier. “It was never an individual driver business. You need debt to operate, and that’s how the model works. The problem is when you try to be a fleet company without going deep on either hardware or logistics, you end up in no man’s land. There are better vehicles and assets emerging every year.”

Another executive in the EV fleet space, who has dealt with the same vehicles first-hand, was less forgiving. “It all boils down to the asset itself—the vehicles are just not the right kind of asset,” he said. “My first experience in this space was with Tata vehicles, and it was a mess from the start.”

Magenta was not immune. The company deployed vehicles from Tata Motors, Switch Mobility, Euler Motors and, disastrously, Altigreen, a three-wheeler maker that became what Cherian called “a big liability”.

“We also bought certain vehicles initially where either the company shut down or the quality of the vehicle was not adequate to be economically viable,” Cherian said, adding that these form a relatively small part of Magenta’s fleet.

He conceded the broader point without hesitation. “I am telling you categorically: your concern is valid. The success of the fleet model and electrification in India is going to depend substantially on the quality of assets that are going to come out.”

But he argued that the tide has turned. Over the past two to three years, he said, both three-wheelers and four-wheelers have improved sharply in performance, battery quality and overall cost of ownership. Magenta currently operates over 400 four-wheelers, largely from Tata Motors, Switch Mobility and Volvo-Eicher, and more than 2,000 three-wheelers, primarily from Bajaj, Omega Seiki and Mahindra.

“Bajaj and some others are good vehicles. We have been operating these for over two years and we are happy,” he said.

Magenta’s answer to all of this is a model it calls B2D, or business-to-driver. Instead of managing fleets, hiring drivers and chasing enterprise contracts, the company now wants to lease electric vehicles to individual drivers on short-term rentals. The drivers find their own work, plugging into platforms like Porter and Borzo. Magenta handles the vehicle, the EMI, the charging, the insurance, the battery monitoring and the repairs.

“We are saying: forget EMI, forget charging, forget repair, forget battery monitoring. All this we will take care of. Drivers just drive,” Cherian said.

The logic is seductive. Strip away the corporate overheads of running a logistics operation. Stop competing with drivers. Instead, become their vehicle provider. Make money on the asset, not the freight.

The company explored other options, including a pivot into passenger EVs for employee transportation. But that path was blocked. BP Ventures, a key investor in Magenta, is also invested in BluSmart, and the potential conflict of interest ruled out any foray into overlapping territory.

Cherian said the B2D model has been in testing for over a year and that its unit economics are “significantly” better than the old approach. He expects Magenta to turn EBITDA positive in the coming year and PAT positive the year after. “It will also come on the back of additional investments, and we are confident those investments will come through,” he said.

Confidence, however, does not pay bills. Magenta publicly stated plans in November to raise $50 million. It is yet to secure a term sheet. And The CapTable has learnt that the company could run out of cash within a year.

Cherian said the company is in “advanced talks”, with initial diligence completed and early investment committee approvals in place. He did not confirm a signed term sheet but said the company has raised a recent bridge round from existing investors and has “adequate liquidity” to operate until the planned Series B raise. He declined to share the size of the bridge round or the exact cash runway.

“At the end of the day, people will fund businesses where they see a clear path to profitability,” he said. “It is not because of my drop-dead gorgeous looks that they are funding. They are funding because they see a robust business plan and unit economics that work.”

But investor mood around EV fleets has soured badly. “The appetite for EV fleet businesses has come down considerably among investors, even among the greenwash investors,” said the investor in the space, pointing to a retreat by backers such as Shell, BP Ventures and HPCL following the BluSmart and Altigreen fallouts.

“Altigreen has been a big liability. BluSmart has been a fiasco for the industry,” Cherian said. “You can quote me on that.”

Every year, close to five lakh light commercial vehicles are sold in India. Last year, barely 10,000 were electric, and of those, only 1,000 to 2,000 went into public goods carriage. The market Magenta is betting on is real, but it remains stubbornly small.

If the $50 million does not come through, the burden falls back on existing investors, and the most powerful among them is Morgan Stanley India Infrastructure, which operates more like a private equity firm than a traditional venture investor, favouring infrastructure assets and control-oriented bets.

According to a person aware of the matter, Morgan Stanley has been open to acquiring a larger stake in Magenta, potentially even a buyout, at a significantly lower valuation, a proposal that existing investors have resisted.

Such moves are not new to the EV sector. Eversource Capital took control of EV cab company Lithium Urban after a tussle with its founders and also operates Greencell Mobility, an intercity bus service. These firms deploy large pools of capital, seize control, cut costs and wait for the market to catch up.

“For fleet companies like this, the only outcomes are: you shut shop, or you get someone like an Eversource to play the waiting game,” said the EV fleet executive.

Cherian denied any such discussions are underway. “No. It is not something that has ever been discussed so far,” he said. “While it cannot be ruled out, it is not something that we are discussing at present.”

Magenta’s fate matters well beyond its own balance sheet. If the company falters, it marks yet another blow for investors like BP Ventures, Lets Venture and JITO Angel Network, many of whom are already nursing losses from BluSmart. It would further freeze lending appetite for EV fleets, an ecosystem already gasping for capital.

With an investor-appointed CEO now steering the ship, the outcome may yet differ from BluSmart’s. Cherian has a track record of building value over long cycles. The B2D model, if it works, could offer a cleaner path than the old freight-hauling approach. And newer vehicles are, by most accounts, genuinely better.

But the runway is short, the capital markets are cold, and the ghosts of BluSmart linger over every pitch deck in the sector.

“Money does not come, businesses shut down. There are no two ways about it,” Cherian said.

He paused, then added something that sounded less like corporate messaging and more like conviction. “Electrification is even more important today than it has ever been for India. If we do not electrify, we are playing ourselves into the hands of geopolitical risk. We are playing ourselves into balance of payment issues.”

Whether that belief, and the business built around it, can survive long enough to prove itself is the question that now hangs over Magenta Mobility.