Greater China’s narrowing technological gaps with the West, vibrant university-to-early-stage deep tech ecosystem, and highly competitive yet increasing capital-intensive AI infrastructure growth are driving a resurgence of global interest and capital inflows into its deep tech and AI sectors.

AI funding, especially big-ticket investments in companies like foundational model startup StepFun, generative AI unicorn Moonshot AI, and embodied AI developer Galbot, has driven Chinese venture funding to reach an estimated $16.5 billion in the first quarter, according to Crunchbase data.

This marked the third consecutive quarter for increased venture funding in China and accounted for 60% of all Asian startup funding in Q1, followed by India as a distant second in Asia with $3.8 billion in venture funding.

As Chinese AI becomes a sought-after portfolio component for venture investors and China-born deep tech takes big strides, avoiding this rapid development and not having exposure poses its own risk, said Philip Hu, founding member and managing director of Primavera Capital Group, during a panel discussion at DealStreetAsia’s Asia PE Leadership Summit on May 20 in Hong Kong.

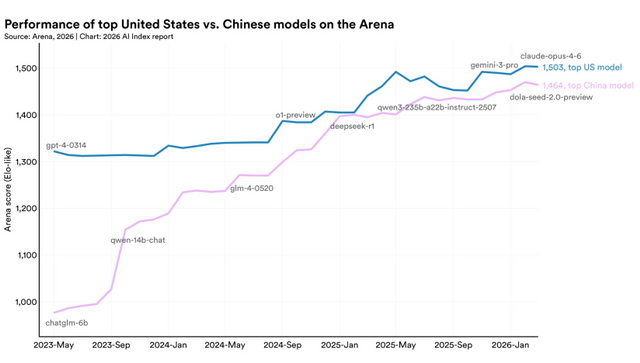

This influx of venture funding into China aligns with its exceptional AI and deep tech gains. “If you look back to May 2023, there was a very clear gap between the US and China in terms of AI model performance. Fast forward to today, that gap has basically disappeared — around 2%-3% difference,” Hu told the audience, citing the latest 2026 AI Index Report by Stanford University.

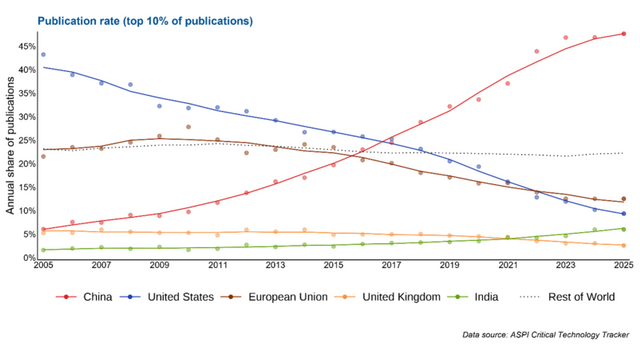

He further cited another report, which outlined a stark updated picture when comparing China and the US across other deep tech areas nowadays: China now leads in 66 of the 74 critical technologies, versus the US, which led in the remaining eight, according to findings published in December 2025 by the Australian Strategic Policy Institute’s (ASPI) Critical Technology Tracker, which maps high-impact scientific research across critical technologies.

This is in contrast to the years between 2003 and 2007, when the US was found leading in 60 out of 64 critical technologies at the time, while China led just three.

The past decade saw China effectively erode an overwhelming US lead across fundamental research. Hu argued that the ongoing AI boom and a continuous rise in demand for massive energy infrastructure, particularly low-cost renewable power, will give China – the global leader in clean energy – a natural upper hand in the AI race over the coming years.

“If you don’t have exposure to Chinese innovation, Chinese AI, or Chinese robotics, that is a risk,” said Hu.

Keeping pace with the ‘AI tsunami’

One of the major changes in Greater China is how alumni and researchers from top academic institutions are now at the epicentre for leading multi-billion-dollar AI and deep tech champions.

Academic institutions in China, most notably Tsinghua University, have become the research hubs and talent pipelines fueling generative AI and large language model (LLM) ventures. Prominent examples include Zhipu AI, one of the hottest AI stocks in Hong Kong, whose founder and chief scientist, Tang Jie, is currently a chair professor at the Department of Computer Science at Tsinghua University. Tang’s student, Yang Zhilin, is the co-founder and CEO of Moonshot AI, the unicorn behind chatbot Kimi. The founder of Alibaba Group-backed general foundational LLM developer Baichuan AI, Wang Xiaochuan, also earned his degrees from Tsinghua University.

Meanwhile, the broader university ecosystem in Greater China is emerging as a driving force in global AI and deep tech development, with more university capital actively participating in startup incubation and helping bridge the gap between academic research and commercial tech power.

AI-centric startups growing out of the university circle are raising large early rounds with relative ease, said Dr. Paul Wang, a director of the HKU Techno-Entrepreneurship Core (TEC).

“For AI, I don’t think they face any ‘Valley of Death’ nowadays,” said Dr Wang. Instead, his network of venture capitalists has been reaching out lately for his help to “put in a good word” in hopes that certain hotly contested AI startup founders might reconsider their term sheet offers.

To an extent, the “AI tsunami” has made it difficult for top universities to retain young, world-class faculty members, who are regularly being offered higher pay and better packages to join or launch an AI startup, said Dr Wang.

