When Brass launched in 2020, its pitch was modest: let Nigerian businesses open a bank account in minutes, move money without friction, pay their teams, and actually understand their finances.

No queues. No bureaucracy. No systems were designed for a banking era that had already passed.

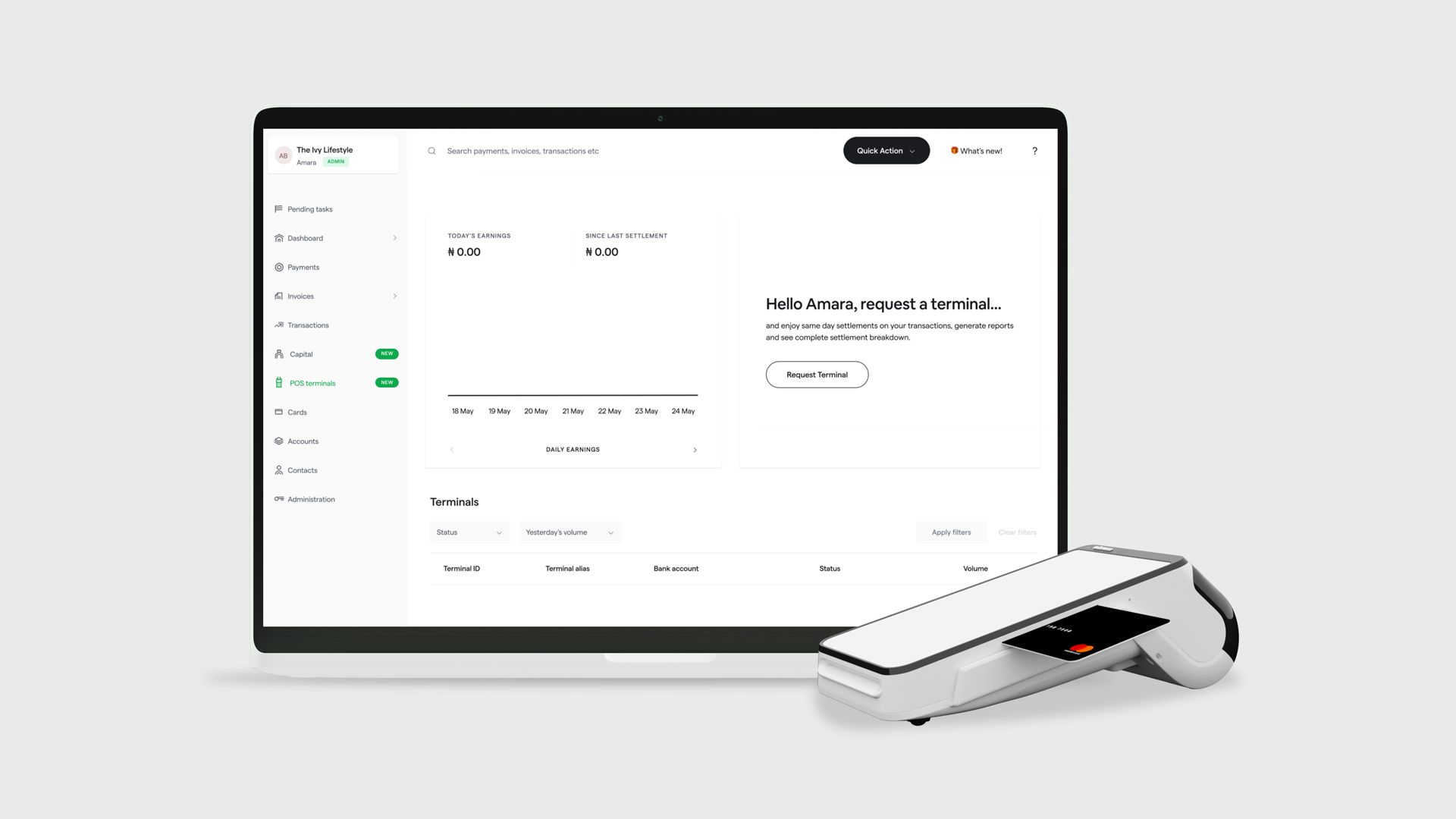

For thousands of Nigerian SMEs, that pitch landed. Brass became one of the country’s most talked-about business banking startups, raising over $2 million and building a product stack that included payments, payroll, expense management, and cash flow tools — all wrapped in a clean interface built for founders who didn’t have time for legacy banking.

For a while, it worked. Then it didn’t.

When the Wheels Came Off

Beginning in October 2023, Brass ran into serious trouble: delays in processing customer withdrawals triggered a liquidity crisis, sparking widespread concern and fuelling rumours of a potential shutdown. The problem threatened to erode trust in Nigeria’s broader fintech ecosystem at a moment when that trust was already fragile.

Several ecosystem heavyweights rallied around the company, worried that the collapse of a deposit-taking fintech could cause a bank run on other fintechs. A new capital injection in March 2024 enabled Brass to resume withdrawals for affected businesses, stabilising operations ahead of what came next.

What came next was an acquisition.

In May 2024, a Paystack-led consortium acquired Brass for an undisclosed amount, in a deal aimed at stabilising operations and preventing a wider confidence crisis in Nigeria’s fintech sector. Joining Paystack in the consortium were PiggyVest, Ventures Platform, and P1 Ventures.

Brass co-founders Sola Akindolu and Emmanuel Okeke exited the business as part of the deal.

The acquisition was framed, publicly at least, as a rescue with ambition — not a wind-down, but a relaunch under stronger stewardship.

Two Years of Rebuilding

In the months following the acquisition, a new leadership team led by Philip Obosi and Yvonne Obike undertook a focused rebuild of Brass’s internal systems and operational processes. The platform was overhauled.

Recurring payments, team spending tools, and financial tracking were re-engineered for reliability. The product matured.

But maturity revealed a ceiling.

As Brass rebuilt, it became clear that the next phase of growth couldn’t be achieved independently. It needed deeper infrastructure, broader regulatory standing, and a larger platform. That platform, the company now says, already existed inside its own ecosystem.

The Final Merge

Brass has announced it will cease to operate as an independent entity. Its business banking operations will migrate into Paystack Microfinance Bank (Paystack MFB), a licensed microfinance bank with the regulatory infrastructure and product depth that Brass, as a standalone startup, could never fully replicate.

Existing customers will be transitioned to Paystack MFB before July 31, 2026, with the company promising direct communication and minimal disruption for each merchant.

The move is less a pivot than a logical endpoint. Paystack MFB offers the core of what Brass customers relied on — account management, payouts, expense organisation, money movement, financial reporting — inside a more powerful, regulated wrapper.

For Paystack, the deal completes a quiet but significant expansion of its financial services footprint. The payments giant has long positioned itself as infrastructure for African business, and absorbing Brass’s SME banking customer base extends that position further up the financial stack.