Hey all, Jason here.

I did not stay awake late enough to watch England beat Norway in yesterday’s World Cup match. I may need to make a stronger effort to actually watch the France v. Spain semifinal game this Tuesday (on Bastille Day no less!) At this point, all the teams I was nominally rooting for (Mexico, Netherlands, USA, in that order) have been eliminated, so I can’t say I have a strong affinity for any of the teams that remain…

Fintech Business Weekly and Alumni Ventures are teaming up this week only to give readers early access to high-growth startup opportunities, including some of today’s most exciting Blockchain & Fintech startups co-invested alongside top VC firms like Paradigm & Pantera Capital.

You get:

• Curated deal flow of high-potential Blockchain & Fintech startups

• No cost, no commitment to join

• Invest only if a company excites you

Don’t miss your chance before access closes.

Key takeaways:

ALT5 Sigma, which World Liberty Financial led a $1.5 billion investment into, has a banking-as-a-service type subsidiary, MSwipe, which also does business under the name Stradacarte

MSwipe works with 14 bank and program manager partners, its staff told me; partners have included Sutton Bank and Marqeta, and appear to also have included Wex Bank, ConnexPay, and Corpay

MSwipe offers “no KYC” card issuing, and, sources told Fintech Business Weekly, it has been linked to “no KYC” crypto card programs that include Bitsika, which marketed its service for use in evading sanctions on Iran

Industry sources describe Sutton Bank as a “paranoid and chaotic organization,” “incompetent,” and warn the bank could be “Evolve 2.0”

You’ve probably heard of World Liberty Financial, the crypto platform launched by then-candidate Trump shortly before the 2024 election.

The company has been a lightning rod for criticism, particularly as it is 49%-owned by a politically-connected United Arab Emirates investment fund and owing to its relationship with Binance, which is reported to have helped develop World Liberty’s USD1 stablecoin.

You may have even heard of ALT5 Sigma — recently rebranded as AI Financial Corporation — into which World Liberty led a purported $1.5 billion investment in 2025.