In comparison, university-born startups across other deep tech sectors, such as biotech and material sciences, still face a long timeline to grow from lab to fundraising readiness in the private markets.

“The biggest structural bottleneck, I believe, is [building] the team,” said Dr Wang. “A good professor is not always a good entrepreneur. When they find the right entrepreneur partner, that is when the project begins to take off.”

Scaling deep tech

While the panel agreed that academic institutions are a primary breeding ground for groundbreaking innovation, fellow speaker Rafael Ratzel, a managing partner at T-Capital, revealed a more diversified approach to sourcing high-IP investments.

Given T-Capital’s deep roots in the academic world – particularly a long-standing relationship with Tsinghua University and its endowment fund, university spin-offs contribute to about 30% of the firm’s deal flow, including Zhipu AI, Ratzel noted.

The remaining 70% of its portfolio originates from a much wider spectrum. “What is a very prevalent opportunity in China, especially in the deep tech field, is founders coming out of big technology companies or MNCs,” said Ratzel.

He highlighted that some of T-Capital’s most successful investments involve seasoned executives spinning out of multinational corporations (MNCs) and global tech giants. These founders, who were previously executives at global sector leaders like Corning Incorporated and KLA Corporation, often bring decades of industrial experience alongside an established patent portfolio.

By backing these experienced founders in building Chinese equivalents for highly specialised optical computing and metrology systems, growth equity-focused T-Capital side-steps the initial commercialisation risks that frequently plague pure academic projects.

A prime example of this strategy is T-Capital’s investment in Moore Threads, a Chinese challenger to Nvidia. The Beijing-based GPU maker, whose $1.13-billion STAR Market IPO in December was 4,000 times oversubscribed, was set up in 2020 by James Zhang, a veteran of Nvidia’s China operations.

For T-Capital, balancing the raw innovative energy of the 30% university cohort with the operational expertise of the 70% corporate cohort provides the structural diversification necessary to “de-risk” the highly volatile deep tech landscape amid geopolitical shifts and the China-US tech decoupling.

Under this approach, T-Capital has already fully deployed its debut $100-million US dollar fund across 12 companies. The portfolio spans nuclear fusion, high bandwidth memory chips, RISC-V data centre infrastructure chips, robotics chips, energy transition, and the so-called “low-altitude economy,” which is a rapidly emerging sector driven by autonomous drones and electric vertical take-off and landing (eVTOL) vehicles.

His views were echoed by Alice Zhu, Empyrean Sky Partners’ director, who specialises in physical AI and hard tech investment.

While the transition from lab to markets relies heavily on cultivating “compound talent” with R&D, corporate, financial, and industrial expertise, Zhu said that the current era of deep tech demands the founding team to develop a tech idea with commercialisation in mind from day one.

To successfully build a viable market product, the founding team needs to leverage the corporate, financial, and industrial perspectives to “understand what the industry pain point is and where the technology can be applied,” said Zhu.

Furthermore, an accelerating “flywheel” of product-market fit, scaling operations, and valuation growth from seed to pre-IPO can be achieved through a sophisticated understanding of global markets and a well-planned expansion strategy beyond China, she added.

This includes designing international corporate architectures and overseas entities early on to capture market attention, access broader pools of capital, and monetise innovations on a global scale, said Zhu.

Empyrean Sky Partners, which is backed by Chinese smart home robotics player Dreame Technology, targets to grow Chinese deep tech startups into internationally recognised names and to power traditional conglomerates in their ongoing tech transformation.

‘Capital is the name of the game’

As more data centres are getting built with energy-intensive hardware designed for AI, the sheer capital requirements of the current AI revolution are changing how investors approach late-stage opportunities.

Andy Yin, general manager of global private markets at Olive Asset Management, emphasised that modern AI companies require unprecedented fundraising speeds and capital density, which itself acts as “a competitive advantage” in recruiting top talent and running superior models.

“Capital is really the name of the game for this round of [AI-led] industrial revolution,” he said.

Yin revealed that Olive Asset Management, which deploys an average of $2-3 billion annually on behalf of global Chinese-speaking high-net-worth individuals and family offices, is moving away from “gold diggers” in the latest AI era.

Instead, the firm is pouring “the lion’s share” of client money into “shovel makers,” focusing heavily on AI infrastructure assets like data centres and energy solutions, the physical backbone of the AI economy.

For now, Yin said that he is only investing selectively in top AI-focused VC funds and AI winners. Regarding direct investments in AI companies, he outlined three key criteria, including a total addressable market (TAM) north of $10 billion, clear category leadership, and real-world financial revenue, preferably with profits.

Although the stock markets in Greater China, especially Hong Kong, are “red hot” for AI listings, he sounded a note of caution: “As an LP, my general advice to GPs is to try to make your fund more flexible and, if possible, shorter [in returning capital]. If you lock me up for 10 years, who knows what is going to happen?”

Limited partners (LPs) are still “healing their wounds” from the 2020-21 vintages, when record-high multiples led to subsequent valuation markdowns and a sluggish exit environment, said Yin. “Now the new hype comes in. LPs are questioning with a healthy dose of suspicion: Is 2026 another hype year that will end up being a very bad vintage?”

Source link