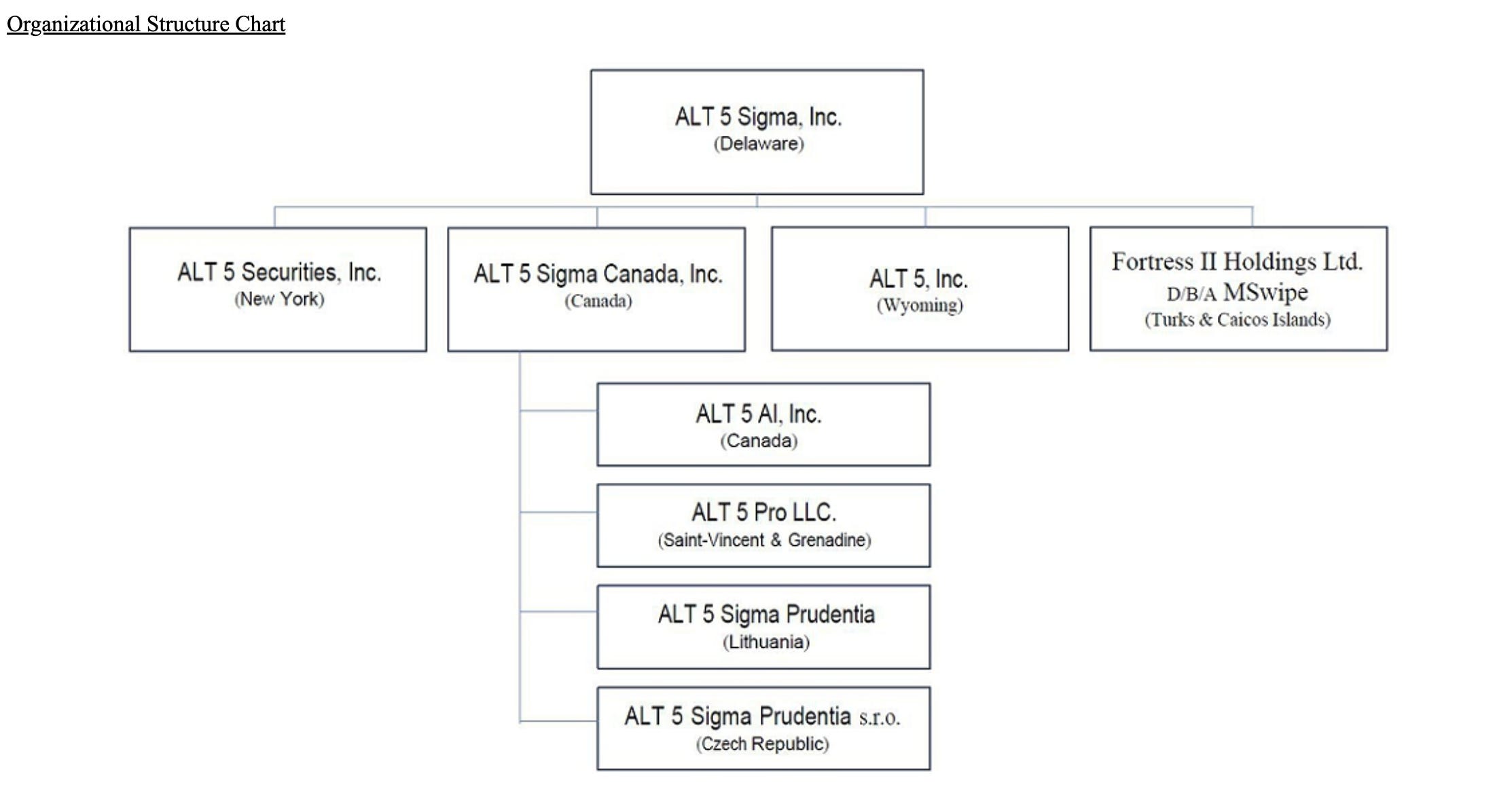

But you probably have not heard of ALT5 subsidiary MSwipe, a Quebec-based middleware-style payment card issuing platform, which also operates under the name Stradacarte.

MSwipe, according to its own documentation and staff, offers so-called “no KYC” cards, ostensibly to be used for media buying — purchasing ads on popular platforms like Google and Facebook/Instagram, as well as across the web and in mobile apps through demand side platforms. But such cards can also be exploited by bad actors for illicit uses, including paying for ads to promote scams or counterfeit goods, as well as use for money laundering and sanctions evasion.

This story is based on extensive reviews of ALT5’s Securities and Exchange Commission filings, current and historical versions of MSwipe’s and Stradacarte’s websites, multiple conversations with and onboarding documents shared by MSwipe’s own staff, and information from more than a dozen industry sources, including issuer-processors and program managers that worked directly with MSwipe or with which MSwipe sought to do business. Sources were granted anonymity, given the sensitivity of the topic and out of fear of retribution.

While, today, ALT5 Sigma ostensibly focuses on blockchain, payments, and digital currencies (and even announced it is exploring a collaboration to develop AI data centers), its roots are decidedly analog.

The company’s origin traces all the way back to 1976, when it was known as “Major Appliances Pick-up Service.” In or around 1989, that entity merged with a publicly listed Minnesota-based company. The earliest electronic records available in the Security and Exchange Commission’s EDGAR system reflect the name the company went by for approximately four decades: Appliance Recycling Centers of America, Inc.

(Much of the background history of what became ALT5, now known as AI Financial Corp, and World Liberty’s investment in and relationship with the company has been previously covered by Reuters, Bloomberg, FT, Forbes, Fortune, CNBC, The Information, Wired, Coindesk, The Block, and others.)

In the late 2010s, the company appears to have begun cycling through various trendy business models. It acquired an “internet of things” technology company, GeoTraq, in 2017.

The company rebranded from “Appliance Recycling Centers of America” to “JanOne” in 2019, amid a pivot to focus on biotechnology. The company disposed of the GeoTraq IoT subsidiary in 2022 and acquired Soin Therapeutics, which purported to be developing a low-dose naltrexone pain treatment, the same year.

In May 2024, JanOne acquired ALT5 Sigma, a blockchain technology company, and assume its name. The following year, as part of the pivot to focus on blockchain, crypto, and payments, the publicly listed entity, known as ALT5 Sigma Corporation at this point, announced a definitive agreement to acquire Canada-based MSwipe.

According to the May 2025 announcement (emphasis added):

“Mswipe is a next-generation payment solutions provider offering multi-currency, fiat payment card services, along with crypto-enabled capabilities through its existing integration with the ALT5 platform. Its suite of physical and virtual cards, available on both the Visa and Mastercard networks, allows users to seamlessly spend traditional and digital currencies worldwide… This capability-enabling instant conversion of stablecoin and other cryptocurrency balances into fiat, and allowing customers to pay merchants in their local currency-significantly expands real-world use cases for digital assets.”

So, what is the connection between ALT5 Sigma and World Liberty Financial?

Less than three months after ALT5 announced its MSwipe acquisition, the company revealed it would receive a purported investment worth $1.5 billion, led by World Liberty Financial.

While some news reports described it as a “$1.5 billion funding round,” the reality is significantly more complicated. ALT5 Sigma’s August 2025 press release describes the deal by saying:

ALT5 Sigma Corporation… today announced that it has entered into definitive agreements for the issuance and sale of an aggregate of up to 100,000,000 of its shares of common stock (or common stock equivalents in lieu thereof) in a registered direct offering (the “Registered Direct Offering”) at a purchase price of $7.50 per share. In a concurrent private placement (the “Private Placement Offering” and, together with the Registered Direct Offering, the “Offerings”), the Company has entered into a securities purchase agreement for the purchase and sale of 100,000,000 of its shares of common stock (or common stock equivalents in lieu thereof), at the same purchase price of $7.50 per share as in the registered direct offering. The gross proceeds of the Offerings are expected to be approximately $1.5 billion, before deducting placement agent fees and other offering expenses.

In plain English, ALT5 raised $750 million by issuing and selling 100 million shares at $7.50 each to a group of unnamed private investors. Later reporting indicates hedge funds Point72, ExodusPoint, and Soul Ventures were among the names that bought shares in ALT5.

ALT5 simultaneously entered into an agreement for the private placement of 100 million shares with World Liberty Financial. But, rather than pay ALT5 for its shares in US dollars, World Liberty paid in the form of $WLFI, the company’s so-called “governance” token. $WLFI wasn’t yet trading, and thus did not have a market-set price; the ALT5 deal valued each $WLFI token at $0.20. This was the first external price established for $WLFI.

As part of the private placement with World Liberty, Zach Witkoff — the son of President Trump’s advisor and envoy Steve Witkoff and the cofounder of World Liberty — became the chairman of ALT5.

It was announced at the time that Eric Trump would become a director of ALT5 and that Zak Folkman, another World Liberty cofounder, would become a board observer. But, due to an unspecified Nasdaq listing rule, Eric Trump was unable to take the board seat and swapped places with Folkman to act as a board observer instead.

Matt Morgan, described as an advisor to World Liberty Financial, would become ALT5’s chief investment officer. This April, ALT5 would acquire another company Morgan served as cofounder and CEO of, Block Street, for an undisclosed sum.

Of the approximately $750 million in actual cash raised in the transactions, ALT5 turned around and used nearly all of it to buy more $WLFI tokens. ALT5 retained approximately only $10 million in US dollars, which the company said it would use towards debt service, litigation expenses, and to fund operations.

According to the World Liberty “Gold Paper” — rather than the customary crypto project white paper — an entity affiliated with President Trump, DT Marks DEFI LLC, is entitled to 75% of “the net protocol revenues as defined in the services agreement after deduction of agreed operating expenses and the initial treasury reserve.”

The upshot is that, of the $750 million in cash ALT5 raised by selling new shares to institutional investors, as much as $537 million could have ended up going to President Trump and his family via DT Marks DEFI LLC.

The various transactions effectively transformed ALT5 into a treasury for $WLFI tokens, analogous to what Strategy (formerly Microstrategy) is for bitcoin: a publicly traded stock wrapper around a crypto token. Owning shares in ALT5 became, indirectly, primarily exposure to the value of $WLFI.

Such treasury company strategies have proven they can be quite profitable — when the value of the underlying crypto asset is increasing.

The $WLFI token began trading on September 1, 2025, shortly after the ALT5-World Liberty deal, at around $0.23, slightly above the price implied by the ALT5 deal. But its value quickly drifted downwards, and it now trades at about $0.05 per $WLFI token.

ALT5’s share price reached as high as $8.35 in the wake of the announcement of the World Liberty deal, before the $WLFI began trading, giving it a market capitalization of just over $1 billion.

But as $WLFI price has slid, so too as ALT5’s — dropping to a mere $0.54 as of Friday’s close, for a market capitalization of just $70 million. Per an 8-K the company filed earlier this month, it is at risk of being delisted from the Nasdaq, as it does not meet the minimum bid requirement of $1.00 per share.

The share price hasn’t been the only problem at ALT5. There has been significant executive turnover, with ALT5 cycling through through three CEOs in a roughly six week period in late 2025. ALT5’s auditor resigned, only to be replaced by an auditor whose licensed had expired. A former consultant allegedly accessed and transmitted ALT5 company documents to a competing business.

And, in a truly bizarre twist, ALT5 disclosed that it learned in August 2025 that its Canadian subsidiary, ALT5 Sigma Canada, Inc., and former principal Andre Beauchesne had been found guilty in a Rwandan court in May 2025 on charges of illicit enrichment and money laundering. The Rwandan court ordered the imprisonment of Beauchesne, the imposition of fines against Beauchesne, the confiscation of ALT5 Sigma Canada Inc.’s funds totaling approximately $3.5 million and the dissolution of ALT5 Sigma Canada Inc.

This January, ALT5 was forced to borrow $15 million from World Liberty — collateralized by ALT5’s holdings of $WLFI tokens — to meet basic operating expenditures. The company has ongoing losses, issued a warning there is “substantial doubt” about its ability to remain a going concern, and, as reported last week, is in talks sell its core business to Japan-based Perpetuals.com

Soul Ventures and Point72 Asset Management, which had invested $85 million and $36.5 million, respectively, both exited their positions in ALT5 before the end of 2025. ExodusPoint still held its investment as of the end of March 2026.

Eric Trump was quietly removed from ALT5’s public website. It is unclear if Eric Trump remains as a board observer. Trump is not listed as a board observer or in any other capacity in the company’s annual report for 2025, which was filed on April 28, 2025. Because board observers are neither directors nor officers, ALT5 would not have to file an 8-K disclosing if and when Trump’s role as a board observer ended.

Folkman, the World Liberty cofounder, remains the chairman of ALT5 (now AI Financial Corp)’s board of directors, and World Liberty continues to be considered a “related party” to the company.

Matt Morgan, the World Liberty advisor, appears to continue to be affiliated with ALT5, though it is unclear if he is serving as its chief investment officer, as previously announced. Morgan is not listed as a director nor executive officer in the company’s most recent 10-K filing.

While ALT5 Sigma’s deal with World Liberty effectively turned it into a $WLFI treasury company, ALT5’s preexisting operations continued — including MSwipe, the middleware-style platform ALT5 agreed to acquire in May 2025.

MSwipe, which has also operates under the name Stradacarte and appears to have shifted to primarily using that name recently, has historically been focused on the prepaid card space.

A thorough review of prior coverage indicates the links between World Liberty Financial to MSwipe/Stradacarte through World Liberty’s 2025 investment in ALT5 have not been previously reported.

An archived version of MSwipe’s website from September 2023 identifies Patriot Bank as the company’s card issuing partner at that time. The same disclosures also indirectly identify CFSB as a supporting bank, via CFSB’s relationship with cross-border payment provider Currency Cloud.

A 2024 version of the site does not mention Patriot Bank, citing only “The Bank, N.A.” It is not clear if this is actually intended to reference a bank by that name (yes, there is a bank named The Bank, N.A., though it does not appear to support fintech partnership programs.)

Today, MSwipe’s site does not appear to specify any issuing bank partner or, for that matter, even include any kind of terms and conditions or disclosures. Links on Stradacarte’s site for “Terms” and “Compliance” direct visitors to speak to an account specialist, who can “share the card program specifications.”

I did just that — contacted Mswipe/Stradacarte. At no point did the company’s staff request nor did I enter into any kind of non-disclosure agreement, nor did the staffers I interacted with ever indicate that they wished the conversations to be considered confidential.

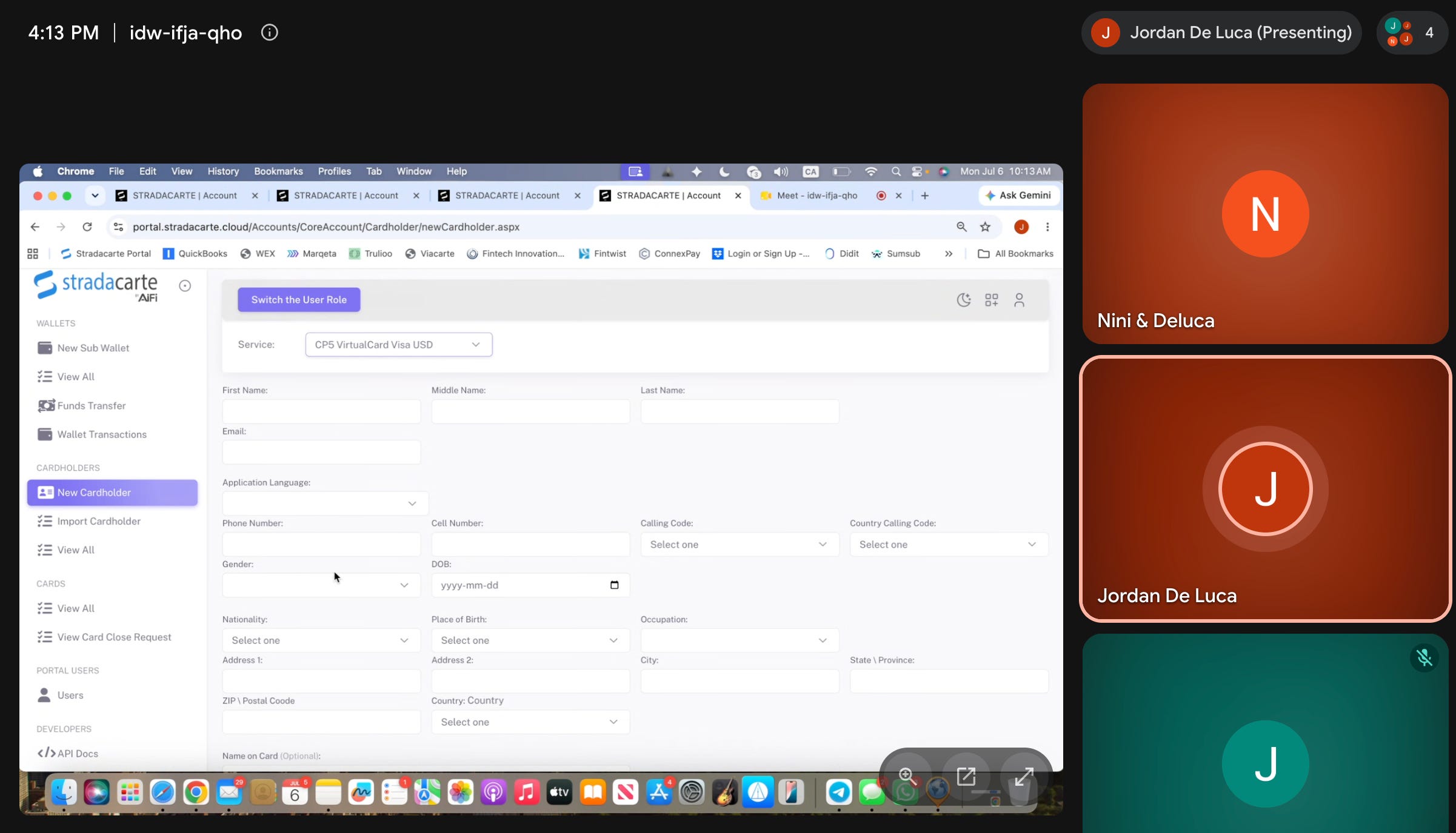

After filing out a web form on Stradacarte’s website, I was contacted by one of the company’s employees via email. The staffer suggested moving the conversation over to popular messaging app Telegram, and we subsequently exchanged messages and had multiple calls for them to provide an overview and demo of Stradacarte’s capabilities.

Asked what the onboarding and due diligence with Stradacarte looked like, the staffer explained that it is pretty straightforward — company incorporation documents, information on shareholders and the like — and said that “within max 48 hours, everything’s approved.” They did say on the ALT5 side, the process was a little more involved, and that it could take somewhat longer — 72 hours, according to the Stradacarte employee.

Asked if a business working with Stradacarte would ever be expected to or need to interface with Stradacarte’s underlying bank and program manager partners, the staffer was unequivical, saying, “No, everything goes through us.”

While not uncommon in the earlier days of banking-as-a-service, this “nested” approach generally fell out of favor after the wave of partner bank enforcement actions seen from around 2022 to 2025, during which more than a dozen banks were hit with regulatory actions, many of which highlighted BSA/AML and third-party risk management failures.

In the wake of the numerous BaaS-related consent orders, it became conventional wisdom that customer-facing fintech programs should have a “direct” relationship with their underlying bank partners in order to provide banks with better visibility and to promote better communication and clearly delineated compliance roles and responsibilities between the parties.

The Stradacarte staffer also told me that it works with 14 banks and program managers and that, while the company’s primary focus is on USD payment cards, it also supports issuing euro, Great British pound, and Mexican peso denominated cards.

While having more than one issuer relationship is common, for redundancy/business continuity, to support different use cases, geographies, and currencies, and for negotiating leverage, multiple industry experts told me it is extremely unusual and a red flag to have 14 issuing partners.

None of the banks or program managers Stradacarte works with appear to be explicitly listed anywhere on its website.

But, a review of the company’s public API documentation, a demonstration of its web platform by company staffers, and extensive conversations with industry sources across partner banks, issuer-processors, and program managers indicate Stradacarte’s 14 partners likely include:

Wex, most commonly known for its fleet card offerings, though the company, which has a banking subsidiary, also operates a virtual card issuing service marketed to fintechs;

Marqeta, a card issuing platform popular with fintechs that partners closely with Sutton Bank. Sutton Bank confirmed it has worked with MSwipe, but stated that it was “a past relationship” that “ended in Q1 of 2026”;

Corpay, previously known as Fintwist, which issues payroll cards and prepaid cards through its relationships with Regions Bank and Republic Bank & Trust;

ConnexPay, a B2B payments platform that supports virtual card issuing, including in GBP and EUR, through its relationships with The Central Trust Bank and MVB Bank;

and ViaCarte, a Panama- and Bahamas-based principal member of Visa and Mastercard that offers programmatic virtual card issuance (a login page hosted at mswipe.viacarte.com further confirms a relationship between the two).

Several of these names or the banks with which they partner have previously been linked to known “no KYC” crypto card programs, including The Central Trust Bank, Regions Bank, and Sutton Bank.

The Stradacarte staffer I spoke with also mentioned a Turks and Caicos-based issuer the company works with that offers physical prepaid cards that can be loaded with as much as $100,000 in a single transaction. The staffer explained that the partner is “crypto friendly” and that crypto deposits could be routed through ALT5 and loaded on to the issuer’s prepaid cards.

Several U.S. based banks, issuer-processors, and program managers Fintech Business Weekly spoke with said they had been approached by MSwipe/Stradacarte over the years, but declined to work with the company or quickly offboarded it if they had. One fintech CEO described MSwipe’s behavior as “shady” and pointed to suspicious transaction activity in bank account records it provided as part of the fintech’s onboarding and due diligence process.

Asked about its apparent relationship with MSwipe/Stradacarte, a Wex spokesperson shared the following via email: “We are bound by contractual and regulatory confidentiality obligations that prohibit us from discussing specific customer relationships, transactions, or account information. WEX does not offer or issue ‘no KYC’ card programs.”

A spokesperson for Marqeta shared the following statement: “Marqeta does not comment on current or former customer relationships. We maintain rigorous risk management, compliance and due diligence programs, including ongoing monitoring to ensure compliance with applicable laws and regulations.”

Representatives for ConnexPay and Corpay did not respond to questions or requests for comment.

The topic of so-called “no KYC” cards has popped up repeatedly over the years, most commonly as a mechanism for users to convert and spend crypto anonymously.

There are permissible prepaid product structures that don’t require traditional KYC (eg, may be exempt from customer information program requirements of the PATRIOT Act and/or relevant portions of FinCEN’s Prepaid Access Rule).

But, generally, such products cannot be reloaded, have fairly strict load/use/withdrawal limits, cannot transmit funds internationally, and do not permit peer-to-peer transfer among users within the program.

Arguably, the ability to programatically issue non-reloadable prepaid cards at scale could effectively enable circumventing dollar thresholds and rendering the reload issue moot, but other restrictions would, presumably, still apply.

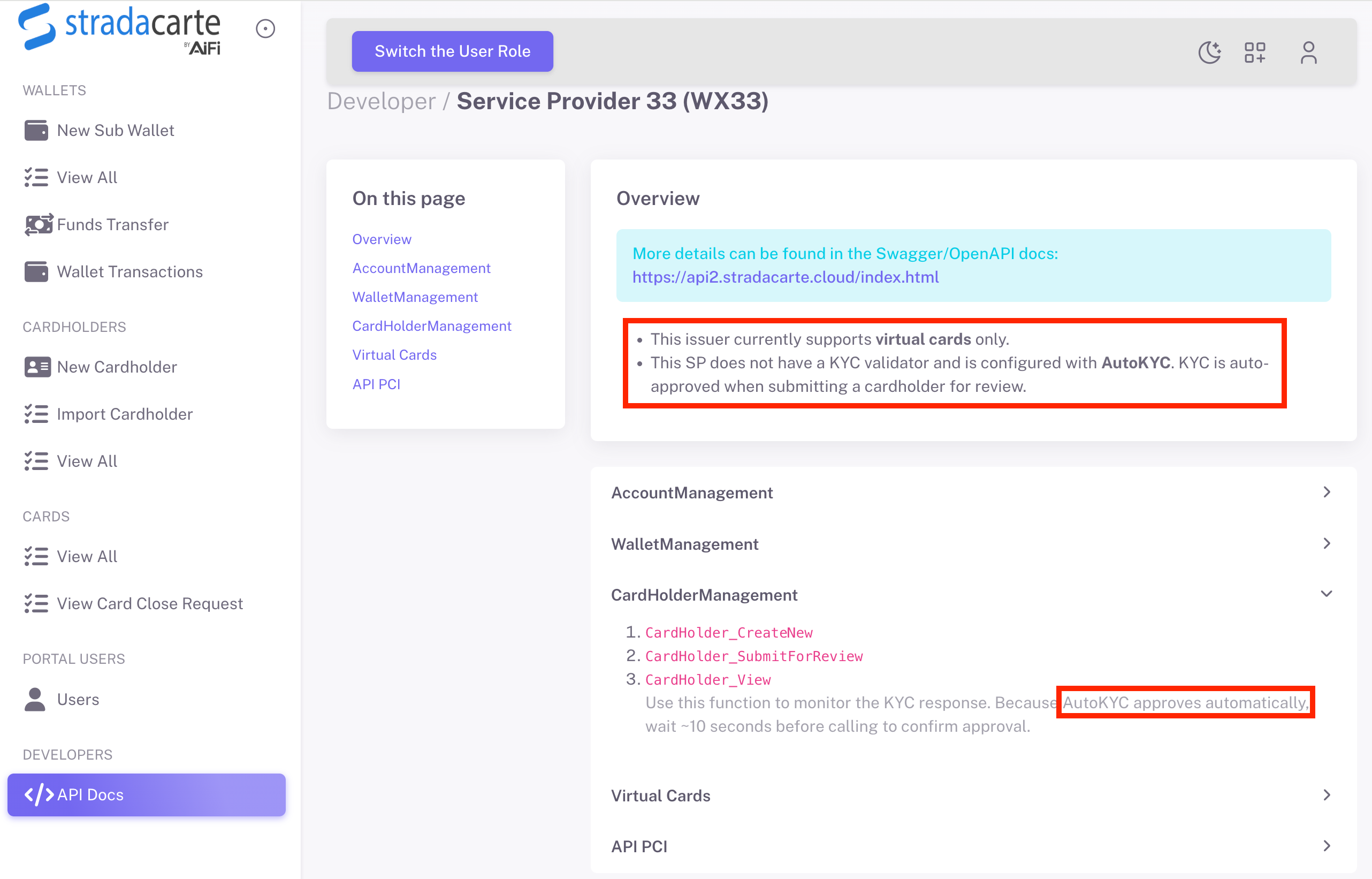

Stradacarte appears to explicitly allow for “no KYC” card issuing. Its API documentation for “Service Provider 33 (WX33),” which appears to correspond to Wex Bank, states that “[service provider] does not have a KYC validator and is configured with AutoKYC. KYC is auto-approved when submitting a card holder for review.”

Directly asked if KYC is required for media buying use cases — paying for ads on Google, Facebook, etc. — a Stradacarte staffer told me, “Because it is a media buy program, we don’t need to collect KYC for individual cardholders, so you can essentially just keep reusing the same cardholder name and address for all the cards you’re creating, if you want to. You just have to populate the cells with any information you want, and the card will work, as long as when you’re doing the transaction it matches the information you inputted correctly.”

Asked if these “no KYC” cards could be funded via cryptocurrencies or stablecoins, the staffer confirmed it is possible to do so, and explained by saying, “Let’s say you have your crypto on Binance — you’ll send it from your Binance account to ALT5. Once it hits ALT5, you have the option to convert it to US dollars. You’ll do the conversion on ALT5, it’s like 25 basis points, then through ALT5, you can do an internal transfer to us, that’s completely free. You send it to our wallet. Once we get it, we’re able to top up your card or your wallet.”

The Stradacarte staffer clarified that for corporate cards issued for media buying, they collect documentation on the company that is being onboarded, but not for downstream individual users/cards.

During our call, the Stradacarte employee explained that “everything would have to be funded from the company that we onboard — you. And I mean, anything under you, that’s up to you, you know, to figure out how you’re collecting your due diligence or whatever.”

While media buys are a legitimate use case for the type of corporate cards Stradacarte offers, it is a higher risk one. Bad actors can use such cards for ad spend to promote grey or black market products and services that are disallowed by platforms, such as online pharmacy, counterfeit goods, or online gaming/gambling, for example. Online ads paid for through such spend cards can also be used for more nefarious purposes — promoting scams, like pyramid or “pig butchering” schemes — and even as a mechanism to launder illicit funds.

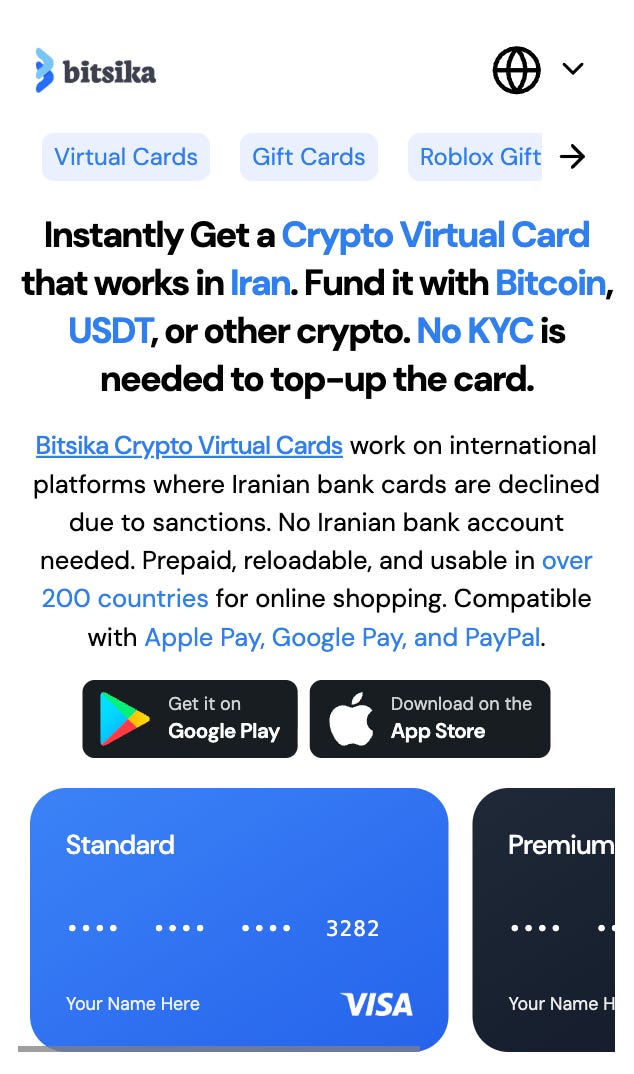

Multiple sources told Fintech Business Weekly that various “no KYC” crypto card programs have leveraged MSwipe/Stradacarte to power their offerings, including Alphaspace and Bitsika.

Bitsika, which Fintech Business Weekly first covered in February 2026, issued prepaid cards on Sutton Bank — apparently via MSwipe, according to the sources Fintech Business Weekly spoke to.

Bitsika explicitly marketed its crypto virtual cards for use on “international platforms where Iranian bank cards are declined due to sanctions.”

After Fintech Business Weekly’s report, Bitsika appears to have pivoted to enabling users to convert cryptocurrency and stablecoins into in-game currencies for games like Call of Duty and League of Legends.

Beyond its apparent relationship with MSwipe/Stradacarte, Sutton Bank has been linked to numerous “no KYC” crypto card programs, including CinCin, ekame, Uncash, Bitsika, and PayWithUs.

Sutton has been operating under a consent order it entered into in February 2024, stemming from gaps in the bank’s BSA/AML compliance, including staff training, suspicious activity reporting, its customer identification program, and its third-party risk management.

Despite the 2024 order requiring Sutton to “[c]ompile a complete inventory of third-party relationships,” it is not clear when the bank became aware of MSwipe/Stradacarte, which appears to have been issuing cards on Sutton through multiple issuer-processor and program manager intermediaries.

One industry source in the compliance space Fintech Business Weekly spoke to characterized Sutton as “a real mess,” and said they have advised programs to avoid working with the bank since several years ago.

Another source indicated the problems at Sutton are hardly new, saying they were aware of these kinds of issues at the bank going as far back as 2011.

And a third source, whose firm has worked with Sutton, described it as “a very paranoid and chaotic organization these days,” and paused before adding, “It’s always been that way.”

Multiple sources described Sutton as “Evolve 2.0,” referring to the embattled bank at the center of the Synapse collapse, Evolve Bank & Trust.

Asked what they thought of the “Evolve 2.0” characterization, a partner bank CEO responded flatly, “Not surprised. They’re incompetent.”

In response to a detailed list of questions about its relationship with MSwipe/Stradacarte, a Sutton spokesperson shared the following via email: “Sutton Bank does not offer ‘no KYC’ cards. If any such cards or issues are identified in the marketplace we work closely with our FDIC regulators to ensure we execute on all regulatory requirements and work diligently to immediately remediate any identified issues.”

While the links between World Liberty Financial, ALT5 Sigma/AI Financial Corporation, and MSwipe/Stradacarte are clear, there is no specific evidence suggesting that that Eric Trump, Zack Witkoff, or other persons associated with World Liberty or with President Trump were personally aware of or directing the activities of MSwipe/Stradacarte.

Nor is it clear to what extent MSwipe/Stradacarte itself is or was aware of how some programs appear to have been leveraging its infrastructure and relationships with underlying banks and program managers to offer “no KYC” crypto cards.

But the revelations about these “no KYC” programs should be viewed against the backdrop of a complex, intersecting set of stories:

the ongoing U.S. military confrontation with Iran;

reporting about how cryptocurrency and crypto exchanges have been used to evade U.S. sanctions on Iran;

ongoing rulemaking to implement the GENIUS Act, including regarding permitted payment stablecoin issuers’ BSA/AML and sanctions compliance obligations;

ongoing efforts from the crypto industry to get the CLARITY Act, commonly referred to as crypto market structure legislation, over the finish line in the Senate (including efforts from some lawmakers to add ethics-related measures that would bar sitting elected officials, including President Trump, from profiting from crypto ventures while in office);

federal banking regulators’ elimination of the use of “reputation risk” and push to refocus supervisory and enforcement efforts on “material financial risks,” which may result in less scrutiny of financial institutions’ BSA/AML practices;

ALT5 Sigma investor World Liberty Financial’s pending application with the OCC to charter a national trust bank (World Liberty also is the issuer of the fourth largest stablecoin, USD1);

the recent Supreme Court decision in Trump v. Slaughter, which effectively removes the protection heads of independent agencies had from being fired without cause;

and numerous oversight efforts from Democratic lawmakers, including over Binance’s alleged Iran and Russia links and World Liberty Financial’s various entanglements.

The American financial system is in the midst of what one could charitably call a grand experiment: expansive deregulation of the traditional banking system, the legitimization and integration of crypto and stablecoins, a push to “democratize” access to private markets, and a mostly laissez-faire approach to the aggressive growth of new entrants and products that include things like stablecoin-based banking and payments services, prediction markets, and perpetual futures.

Enforcement activity from federal regulators has dropped substantially in recent years. A just-released analysis from Brookings found that, from 2017 to 2019, regulators issued an annual average of 341 enforcement actions. But, for the 2023 to 2025 period, that had dropped by more than 20%, with an annual average of 263 regulatory enforcement actions during this period.

This deregulatory and laissez-faire trend seems more likely to continue than not.

But if it is the case that these kinds of trends act like a pendulum — when, and for what reasons, might the pendulum swing back? And, if and when it does, how might that reshape banking, fintech, and crypto?

Representatives for ALT5 Sigma/AI Financial Corporation did not respond to questions and a request for comment for this article prior to the time of publication.

Elsewhere last week, Klarna filed an application with the Utah Department of Financial Institutions to charter an industrial loan bank in the state and a corresponding application for deposit insurance with the FDIC; major outlets are reporting that a group of big banks is considering acquiring one of Fiserv’s debit networks; and $3.7 million asset Kentland Federal Savings and Loan was placed into receivership.

Source link